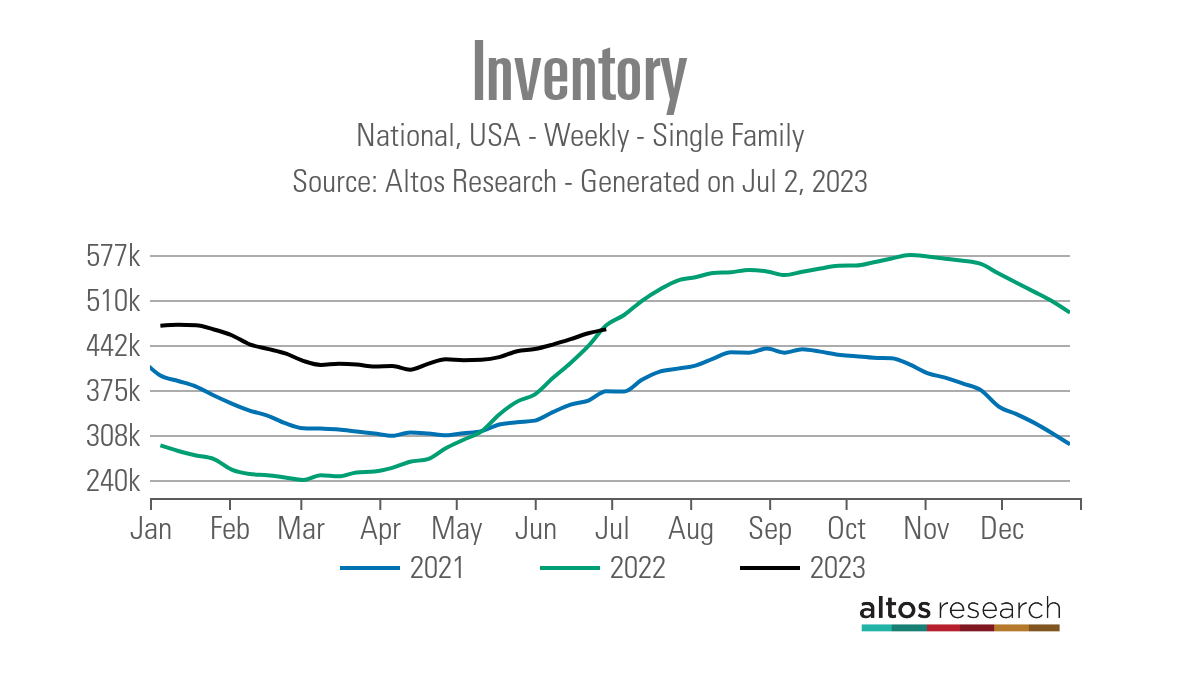

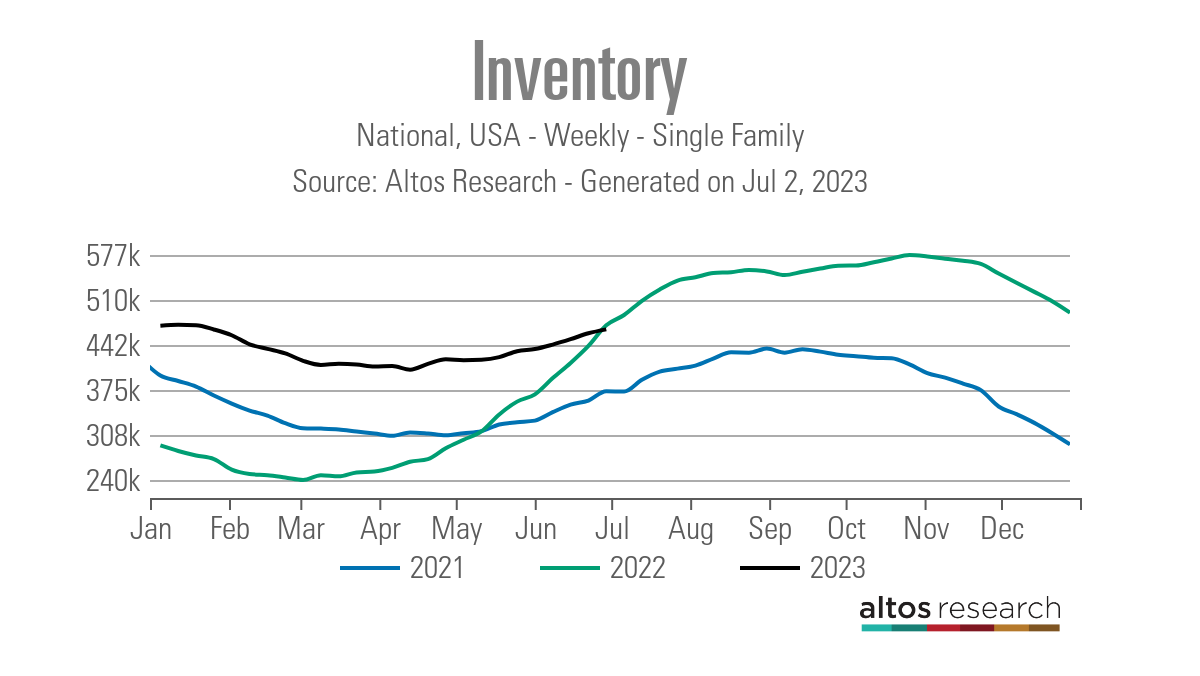

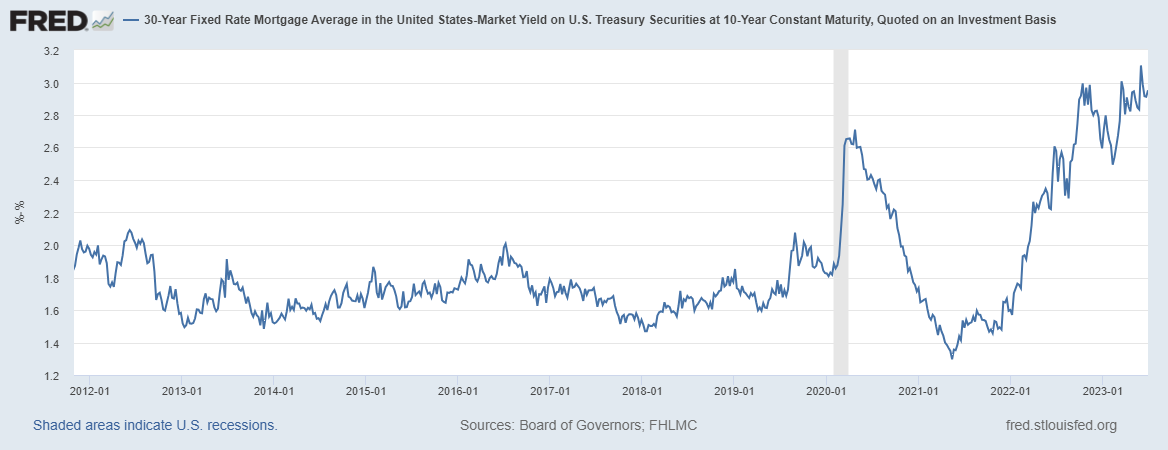

Real estate stock lastly broke under 2022 levels recently. To provide you a concept how various this year is from in 2015, recently in 2022, active listings grew 30,940 while this year they just grew 5,848. Home mortgage rates increased recently after the better-than-anticipated out of work claims information however even with greater rates, we likewise had a 3rd week of favorable purchase application information.

Here’s a fast rundown of recently:

