Antony Velikagathu

Euronav ( NYSE: EURN) has actually sealed its position as a leading entity in the shipping sector, regularly providing remarkable monetary outcomes, astute fleet enhancements, and a forward-thinking action to moving international market patterns. As one of the world’s most substantial owner/operators of VLCCs, EURN boasts a fleet with a DWT-adjusted typical age going back to 2016 and an average age of 7.5 years. This makes EURN’s fleet among the most contemporary in the market. Offered this, we forecast that EURN will keep its generous dividend payment method for the coming quarters.

An often-overlooked consider the shipping market is the age of the typical oil tanker. A considerable percentage of the international fleet is aging, and there’s been an obvious absence of brand-new integrate in current years. This older typical age, combined with the lack of brand-new vessels, puts business like EURN in a beneficial position. They take advantage of minimized competitors and can command premium rates, specifically provided the increasing regulative pressures and effectiveness needs that older vessels battle to fulfill.

We promote for a portfolio mix that consists of Oil Tanker business like STNG, FRO, INSW, GASS, and EURN This mix deals an engaging interaction of Price/Net Possession Worth discount rates and constant dividend inflows. Our recommendation for EURN acquisition comes from the present momentum in the Oil Tanker sector, the sophisticated age of the international fleet, the strong prices patterns, both in rate terms and the tanker secondary market, and the benefits of a more youthful fleet. We set a Rate Target for EURN at $20, aligning it with other market frontrunners.

Current Efficiency

In Q2 2023, Euronav reported a net earnings of $161.8 million, matching the robust efficiency from Q1. With an utilize ratio at 47.5% and a prepared balance sheet, the business’s monetary stability stays good, preparing it for even difficult tanker market conditions. Euronav’s money and short-term financial investments are around $165 million, constant with patterns from current years. We prepare for that any additional money produced will be directed towards gratifying financiers and broadening the fleet, instead of simply enhancing the balance sheet through increased money reserves or financial obligation decrease. The business’s loan-to-value ratio is an excellent sector-leading 30%. The current choice to raise the payment ratio to 100% highlights its obligation to investors, even more exhibited by the $0.80 dividend stated in Q2. Cumulatively, the dividends stated in 2023 concerned $2.63

In addition to high dividends, Euronav’s low financial obligation has actually enabled them to purchase their fleet. The very first half of 2023 saw the addition of 3 brand-new Huge Unrefined Providers (VLCCs). The business likewise just recently invited a brand-new Suezmax vessel and prepares to incorporate 4 more into its fleet within the next year. While we would choose to see capital be gone back to financiers rather of invested in brand-new vessels at traditionally high appraisals, we do comprehend that the business present and future will be figured out by these vessels.

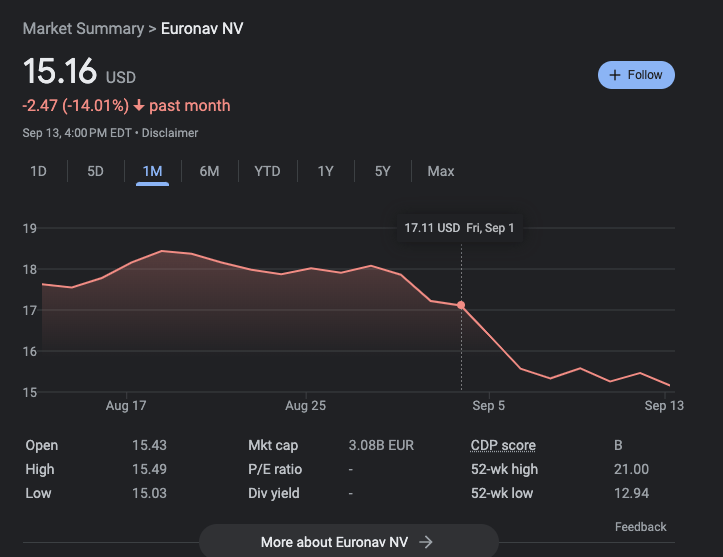

While VLCC rates are staying at their raised levels, the previous 9-10 months have actually seen an increase in oil need, with Euronav benefiting considerably over that timeframe. China led the unrefined develop, however they have actually just recently decreased their big unrefined purchases in addition to this Saudi Arabia has actually continued their voluntary sluggish down. This downturn in unrefined purchases and production has actually straight impacted EURN and over the last couple of weeks shares have actually fallen approximately 15%.

