The development rate of inflation has actually been succumbing to a year, however home loan rates are still near multi-decade highs. Why? While it holds true that home loan rates generally fall together with inflation, I thought 2023 was going to have to do with the labor market. This was the core facility of my 2023 projection, therefore far it has actually worked.

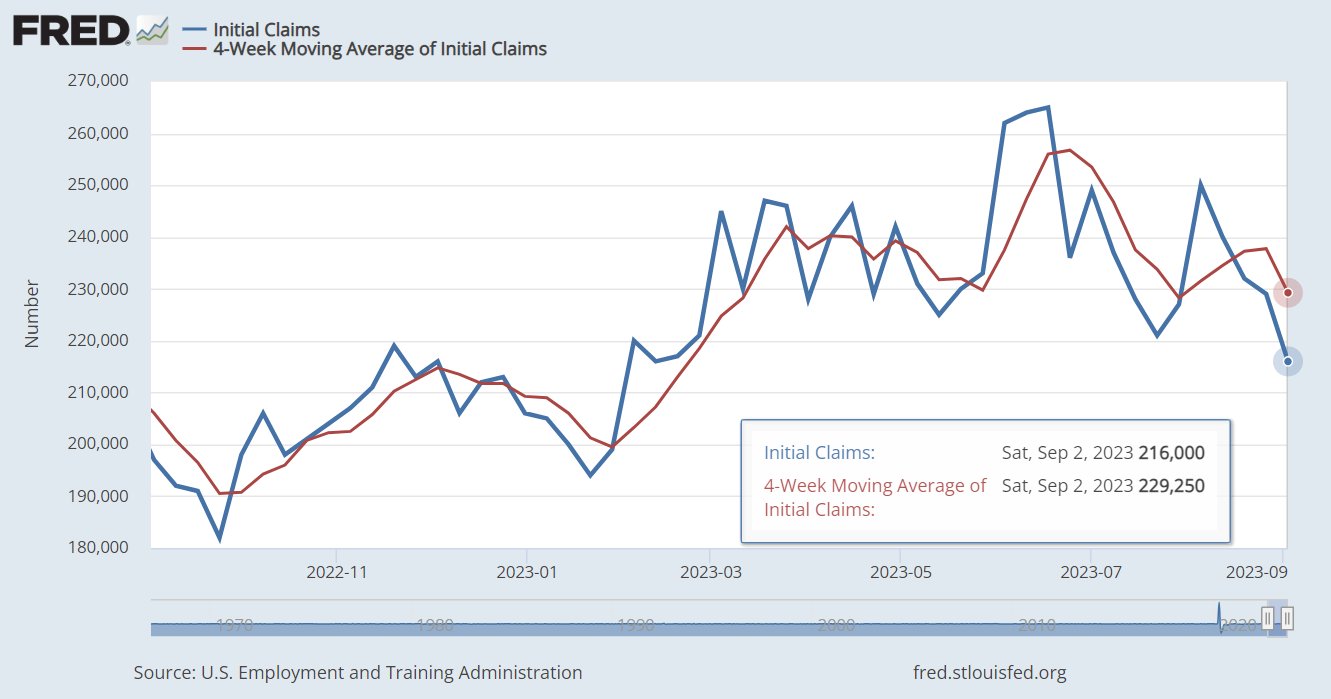

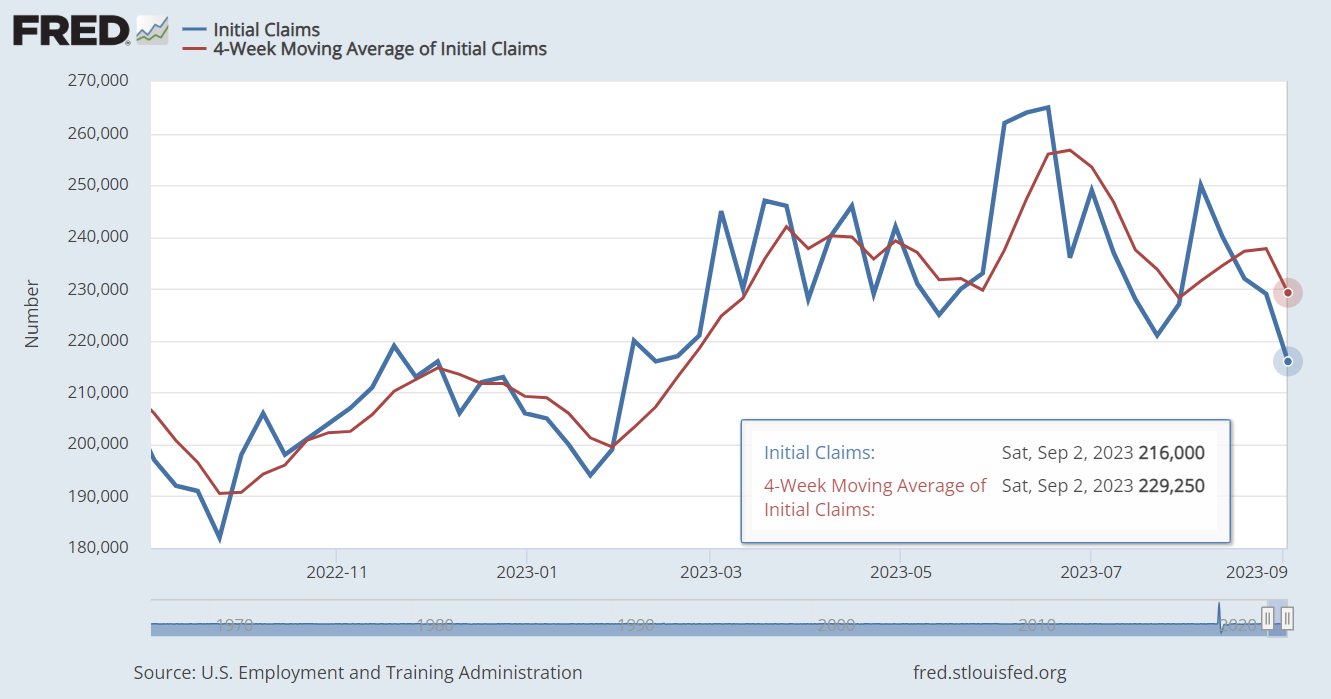

In my 2023 projection, I set the variety on the 10-year yield in between 3.21% -4.25%, stressing that the bond yields can go lower than 3.21% just if the labor market breaks– which would need unemployed claims to discuss 323,000 on a four-week moving average. The labor market is not as tight as it utilized to be, however unemployed claims are not breaking either. As revealed listed below, 229,250 on the 4-week moving average is traditionally lacking.

From the Fed: In the week ended Sept. 2, preliminary claims for joblessness insurance coverage advantages decreased by 13,000 to 216,000, the most affordable level considering that February. The four-week moving typical decreased by 8,500 to 229,250