- Active stock grew by a frustrating 5,848 weekly

- Home mortgage rates exceeded 7% once again after much better labor information

- Purchase application information revealed 3% development week to week

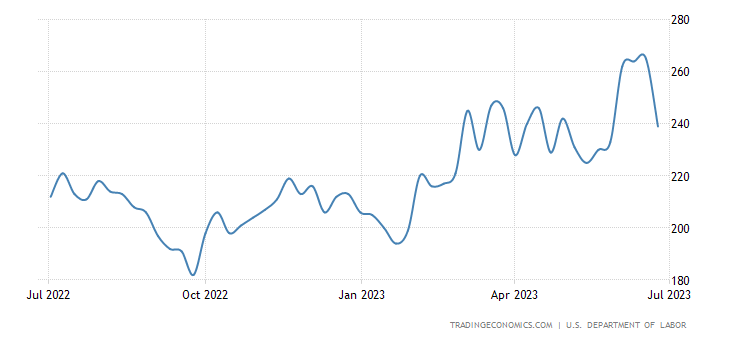

Weekly real estate stock

On Might 15, I went on CNBC and discussed how stock development in 2023 looked like a zombie from the program The Strolling Dead, gradually attempting to increase from the tomb. Because May 15, that pattern has actually continued to the point that stock in America is now unfavorable year over year.

