Home loan rates were near 7% recently however purchase applications were still able to take out an 8% week-to-week gain. That was remarkably strong, however as I have constantly stressed out, context is important. Purchase apps were coming off a four-week losing streak and despite the fact that those were moderate week-to-week decreases, it was still 4 weeks of weak point. The current development broke that streak, however need is still low.

Active real estate stock grew while brand-new listing information fell. Home loan rates barely budged recently, even with the Federal Reserve‘s statement it was stopping briefly rate walkings and CPI inflation reports

Here’s a fast rundown of the recently:

- Active stock grew 8,041 weekly. I am still expecting some weeks that reveal stock development in between 11,000-16,000

- Home loan rates remained in a tight variety in between 6.94% -6.98%

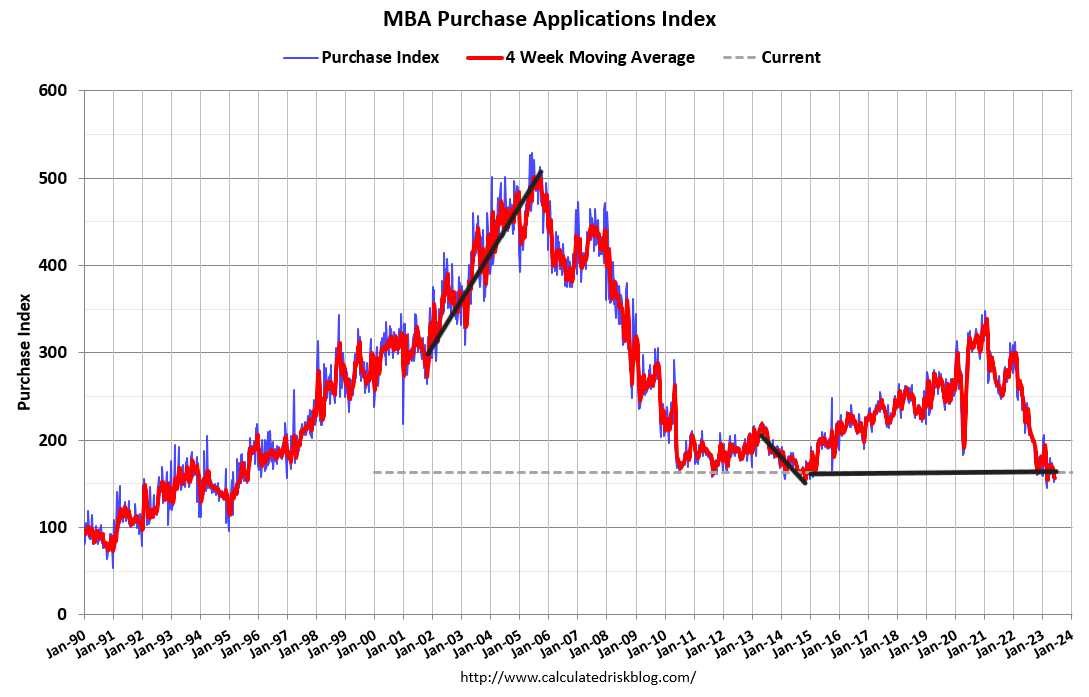

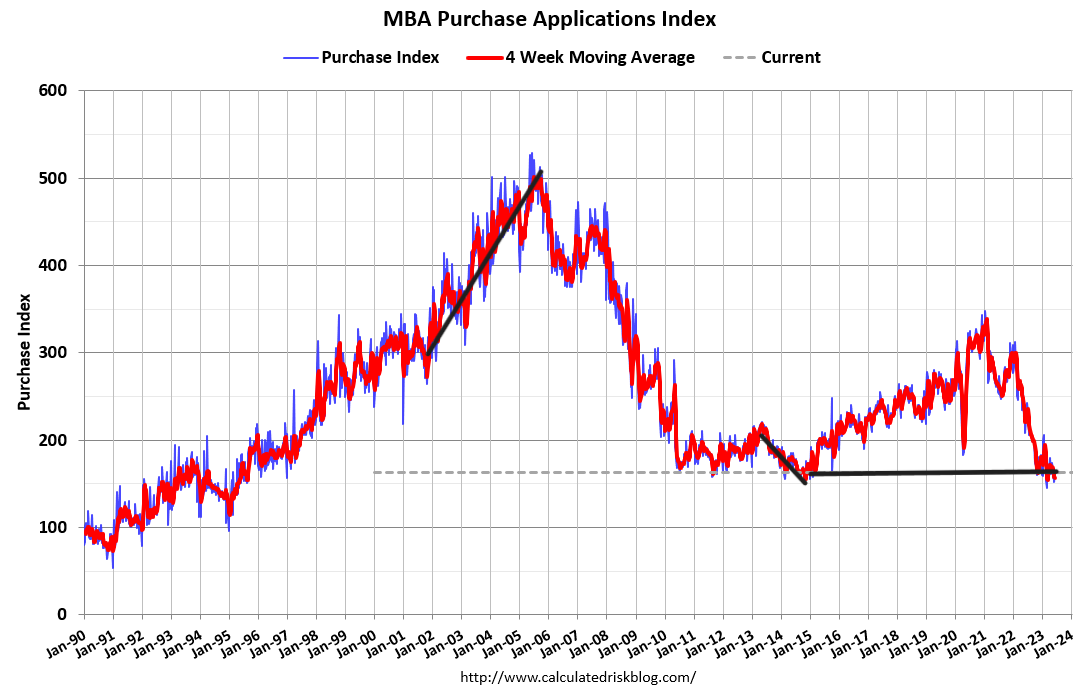

- Purchase application information revealed an 8% development week to week

Purchase application information

Recently’s 8% week-to-week development with rates near 7% was more powerful than anticipated. However, in 2015 we had the most significant waterfall collapse in purchase application information ever for a single year, and given that Nov. 9, 2022, this information has actually been forming a bottom-end variety.

This vibrant altered the real estate market from one where house sales were crashing to one that is now supported. I describe how this occurred in this current podcast As you can see in the chart below, the collapse of the purchase application information has actually stalled out, and if this didn’t occur, we would be having a various discussion about the real estate market today.

Nov. 9 is a vital date since that’s when the real estate market turned. Because that date, the purchase application information, after making some vacation modifications, has actually had 18 favorable and 11 unfavorable prints. Year to date, we have actually had 11 favorable and 11 unfavorable prints.

