franckreporter

BBCA vs. The Stalwart

The JPMorgan BetaBuilders Canada ETF ( BATS: BBCA) provides protection to over 82 stocks from the broad Canadian market. In spite of its fairly young age (BBCA made its listing launching just in August 2018), BBCA has actually handled to collect almost two times the AUM of the earliest Canadian-focused ETF in the market– The iShares MSCI Canada ETF ( EWC), which has actually been around for approximately 27 years now (AUM of $6bn vs $3.2 bn for EWC).

Whilst both portfolios cover a comparable variety of stocks (80-90 stocks) and are not vulnerable to quite churn (the yearly turnover ratio of both ETFs is small at just 5%), BBCA provides a couple of other structural advantages that might have slanted belief towards it.

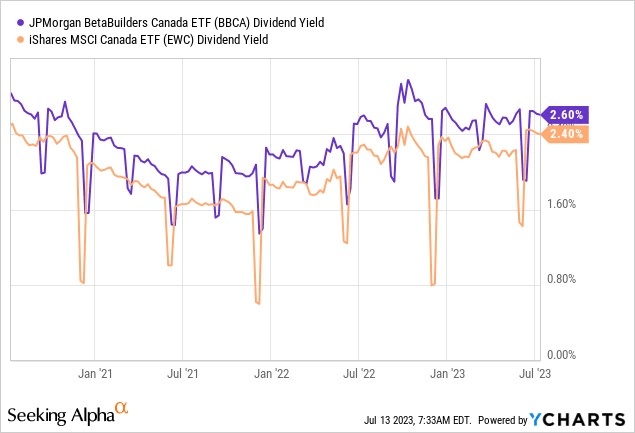

Mostly, it comes down to cost performance, and here, BBCA’s substantially lower cost ratio of 0.19% provides it an edge over EWC, which is unfavorably positioned, with an expenditure ratio of 0.5%. Financiers, will likewise likely value the remarkable yield differential available, which has actually been rather a constant aspect for the majority of durations throughout the last 3 years (presently it stands at 20bps).

YCharts

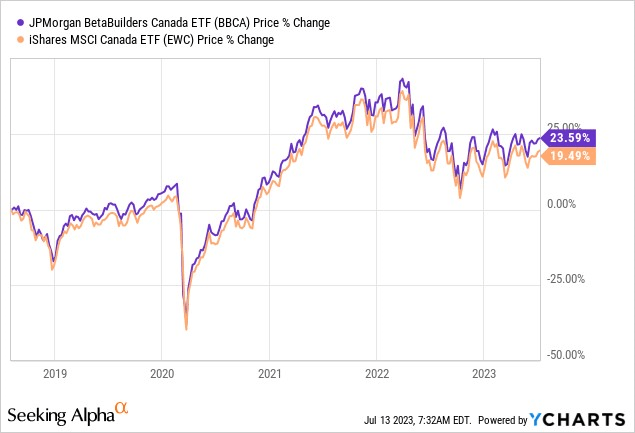

It definitely likewise assists that BBCA has actually constructed a credibility for surpassing EWC because its listing date, providing aggregate returns of ~ 24% (EWC’s returns throughout that time have actually can be found in at 19%).

YCharts

Macro Commentary

Hitherto, the Canadian economy has actually held up rather well, however the wheels might come off in the quarters ahead, especially thinking about the reserve bank’s unwillingness to pivot far from rate walkings.