We have actually typically gone over that the real estate market characteristics altered beginning Nov. 9, 2022, and today you can see the outcome of that vibrant shift as stock is now unfavorable versus the 2022 information– all prior to July fourth. I just recently evaluated this insane duration on the HousingWire Daily podcast, explaining about what occurred in real estate over the in 2015.

- Weekly stock modification (June 23-30): Stock increased from 459,907-465,755

- Very same week in 2015 (June 24-July 1): Stock increased from 441,106 to 472,046

- The stock bottom for 2022 was 240,194

- The stock peak for 2023 up until now is 472,688

- For context, active listings for today in 2015 were 1,183,390

Seeing unfavorable year-over-year stock prior to July 4 would be a huge offer if in 2015 wasn’t so insane. Nevertheless, I require to put some context into what occurred in 2022. In March of 2022 we had the most affordable stock levels ever tape-recorded in history. Then in a brief quantity time, we had the greatest and fastest home loan rate spike in history, which assisted in the greatest 1 year crash in house sales in history, which assisted stock grow faster than regular in 2022.

So the truth that real estate need supported and stock is now unfavorable year over year requires the context that 2022 was an unique occasion. As you can see in the chart below, 2023 stock development is extremely sluggish compared to 2022.

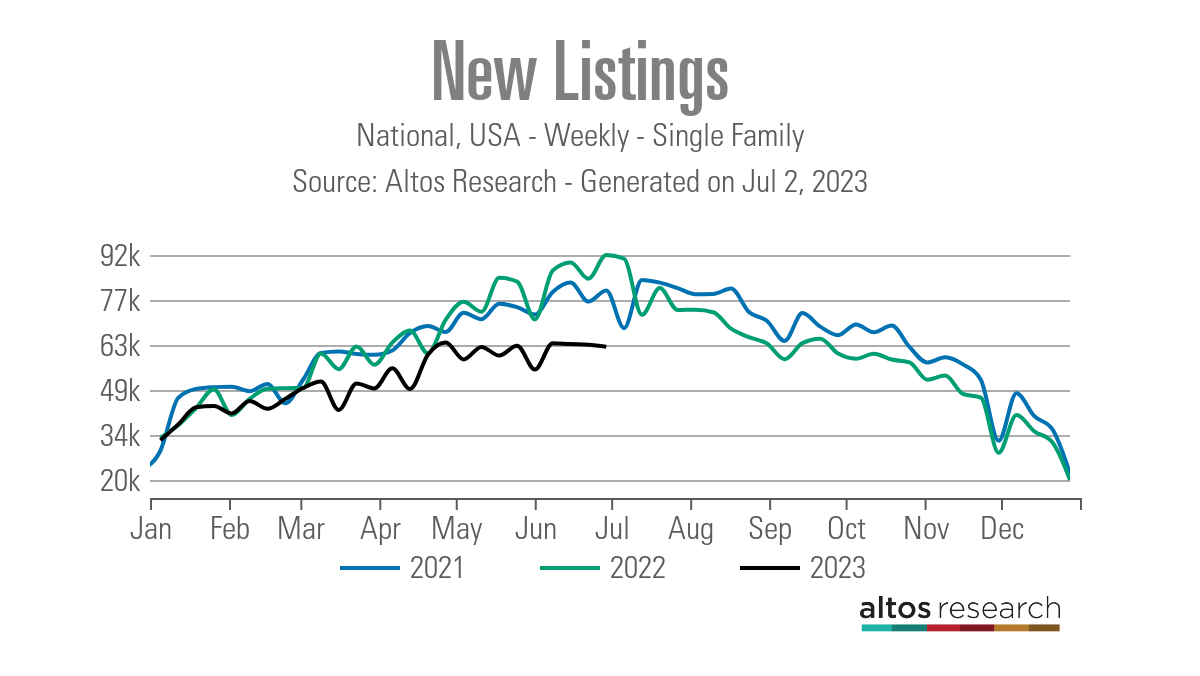

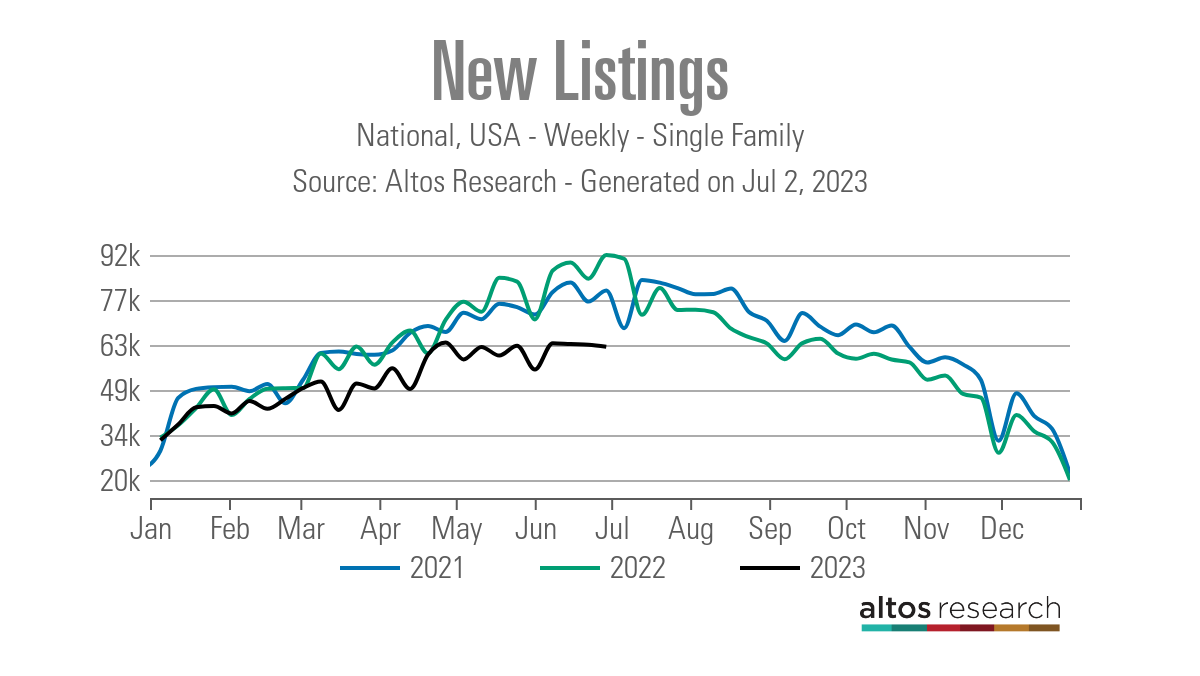

The other huge story with real estate stock is that brand-new listing information has actually been trending unfavorable year over year because completion of June 2022. A standard seller is likewise a standard purchaser, and particular house owners have actually declined to purchase their next house with home loan rates above 6%.

We had brand-new listings development from 2021 to 2022, however that’s not the case this year. This is another variable adding to slow stock development, which has actually now turned unfavorable in the weekly listings.

Compare the brand-new listings information recently to the very same week recently:

- 2023: 62,466

- 2022: 91,530

- 2021: 80,289

My issue recently is that we have actually seen 4 straight weeks of moderate decreases and will head into the seasonal decrease duration of brand-new listings. This is one information line I will track like a hawk due to the fact that it will be an unfavorable for the real estate market if this information line makes a visible year-over-year decrease pattern in the 2nd half of 2023.