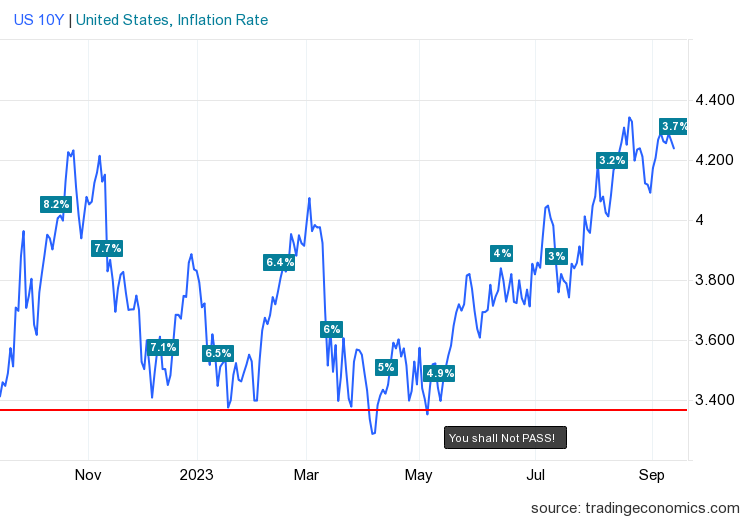

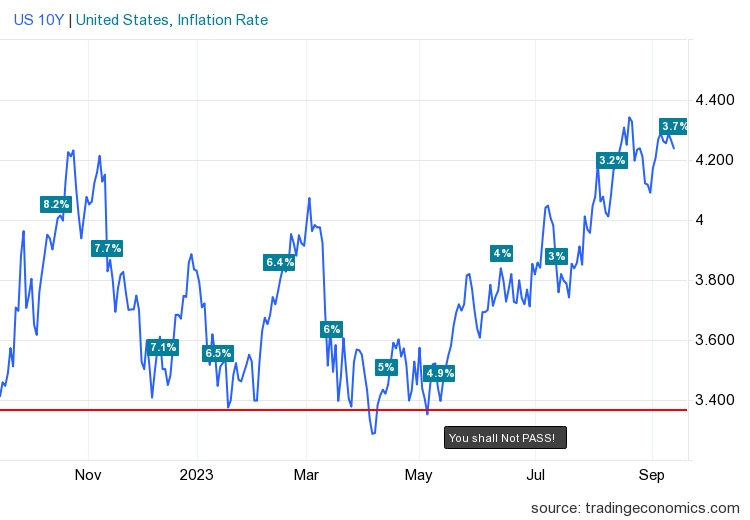

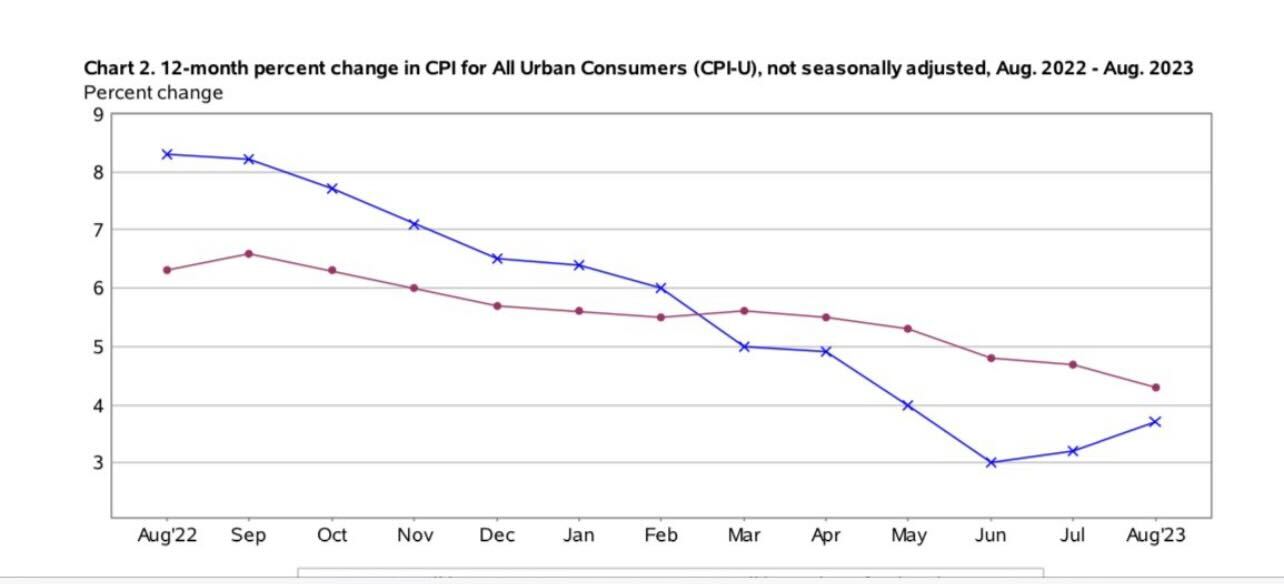

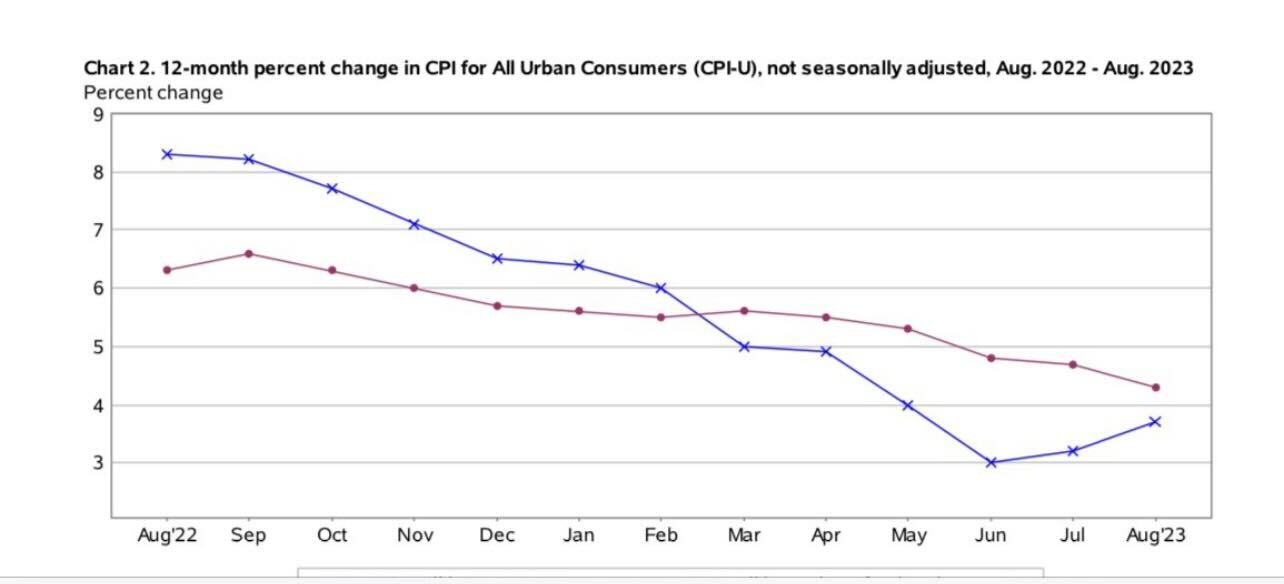

After today’s CPI inflation report, we can now take a look at a 1 year information line set comparing the 10-year yield and the development rate of inflation to see that we had lower home loan rates with hotter inflation information. While the information listed below is heading inflation, not core inflation, we have actually made great development from the 9% plus year-over-year inflation development information we had in 2015.

What do we think of home loan rates and inflation now? Let’s have a look, considering that one year ago today, I went on CNBC and spoke about how the development rate of leas cooling down would be a 2023 story, and it’s an excellent one for inflation.

Today’s CPI report was firmer than anticipated, however the core disinflation story stays undamaged and this is essential for the Fed and what they will think of in the future.

From BLS: The Customer Rate Index for All Urban Customers (CPI-U) increased 0.6 percent in August on a seasonally changed basis after increasing 0.2 percent in July, the U.S. Bureau of Labor Data reported today. Over the last 12 months, the all-items index increased 3.7 percent prior to seasonal modification.

As revealed listed below, heading inflation has actually increased over the previous 2 months as oil rates have actually increased. Nevertheless, core inflation is still in a drop. The Fed has actually constantly worried that core inflation is essential, so although we made much better development with heading inflation, that does not matter to them as much as core inflation.