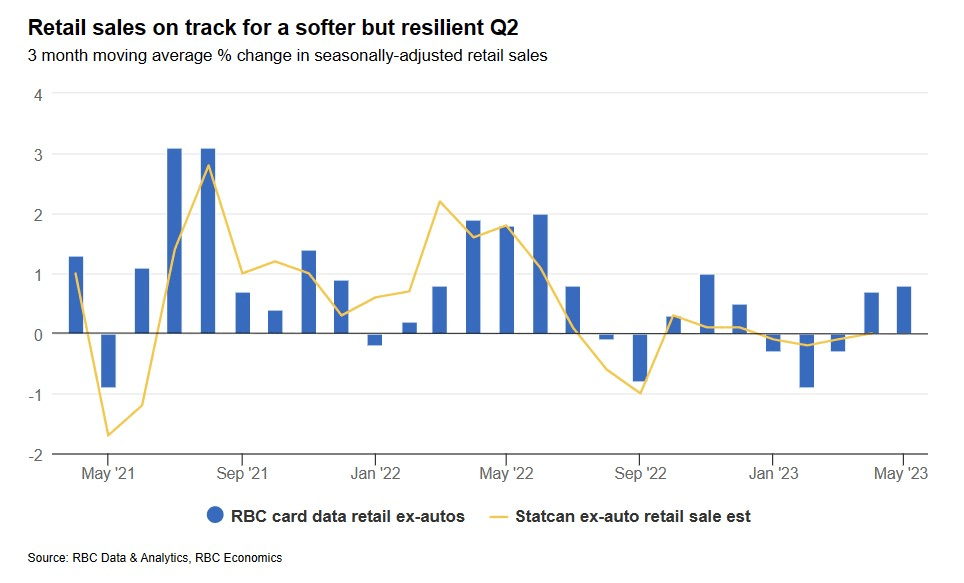

Whilst it has actually been motivating to keep in mind a decrease in heading inflation, the decrease hasn’t been broad-based, with several pockets within the CPI basket trending over mid-single-digit levels. On the other hand, the Canadian labor market likewise stays fairly resistant, with the current report highlighting how the economy included 60k tasks, 3x greater than what the street was anticipating. On the other hand, it likewise appears like customer costs in Q2 will likely end up on a motivating note with consecutive development seen throughout the quarter.

RBC

Fairly tough retail costs has actually been sustained by tough home wealth levels which have actually been growing for 2 straight quarters now.

Thinking about all these advancements, it was not a surprise to see the Bank of Canada lift policy rates yet once again by 25bps, taking it to 22-year highs (it had actually raised rates by a comparable figure last month, after a 5-month time out in between). Passive observers might now be vulnerable to believe that this would be the last of the rate walkings, however we definitely would not bank on it. Why so?

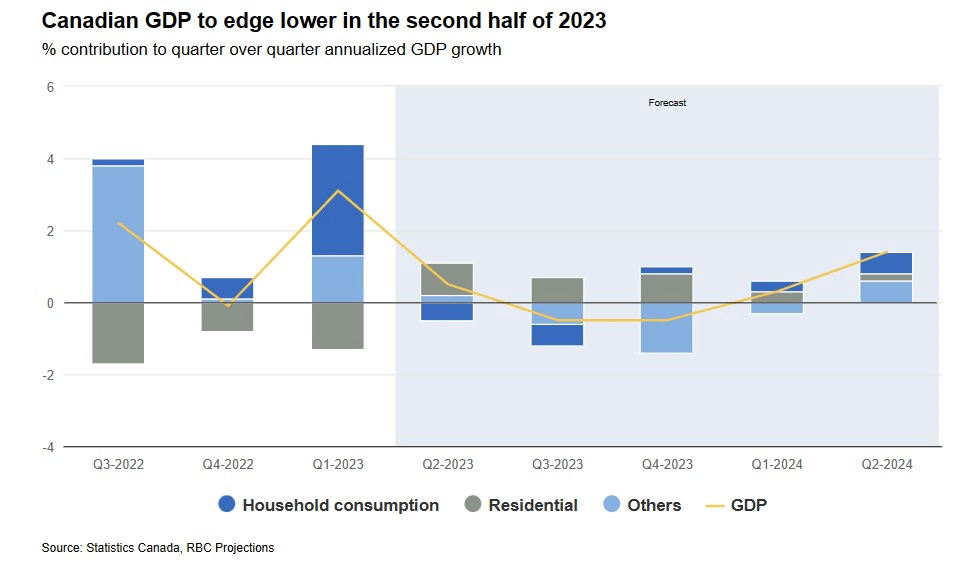

Well, the Bank of Canada had actually intended to close FY25 with inflation listed below their 2% target, however due to the fact that of the stickiness of particular elements, they have actually been required to extend their target by another 6 months to mid-FY25 (Likewise keep in mind that inflation in FY24 will likely be around the 3% annualized levels). With additional rate walkings on the cards, dangers to the GDP development trajectory in H2-23 seeks to have actually grown.