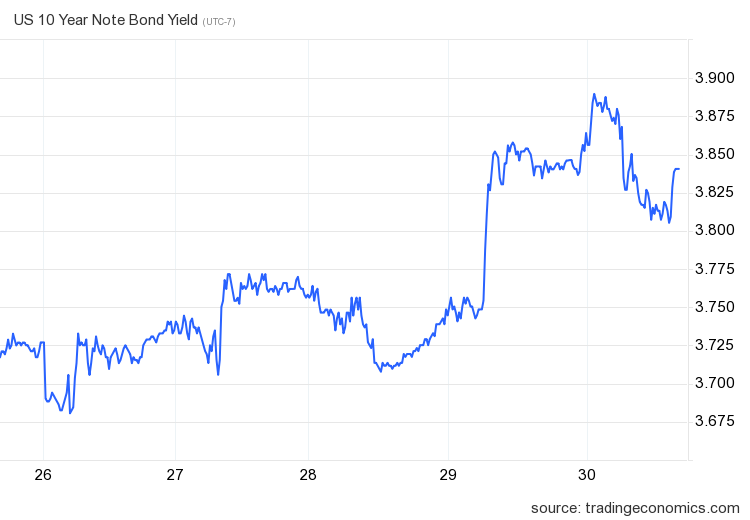

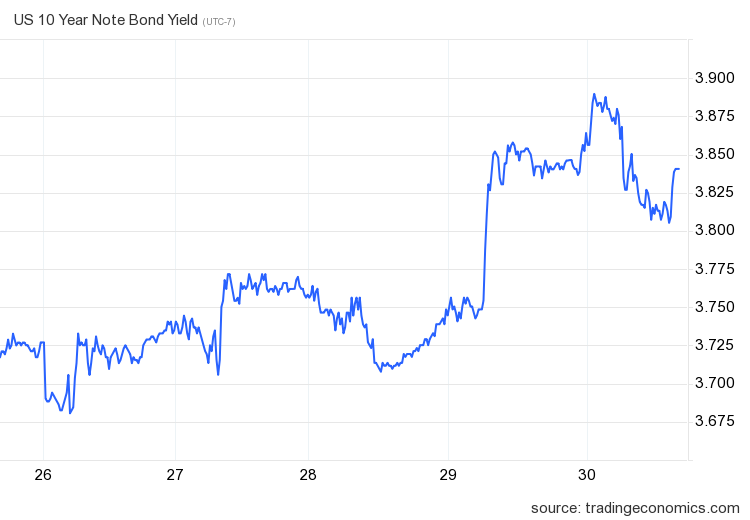

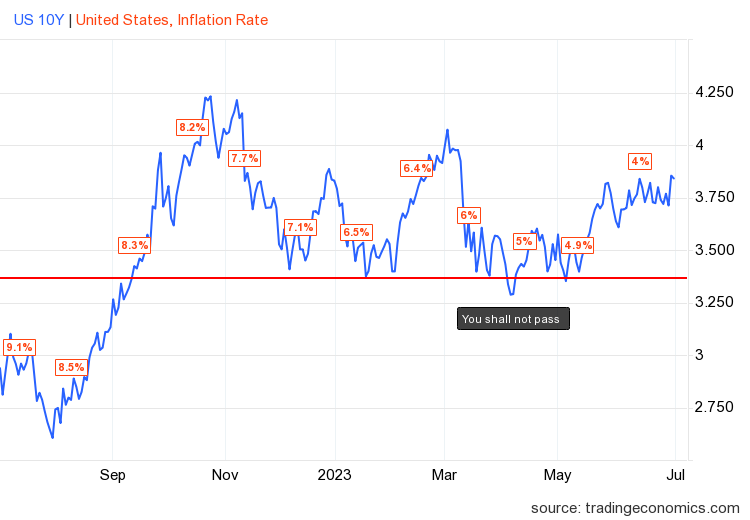

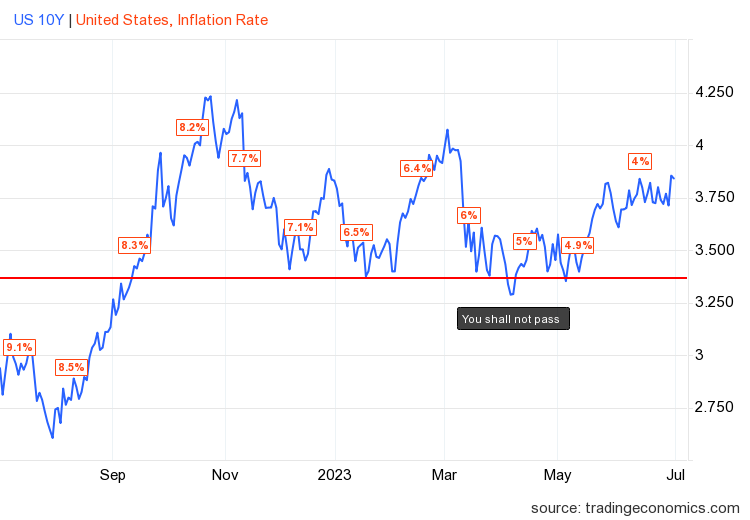

The 10-year yield and home loan rates

For those who have actually followed the weekly Real estate Market Tracker posts, I constantly concentrate on out of work claims information as it’s the important information line at this moment of the financial cycle for me and my projection in 2023 for home loan rates.