Google Stocks

Speculation around Iran’s possible re-entry into the oil market would be a game-changer for EURN. With Iran’s present production level at 1.5 million barrels each day, this re-entry might open a considerable market sector for Euronav and would balance out the voluntary Saudi Arabian cuts.

The Area Market

Fearnley’s

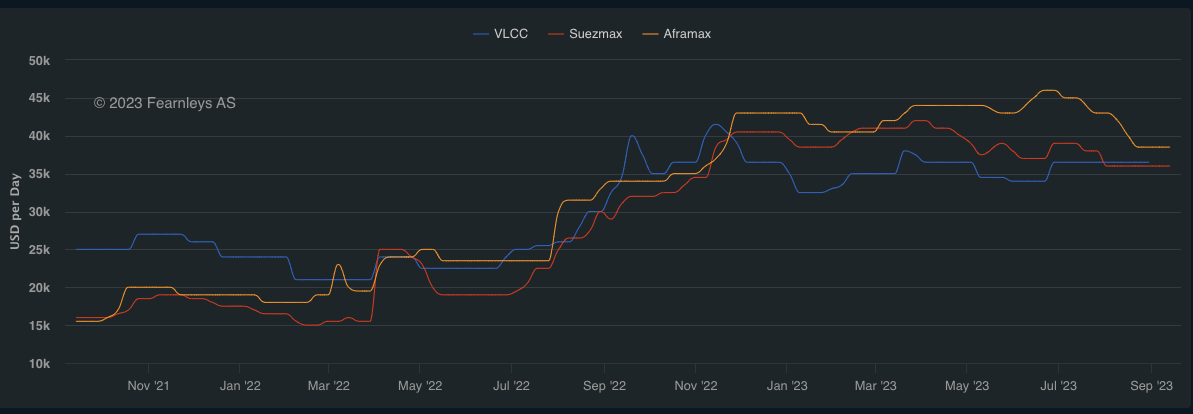

In spite of some current short-term headwinds VLCC rates have actually stayed raised with rates for VLCC’s hovering around $35k each day. It is forecasted that there will be some weakening in Aframax and Suezmax rates relative to VLCCs however that weak point isn’t anticipated for a couple of months. With such a low debt-load EURN’s breakevens on their ships are likewise market leading. EURN has a breakeven on Suezmax’s of $16,000 each day and $19,000 for VLCC’s. Some forward reservations for Q3 for EURN have actually been repaired at $45,000 each day which reveals simply how successful this present rate environment is for EURN.