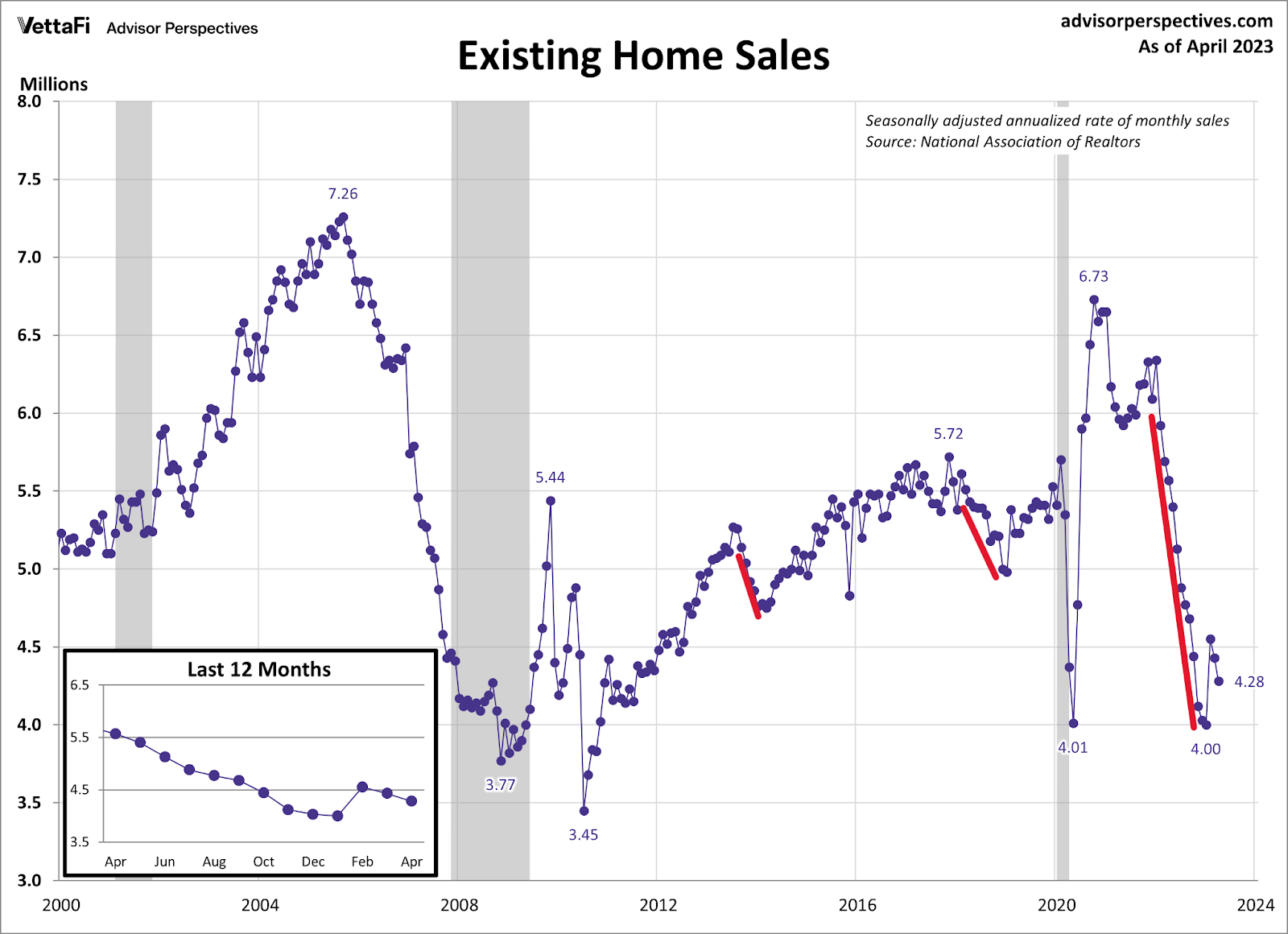

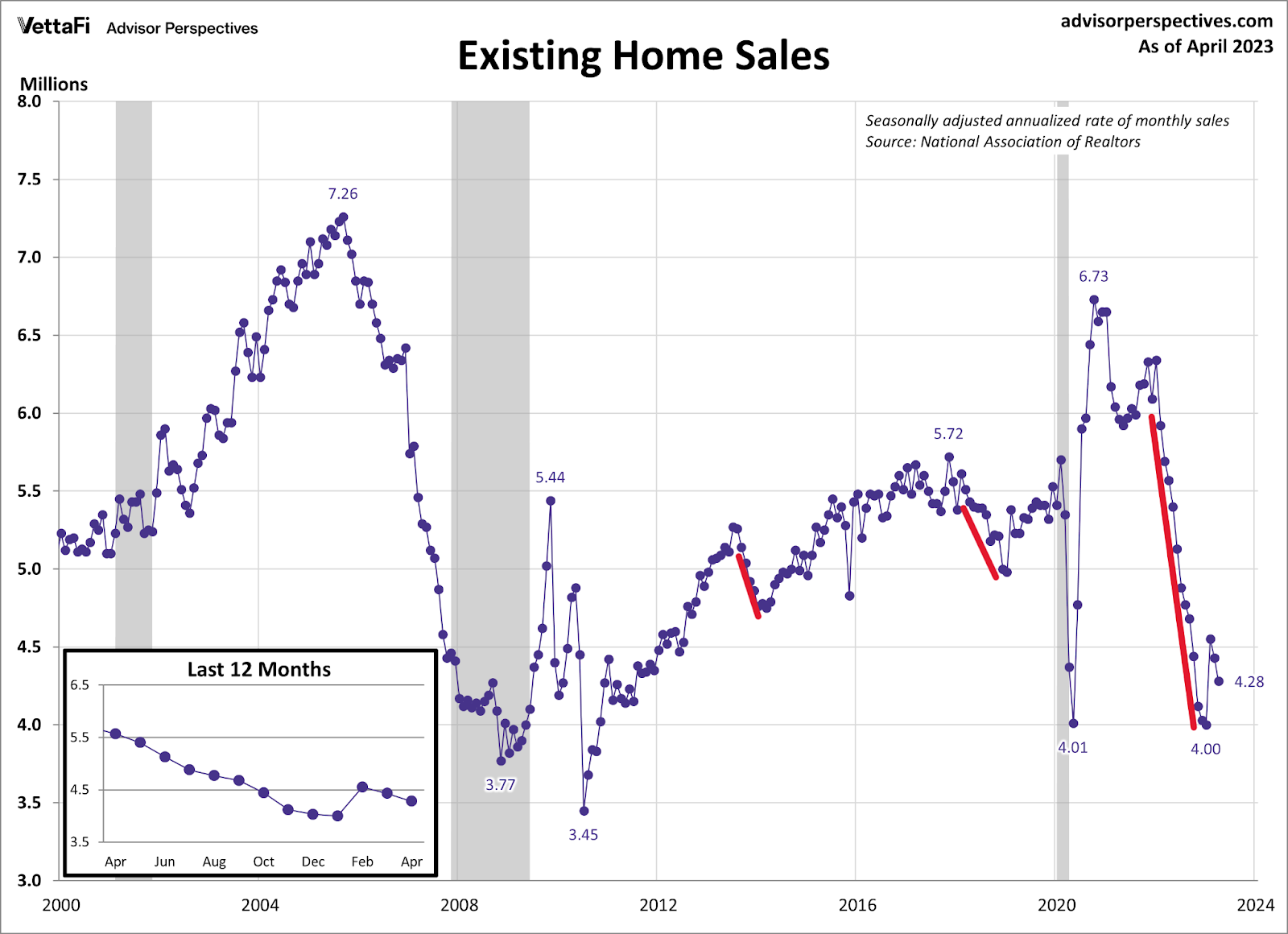

The development we saw from Nov. 9 to February was long enough to offer us the just huge existing house sales print we have actually had this year. In reality, after that, very little has actually been occurring, so the sale varies must remain in between 4 million and 4.6 million this year. Nevertheless, if we get more weak point in purchase apps, there is an opportunity that this information line goes listed below 4 million.

Existing house sales are showing up, however I do not anticipate any huge surprises in this week’s report. We can not break over 4.6 million this year unless we get a long string of favorable purchase application information, which would need lower home mortgage rates. In 2015, when home mortgage rates fell from 7.37% to 5.99% for a couple of months, we had a string of favorable purchase application information that assisted in that huge house sales print. Envision what the real estate market would appear like if rates remained in between 5.5% -6% for a year.