RBC

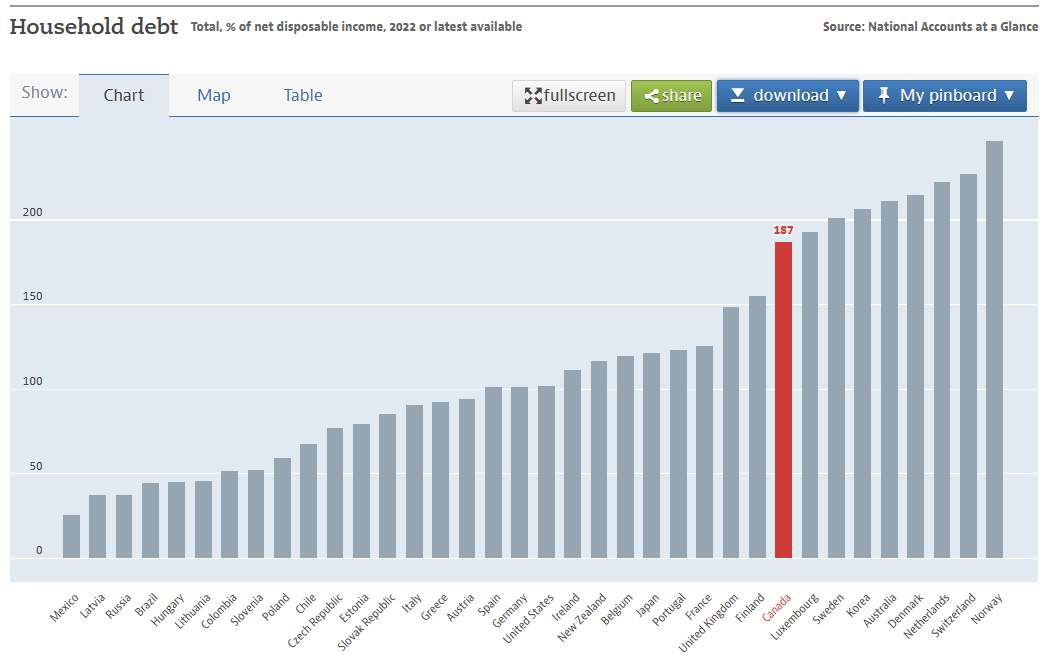

The more important problem likewise focuses on how greater rate of interest might asphyxiate the debt-servicing abilities of Canadian families. Even prior to these walkings, Canadian families represented among the most indebted pockets throughout the world (with home financial obligation to non reusable earnings of 187% in 2015).

OECD

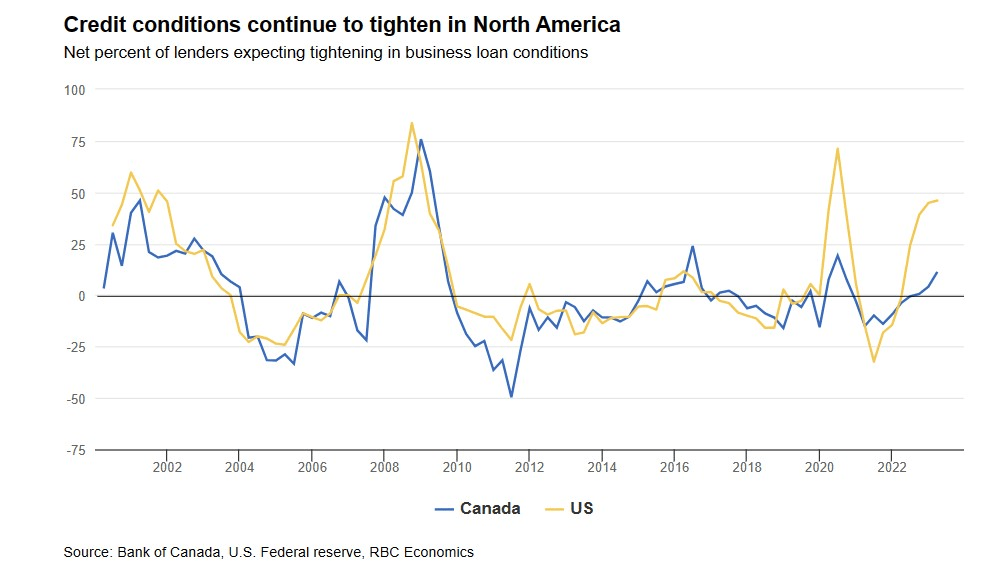

A greater limit of policy rates in the face of an exceedingly levered home base will definitely not contribute for the potential customers of Canadian banks (which by the way control BBCA’s portfolio with an aggregate weight of 35%). These banks have actually been tightening their requirements in current durations, however it is still not rather at the very same limit as their United States equivalents