Recently we had a huge relocation in the 10-year yield due to the fact that out of work claims was available in much better than prepared for, and bond traders were captured off guard selling bonds on the news and sending out home loan rates above 7% once again. As you can see in the chart below, that huge spike was truly about out of work claims improving.

The following day, the PCE inflation information revealed a cooling off in heading inflation year over year. Core PCE inflation is a bit more sticky than heading inflation, nevertheless, bond yields fell after that report and recovered at the end of the day.

In my 2023 projection, I composed that if the economy remains company, the 10-year yield variety must be in between 3.21% and 4.25%, corresponding to home loan rates in between 5.75% and 7.25% As long as out of work claims pattern listed below 323,000 on the four-week moving average, the labor market remains company, which suggests the economy stays healthy. Unemployed claims have actually remained listed below this variety all year, and task openings are still at 10 million.

I have actually likewise worried that the 10-year level in between 3.37% and 3.42% would be difficult to break lower. I call it the Gandalf line in the sand: You will not pass. The setup for the 10-year yield to remain in the variety is undamaged.

The counter to my 10-year yield variety would be if the economy here or worldwide begins to speed up greater; that would be a legitimate facility to get the 10-year yield above 4.25%. Considering our economy this year, the 10-year yield and home loan rates look about best to me.

Now the something that has actually altered in 2023 is that because the banking crisis, the spreads in between the 10-year and home loan rates have actually aggravated, making home loan rates greater than I prepared for versus the 10-year yield, which is not a favorable for the real estate market.

We have not seen anything in the information revealing that it’s been enhancing just recently. This is a huge offer as we have actually seen real estate stock not get much traction with greater rates and ideally in the future, lower rates can attract some sellers to move.

On out of work claims information, I constantly worry utilizing the four-week moving average with this information line due to the fact that we do have times when this information line can get chaotic week to week. For that reason, I just think the low out of work claims print when I see weeks of this information line improving. So, it will be important over the next 2 weeks to see if this decrease was a one-time blip in the information, which we have actually seen from time to time. As you can see below, that was a substantial drop week to week, which looks unusual to me.