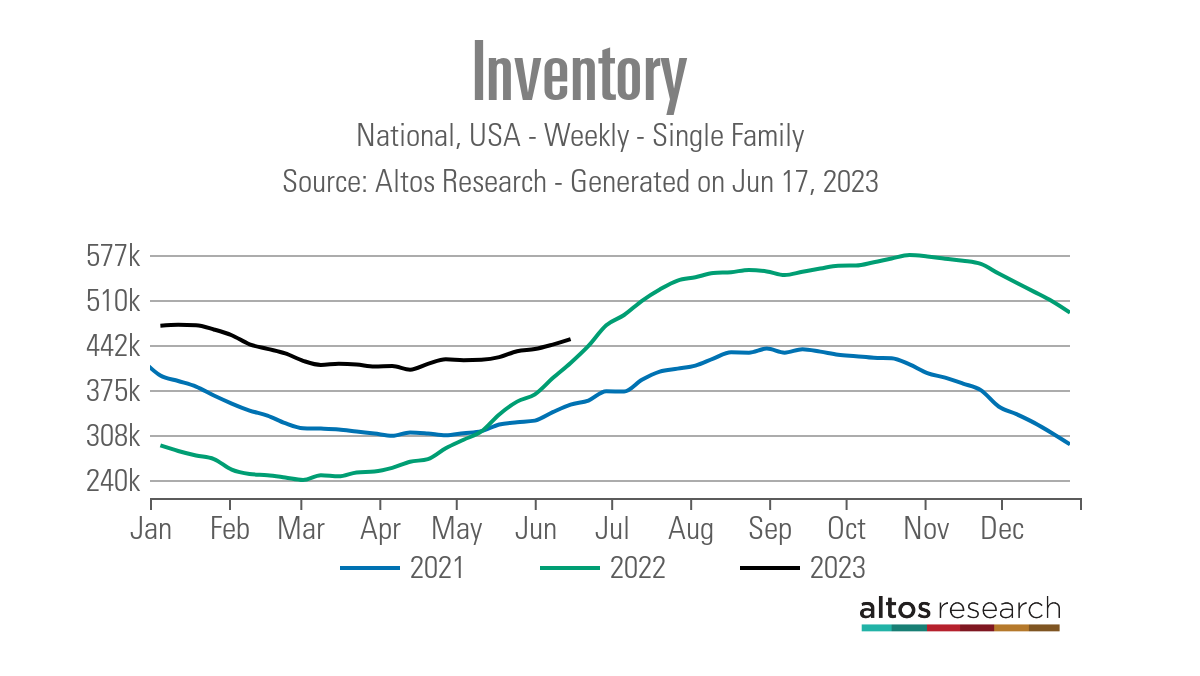

Weekly real estate stock

This year’s real estate stock style has actually been a strolling dead musical chorus of a zombie attempting to get away a tomb. Sluggish and constant and late! It took the longest time ever taped in U.S. history to discover the seasonal stock bottom, which took place on April 14, and it’s been a sluggish increase ever since.

However, it’s still an increase! A typical real estate market constantly has a spring stock boost and after that stock fades in the fall and winter season. While I wished to see more stock development this year, I will take what I can.

- Weekly stock modification (June 9-16): Stock increased from 443,006 to 451,047

- Very same week in 2015 (June 10-17): Stock increased from 392,792 to 415,582