Appraisal

FactSet & & Stifel

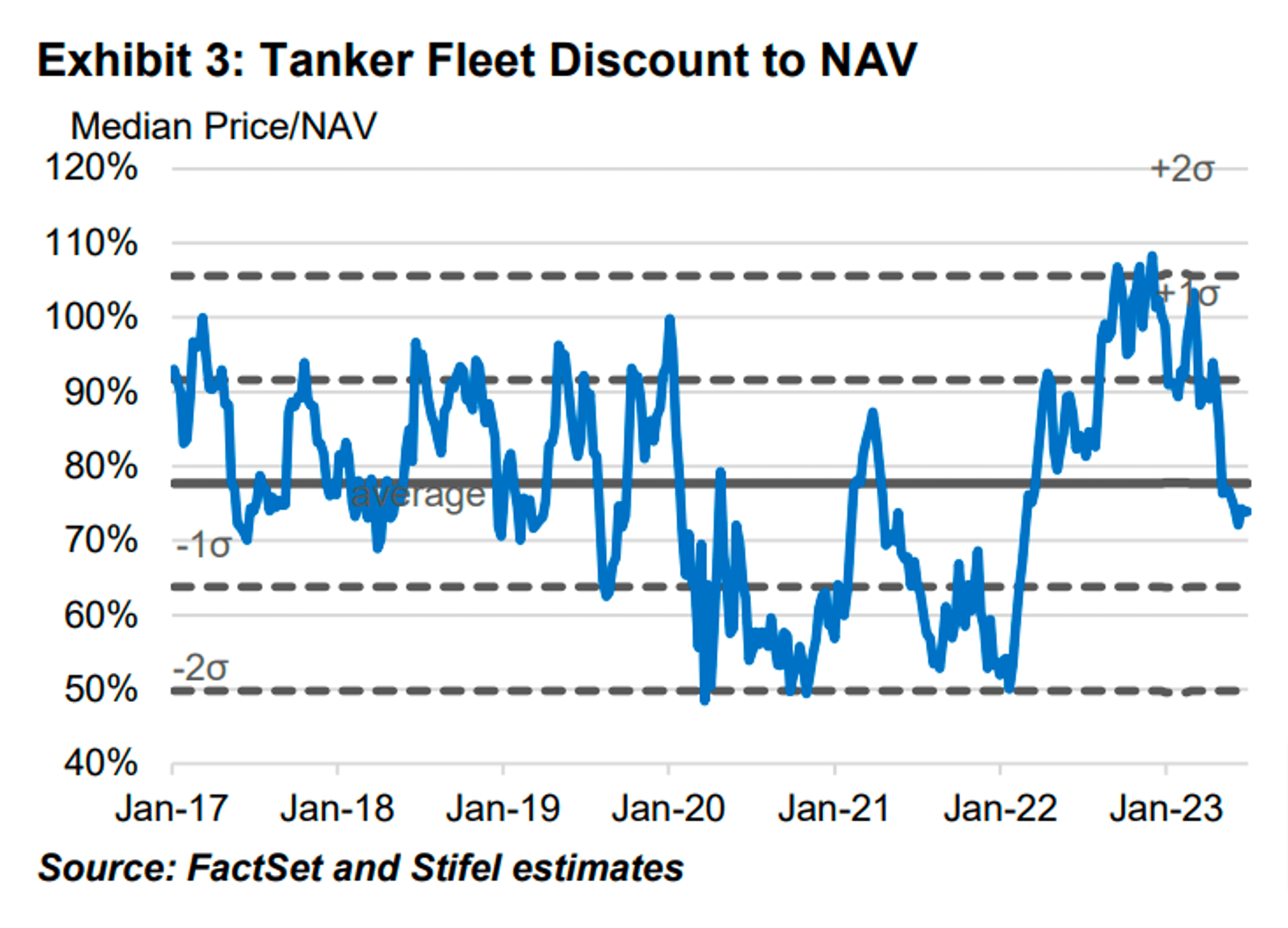

Because 2017, tanker fleets have actually generally traded at a discount rate to NAV with approximately ~ 79%. While success for fleet operations has actually differed extensively over this time so has the assessment of the fleets.

Pareto

Presently, the P/NAV for the majority of the significant names in the area hovers around 0.85 x and EURN sits right around that average with a P/NAV of 0.86 x. This is approximately in line with the historic average of 0.79 x. Our company believe that STNG, GASS, and INSW use much better NAV plays if you think that these names ought to trade near the historic averages.

Conclusion

In our initial remarks, we highlighted possible structural imbalances in the tanker market, which we prepare for will drive charter rates greater throughout 2023 and into 2024. Euronav is poised to take advantage of these raised rates, and, unlike its equivalents, it’s not singularly concentrated on balance sheet improvement. Their contemporary fleet uses a protective guard versus the pushing requirement for brand-new acquisitions– an obstacle facing rivals like Teekay Tankers ( TNK). We are positive that EURN stands apart as a business most likely to regularly funnel its incomes to investors. This conviction is strengthened by the management’s steady commitment to generous payment ratios. While the Oil Tanker and product sectors are not without threats, EURN’s considerable dividends, beneficial area rates and low everyday breakevens use a buffer versus possible declines. Euronav uses appealing dividends and provides a reasonable assessment matched by guaranteeing development potential customers, provided the ideal macroeconomic circumstances. We prepare to have a ‘purchase and hold’ method, as we visualize a favorable environment for tankers continuing for the foreseeable future.