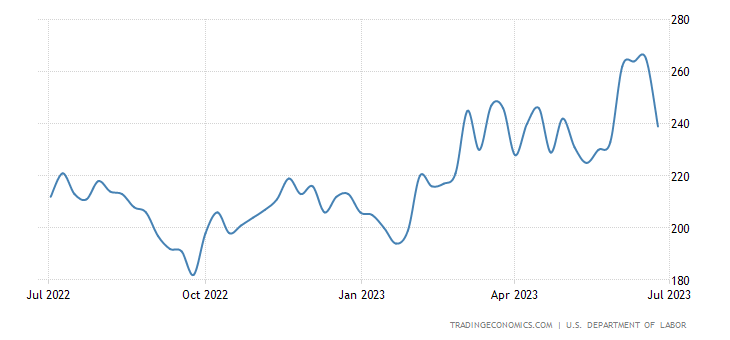

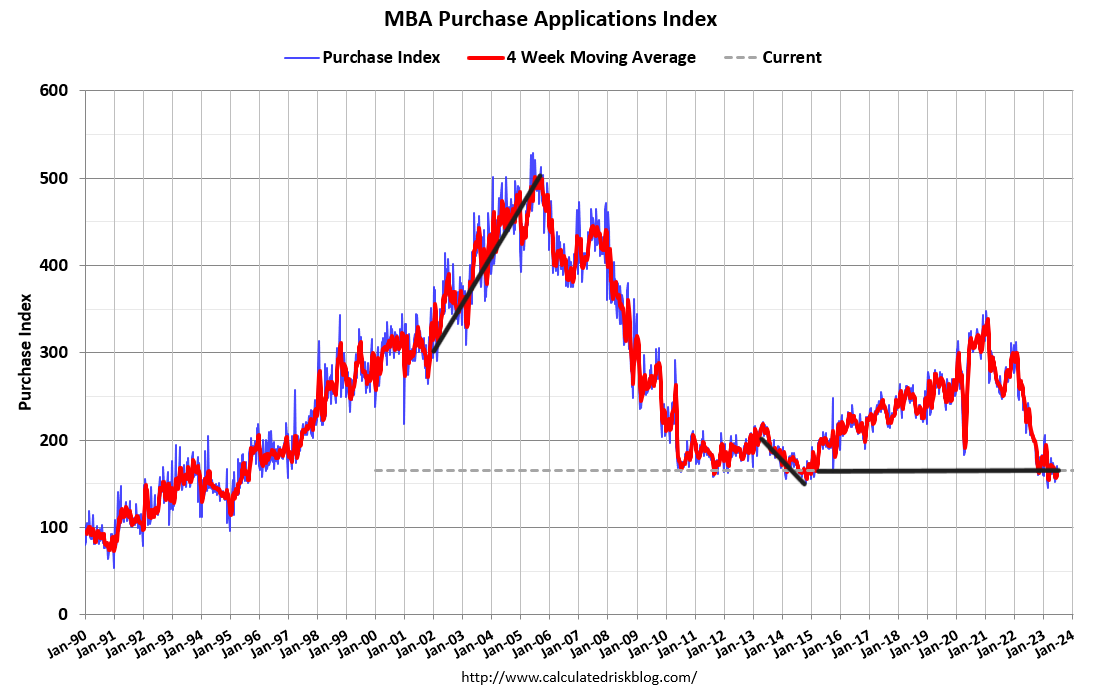

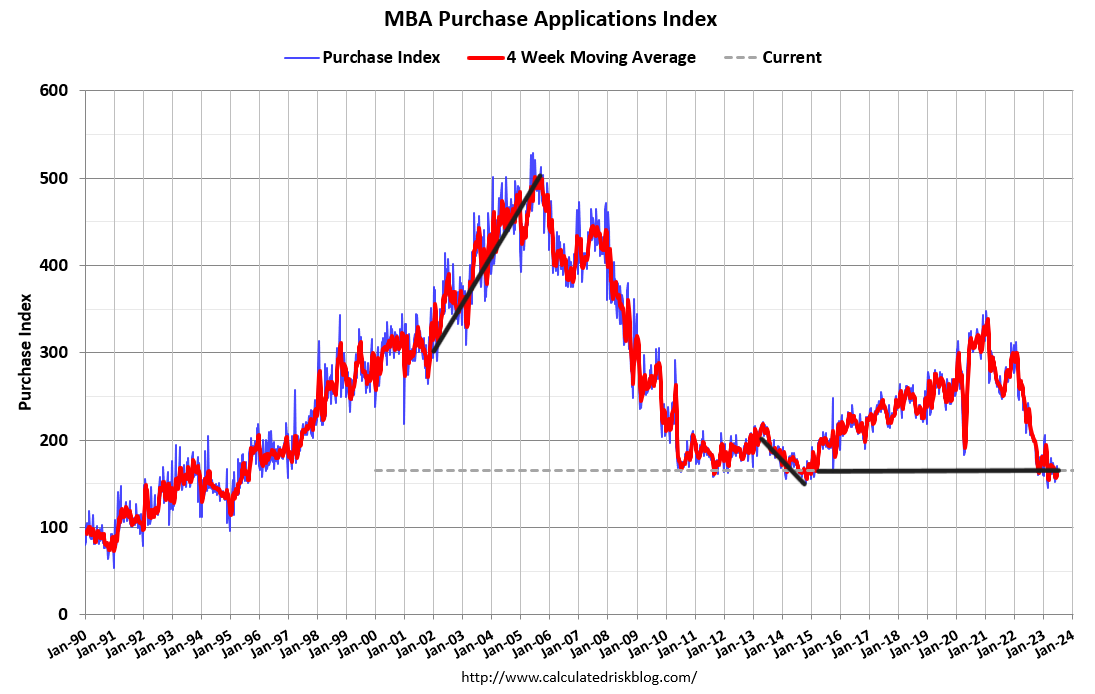

Purchase application information

Purchase application information has actually shocked individuals with 3 weeks in a row of development, while home loan rates have actually been near 7% throughout this duration. This now makes the favorable count because Nov. 9, 2022, 20 favorable prints vs. 11 unfavorable prints. The year-to-date numbers are 13 favorable vs. 11 negatives after making some vacation changes to the information line.