- The stock bottom for 2022 was 240,194

- The peak for 2023 up until now is 472,680

- For context, active listings for today in 2015 were 1,173,793

As you can see in the chart below, the stock development has actually been so sluggish that we are on the edge of revealing some unfavorable year-over-year stock information. This occurs with purchase application information being flat year to date. Naturally, if we get some weak point in need, then days on the marketplace can grow and enable stock to build up.

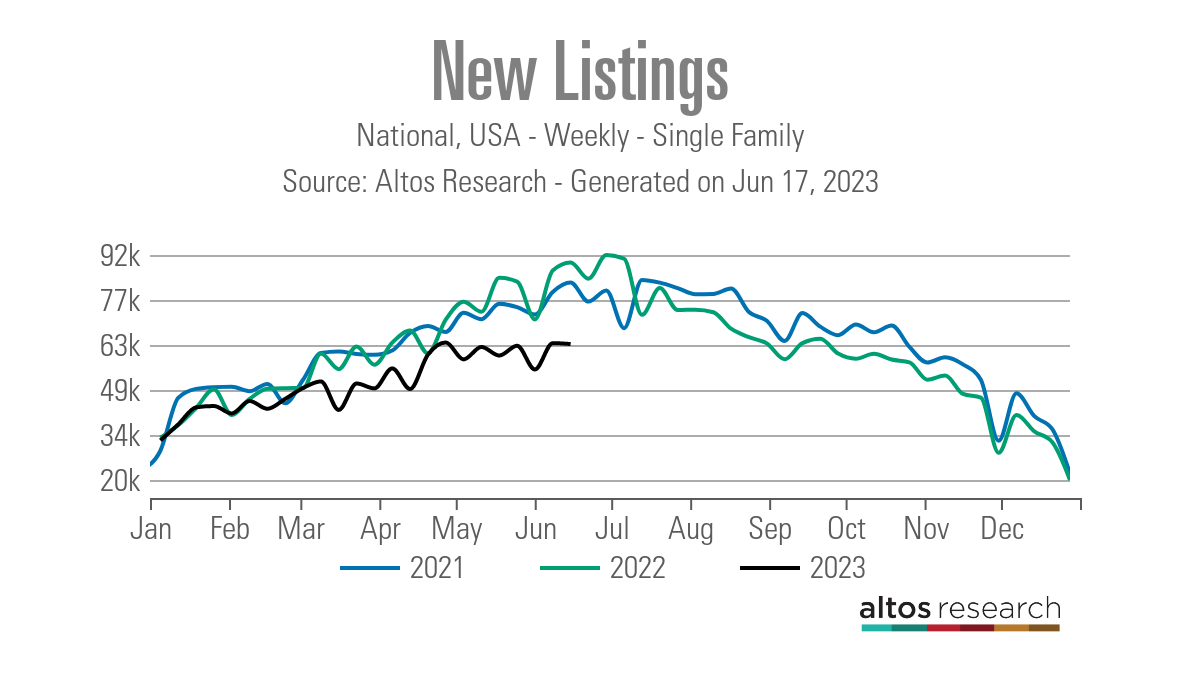

New listings information is another huge story with real estate stock. Considering that the 2nd half of 2022, it has actually been trending at lowest levels This pattern has actually continued all year long, so we have actually restricted brand-new real estate to deal with.