A longer take a look at core inflation, where the Fed focuses its energy, reveals a great deal of development from in 2015, however it’s still traditionally high compared to COVID-19 patterns.

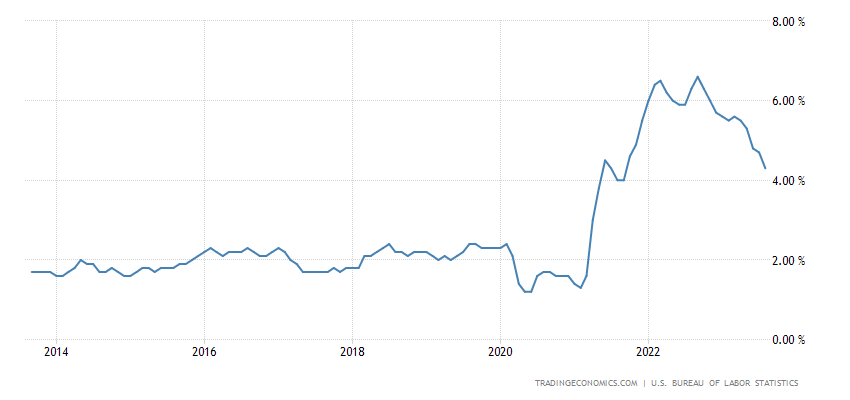

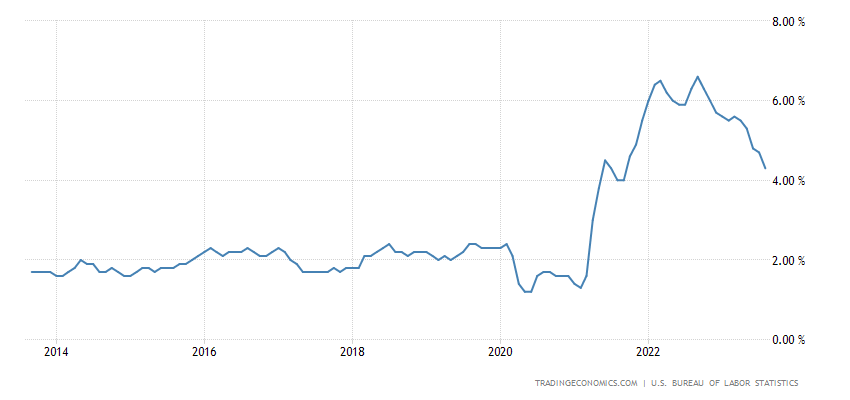

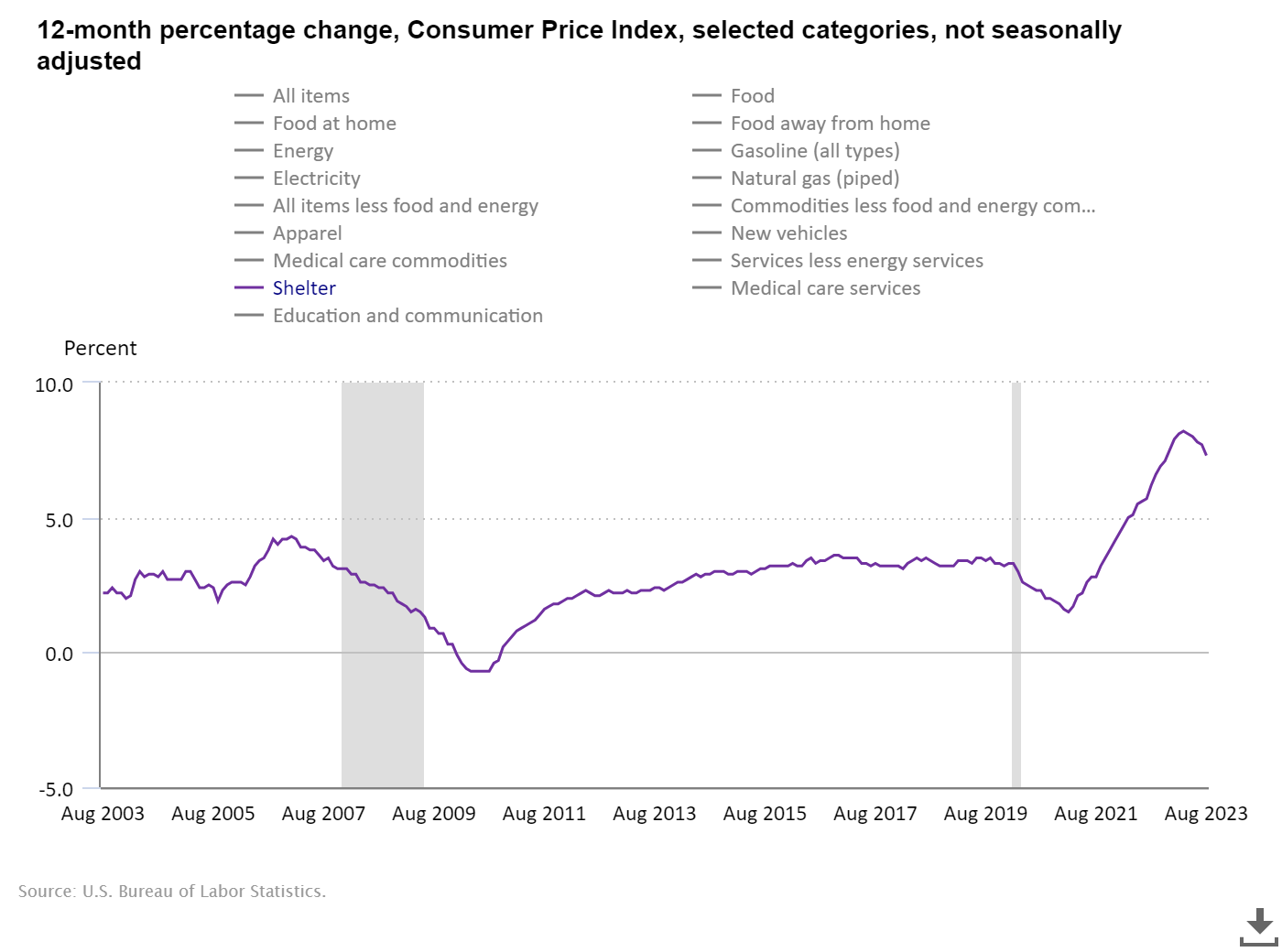

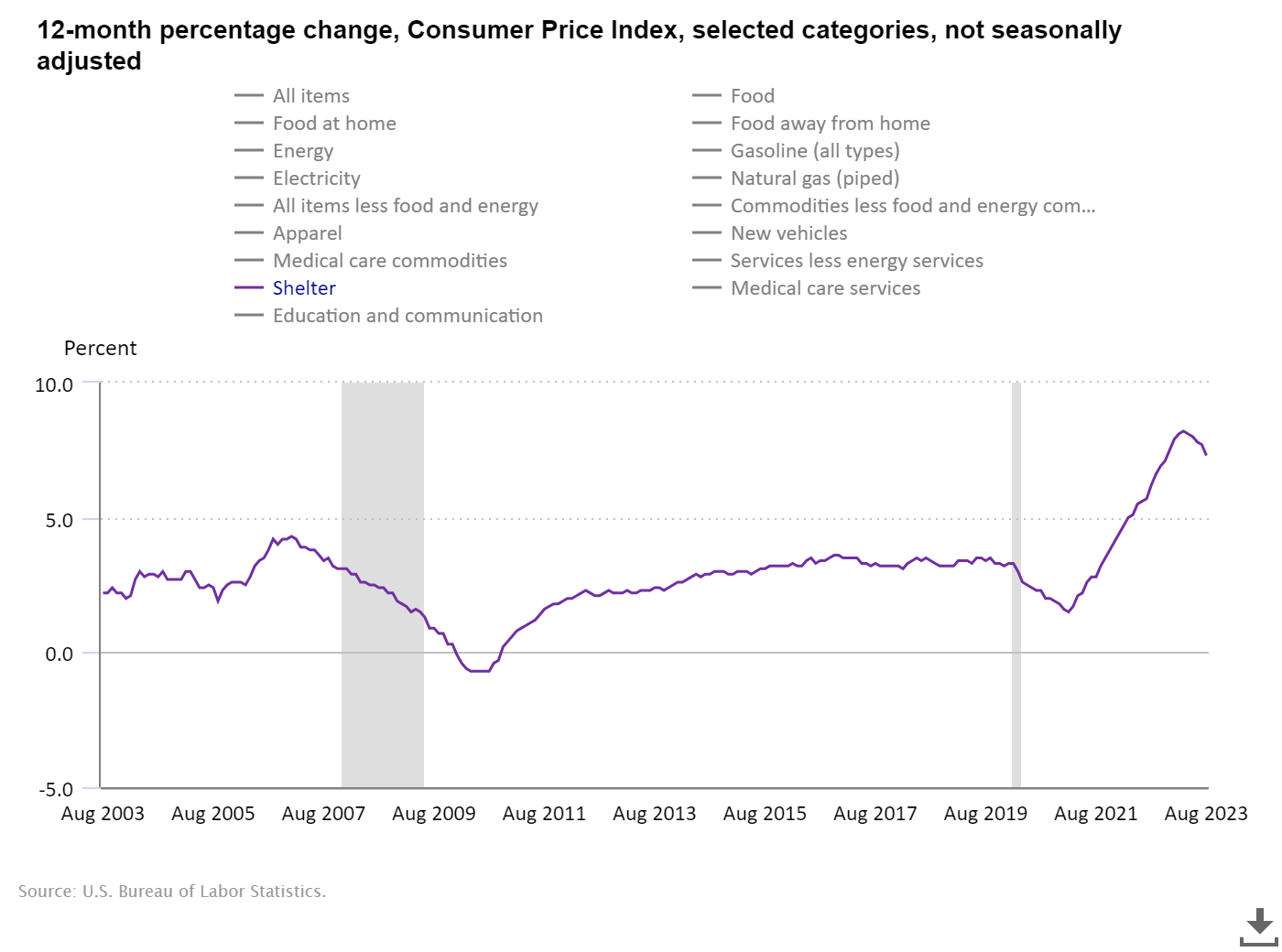

Likewise, the greatest part of core inflation is shelter inflation, which has legs to go lower for much more months. This information is much lower in real-time, so the core inflation information isn’t far from the 2% that the Fed targets. The Fed understands this, too.

Now, why is inflation information more crucial heading out? The Fed has actually discussed rate cuts next year, even without a task loss economic crisis, due to the fact that they think rates are presently extremely limiting with the inflation development rate. Now, as long as the inflation development rate falls, they will cut rates a bit to guarantee the U.S. does not enter into an economic downturn where they will need to cut more than they like. So, for the very first time in a while, the foundation has actually been laid for a rate cut with the development rate of inflation falling.

For 2023, the essential information line I was tracking was unemployed claims, much more than the inflation development rate. Next year will be various. As I am composing this today, the 10-year yield is at 4.25%, and we are at the peak of the projection for 2023. Entering into next year, we do have a great deal of essential financial information to track, however for the very first time, we can see we can get rate cuts without a task loss economic crisis.

This is why it is very important that the development rate of inflation is falling, however it will affect the Fed and home loan rates more in 2024 than 2023.