What do these numbers suggest? They simply suggest that real estate information has actually supported; absolutely nothing in the information reveals good development after that very first excellent relocation from November to February. Nevertheless, the truth that real estate need has actually supported is a huge offer due to the fact that in 2015, we did have a waterfall collapse in the information, as displayed in the chart below. The only drawback to this is that we have not had the real estate stock development I would like.

Now the year-over-year decrease was down to -21%, which was the most affordable because Aug. 24, 2022. Nevertheless, all of us need to bear in mind that the 2nd half of 2023 will have a lot easier compensations, so even if need remained the very same the remainder of the year we will have some favorable year-over-year information at some time.

Take care in checking out excessive into the much better year-over-year information we will see in the future. The most current pending house sales print was available in as a miss out on from price quotes, however the existing house sales information is still trending in the variety I believed it would remain in because I thought that initially huge print we had a couple of months back was going to be the peak for many years. When need is returning in a huge method, purchase apps will be favorable for a bulk of the weeks as we are working from such low levels today traditionally.

The week ahead: Jobs, tasks and tasks information

Yes, it’s tasks week when again and with 4 labor reports turning up on this brief vacation week, we’ll have the ability to see if the Federal Reserve is getting what it desires– a softer labor market. Just Recently, Fed Chair Powell when again worried that the labor market is too tight which softer labor is the method to get inflation to the Fed’s 2% core PCE target.

Well, we have 4 reports today: the task openings information (SHOCKS), the ADP tasks report, out of work claims and the huge one on Friday– the BLS task report– so we’ll see what occurs.

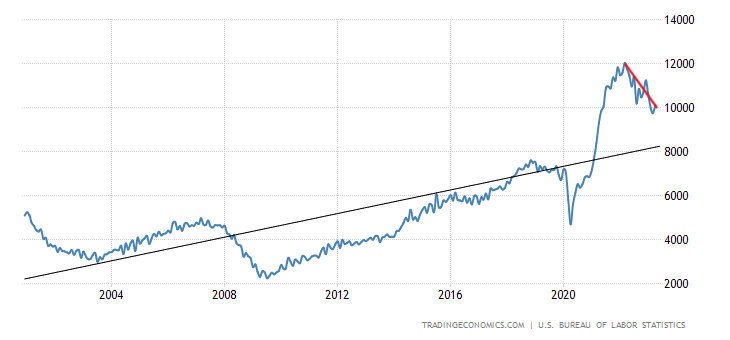

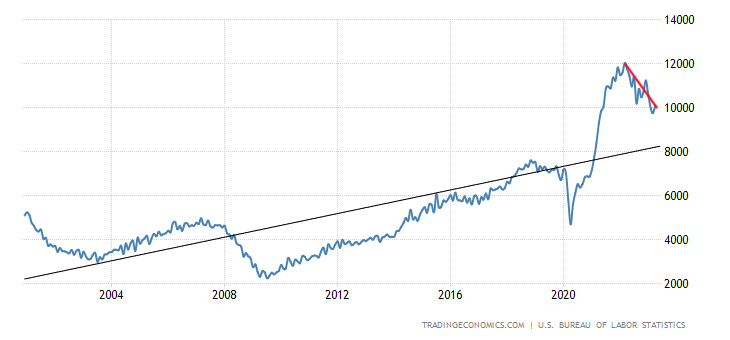

A lot of my COVID-19 healing design was based upon the labor characteristics being much various now, because I was the only individual discussing task openings getting to 10 million in this healing. Today as I compose this, we are still at 10 million task openings, as the chart listed below programs.

I have a company belief that the Fed does not fear a huge job-loss economic crisis as long as task openings are this high. What they have actually delighted in seeing is wage development cooling off, as displayed in the BLS task reports for 18 months now. So, for today, we constantly concentrate on out of work claims information over whatever else, however bear in mind the task openings information because the Fed wishes to see this decrease, and the wage development in the BLS tasks report information.