Below are some numbers to compare the brand-new listings information recently. As you can see, in 2015 we were revealing some year-over-year development, however that’s not the case this year.

- 2023: 63,293

- 2022: 89,166

- 2021: 82,815

We just have a couple of weeks left prior to we will see the standard brand-new listings information decrease and just a few months left prior to we see the standard active listing supply decrease. Today we will get the NAR existing house sales report, which will upgrade that stock information line, however overall stock levels are still traditionally low

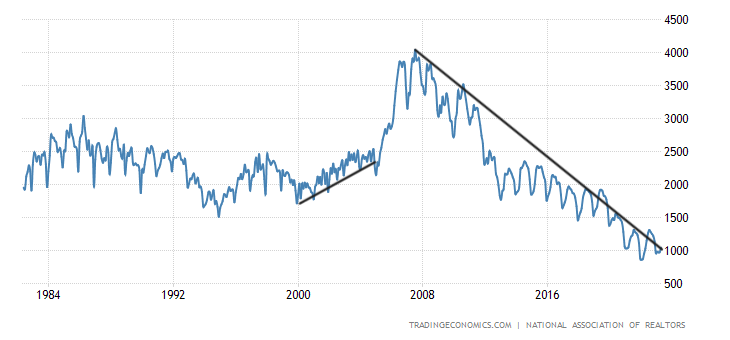

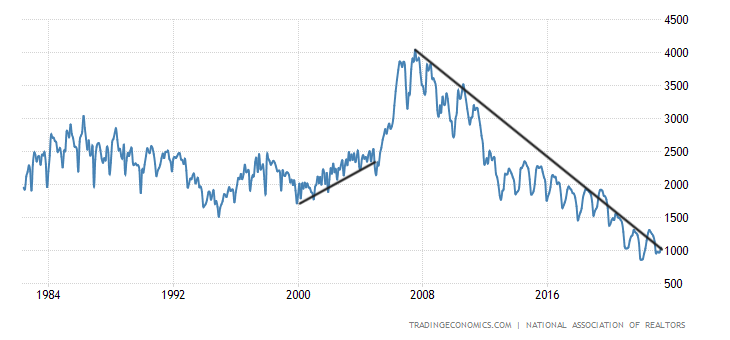

NAR overall Stock levels:

- Historically stock is in between 2-2.5 million

- The peak in 2007 was a bit over 4 million

- Presently we’re at 1.04 million

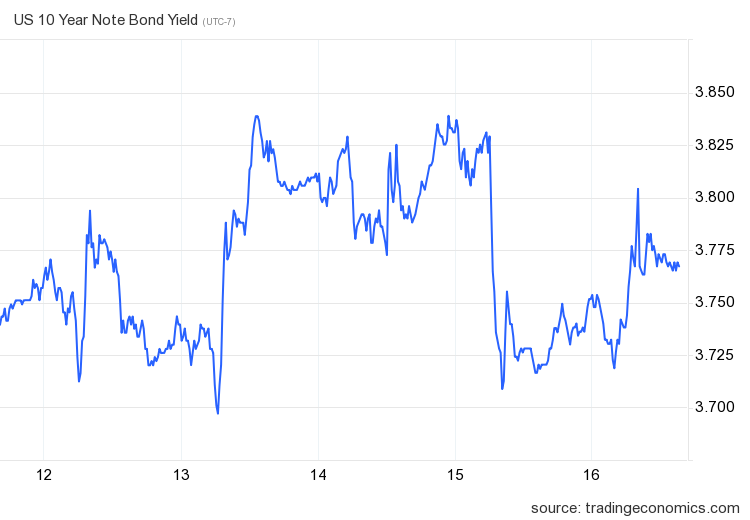

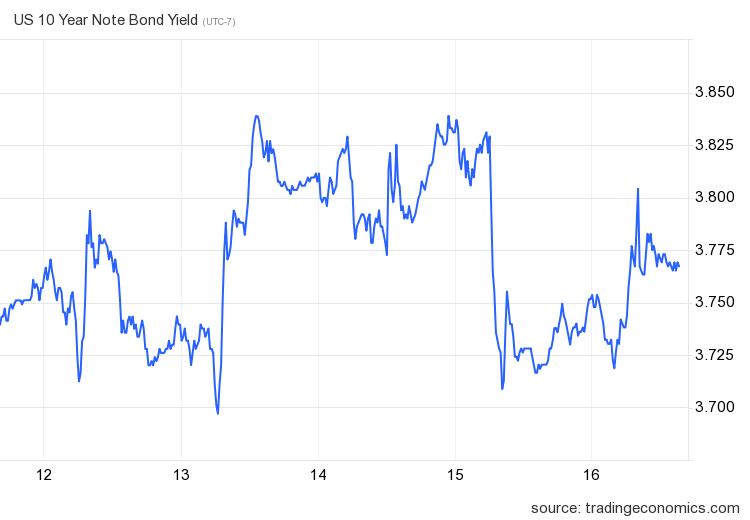

The 10-year yield and home mortgage rates

We simply had a remarkably dull week with home mortgage rates, considering we likewise had the CPI report and the Fed conference. Very little occurred recently with home mortgage rates, as they remained in an extremely tight variety in between 6.94% -6.98%.

Nevertheless, the bond market had some interesting action that I must describe. Initially, the bond market didn’t respond much to the CPI report; I discussed the report itself here, which still reveals the sag in the development rate of inflation.

Nevertheless, as I have actually kept in mind in previous weekly tracker short articles, we are having some challenging bond auction occasions given that the financial obligation ceiling action, which moved the marketplaces recently. The marketplace didn’t respond excessive to the Fed conference, something I spoke about on this podcast With all those occasions occurring recently, the chart listed below demonstrated how the 10-year yield acted.

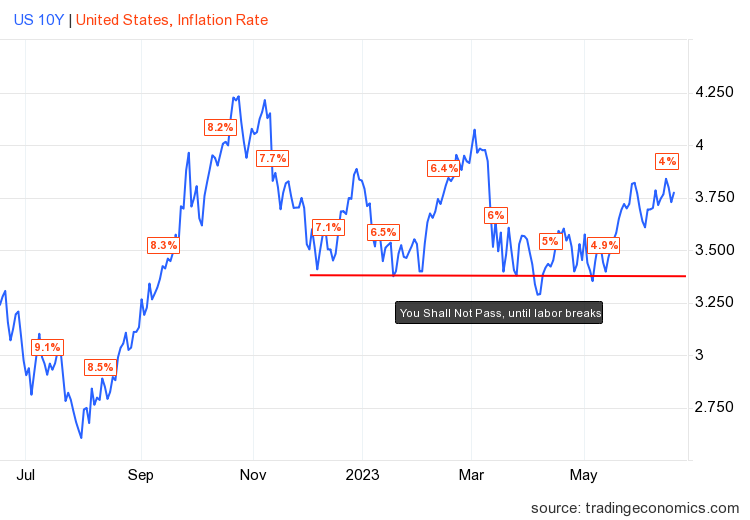

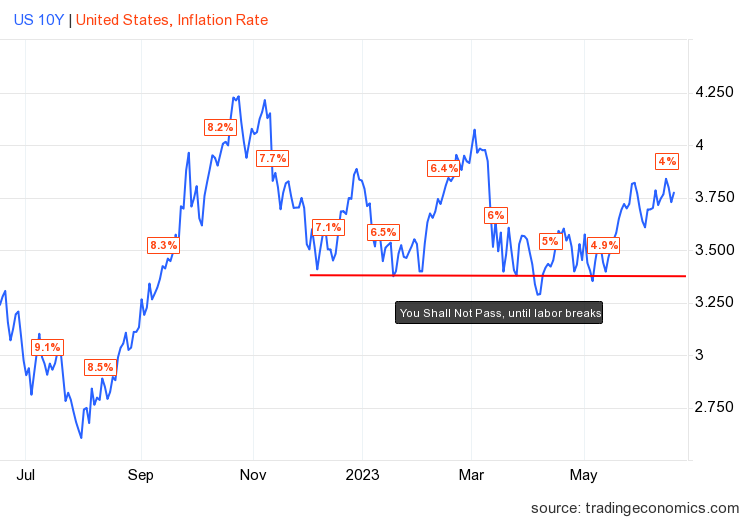

In my 2023 projection, I composed that if the economy remains company, the 10-year yield variety must be in between 3.21% and 4.25%, relating to home mortgage rates in between 5.75% and 7.25% As long as out of work claims pattern listed below 323,000 on the four-week moving average., the labor market is remaining company, which implies the economy is remaining company.