RBC

Likewise think about the obstacles related to refinancing of their home mortgage portfolio, with over $250bn worth of home mortgages due to be restored next year at much greater rates (for context, the drifting rate home mortgages are now costlier by 70% vs levels seen in October 2021 when rates were at record lows).

Whilst it is motivating to keep in mind that the Canadian banking regulator means to execute more rigid capital standards to alleviate the dangers related to the home mortgage portfolio of these banks, advancements like this will just moisten the potential customers of greater investor circulations, which might trigger some financiers to avert from Canadian financials.

Closing Ideas

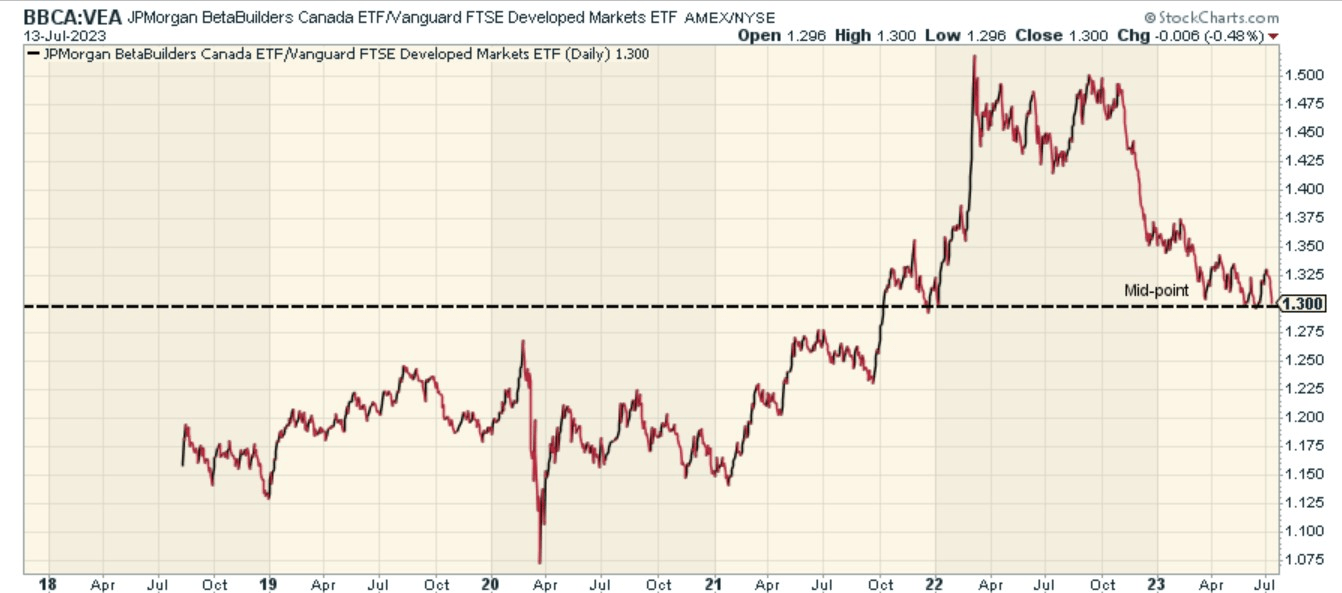

As far as the assessment background is worried, Canadian equities do not seem wonderfully priced. For context, BBCA’s constituents are presently priced at a forward P/E of 13.6 x, which equates to an 8% premium over the matching multiple of the Lead FTSE Established Markets ETF ( VEA).

Would BBCA discover as an appealing rotation play within the industrialized market area? Well, that chart listed below recommends there’s no terrific reward to turn into BBCA at this moment as its relative strength ratio versus VEA is bang in line with the mid-point of its trading variety.

Stockcharts