I have actually likewise worried that the 10-year level in between 3.37% and 3.42% would be tough to break lower. I call it the Gandalf line in the sand: “ You will not pass.” Yes, it may be corny, however I thought this level would be tough to break under, and Gandalf had the ideal line for this bond market call.

Up until now in 2023, that line has actually held up, as the red line in the chart listed below programs. Home loan rates have actually remained in the variety of 5.99% -7.14% Nevertheless, we do have some concerns in the home mortgage market.

Because the banking crisis began, the spreads in between the 10-year yield and 30-year set home mortgage rates have actually become worse, keeping home mortgage rates greater than typical. As revealed listed below, spreads made a visible turn when the banking crisis drama began and have not gone back to the pre-drama pattern. It will be a huge favorable for the real estate market when this information line returns to typical. Nevertheless, up until then, this has actually been an unfavorable for the U.S. economy.

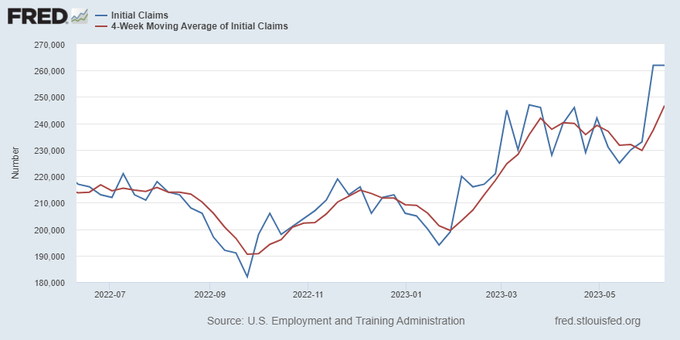

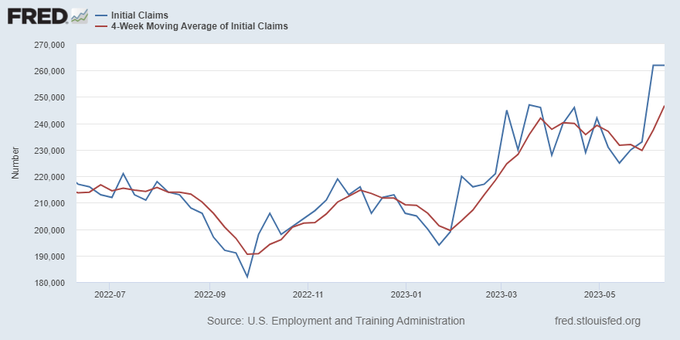

Another element of my 2023 projection is that if out of work claims break over 323,000 on the four-week moving average, the 10-year yield might break under 3.21% and head towards 2.73%. Recently we didn’t have much motion here. Nevertheless, as we can see below, the labor market, while still extremely healthy today, isn’t as tight as it utilized to be.

From the St. Louis Fed: Preliminary claims for joblessness insurance coverage advantages were bit altered in the week ended June 10, at 262,000. The four-week moving average increased to 246,750

The week ahead: More real estate information coming!

Today we have a series of real estate information being launched: Contractor’s self-confidence, real estate starts and the existing house sales report. Federal Reserve Chairmen Powell will likewise affirm to Congress today, which might produce fireworks. Naturally, I am constantly conscious of the out of work claims information to see if we can find more fractures in the labor market.

For real estate starts, we wish to see more conclusion of houses due to the fact that the very best method to handle inflation is constantly including more supply, and we have a great deal of 5 systems under building and construction quickly This is extremely essential due to the fact that without lease inflation removing once again, it’s difficult ever to have a repeat of the 1970s-style inflation.

So, let’s expect some much better real estate conclusion information today! The very best news for home mortgage rates is less inflation and the very best method to handle that is more supply.