Falcor

It’s been an unstable previous couple of months for the Gold Miners Index ( GDX), however the sharp pullback we have actually seen in some names like Orla Mining ( ORLA), Coeur Mining ( CDE), and AngloGold Ashanti ( AU) ought to not be unexpected, considered that they were priced for near excellence in April/May relative to their peers. Sadly, the pullback in these names has actually added to the underperformance in the GDX with|45% typical decrease for these 3 names, and couple of names have actually had the ability to avert the sector-wide selling pressure, with just a handful of names still sporting favorable year-to-date efficiency.

And while there’s been an absence of general news beyond fundings to assist support the share rates of miners over the previous number of months, the Q3 Incomes Season is simply around the corner with miners set to report their initial Q3 results today. The given name to report its initial Q3 outcomes was Eldorado Gold ( NYSE: EGO), which is tracking at|69% of its yearly assistance and will require a strong Q4 to provide at its assistance mid-point of 495,000 ounces. In this upgrade, we’ll take a look at the most current quarter, the stock’s appraisal, and see whether the stock is using a sufficient margin of security following its|27% correction from its highs.

Eldorado Gold Pour – Business Site

All figures remain in United States Dollars unless otherwise kept in mind.

Q3 Production & & Sales

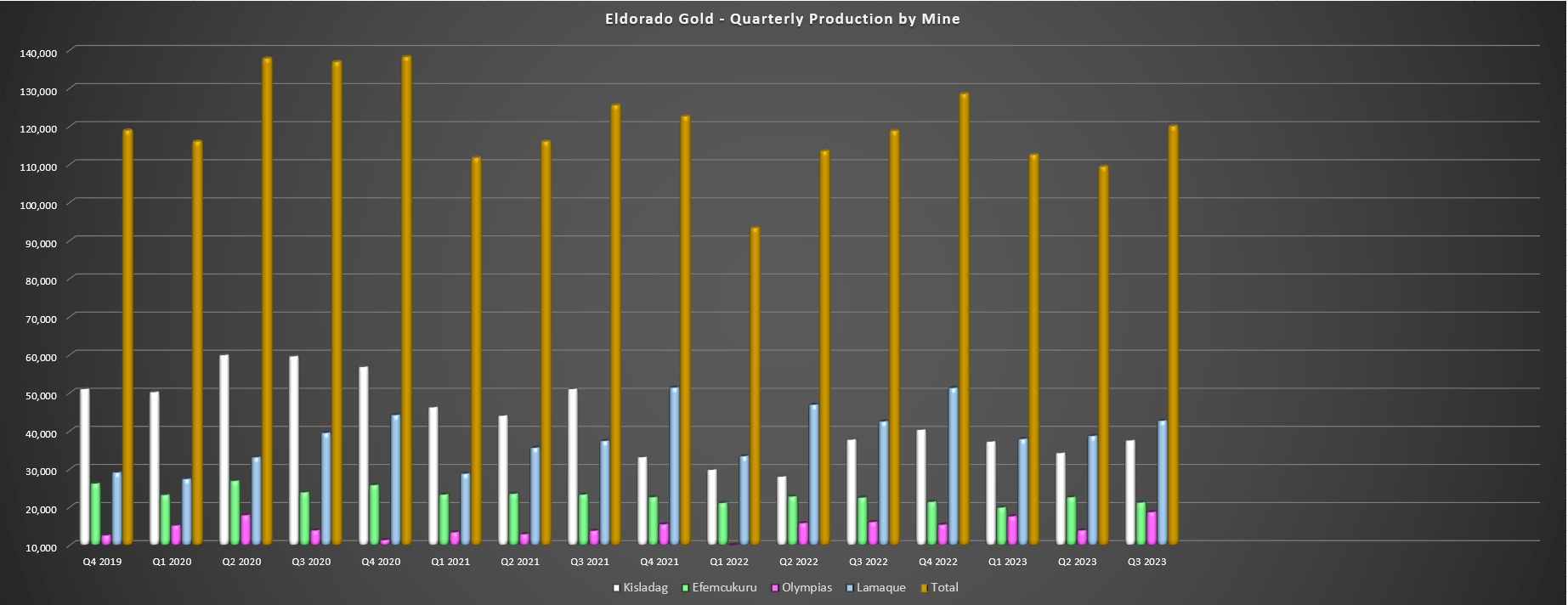

Eldorado Gold launched its Q3 results today, reporting quarterly production of|120,000 ounces of gold, a limited enhancement from the year-ago duration. The 1% boost in production can be credited to greater output from its tiniest polymetallic Olympias Mine in Greece and Lamaque, with production up by|0.5% at Lamaque and|16% at Olympias to|42,700 ounces and|18,700 ounces, respectively. This was partly balanced out by lower production at its flagship Kisladag Mine and its smaller sized Efemcukuru Mine, with production at Kisladag down partially to|37,500 ounces and Efemcukuru’s production down over 5% to|21,200 ounces. The outcome of the softer quarter than I anticipated is that Eldorado Gold is heading into Q4 with simply|341,000 ounces produced, or|69% of its yearly assistance midpoint of 495,000 ounces.

Eldorado Gold – Quarterly Production by Mine – Business Filings, Author’s Chart

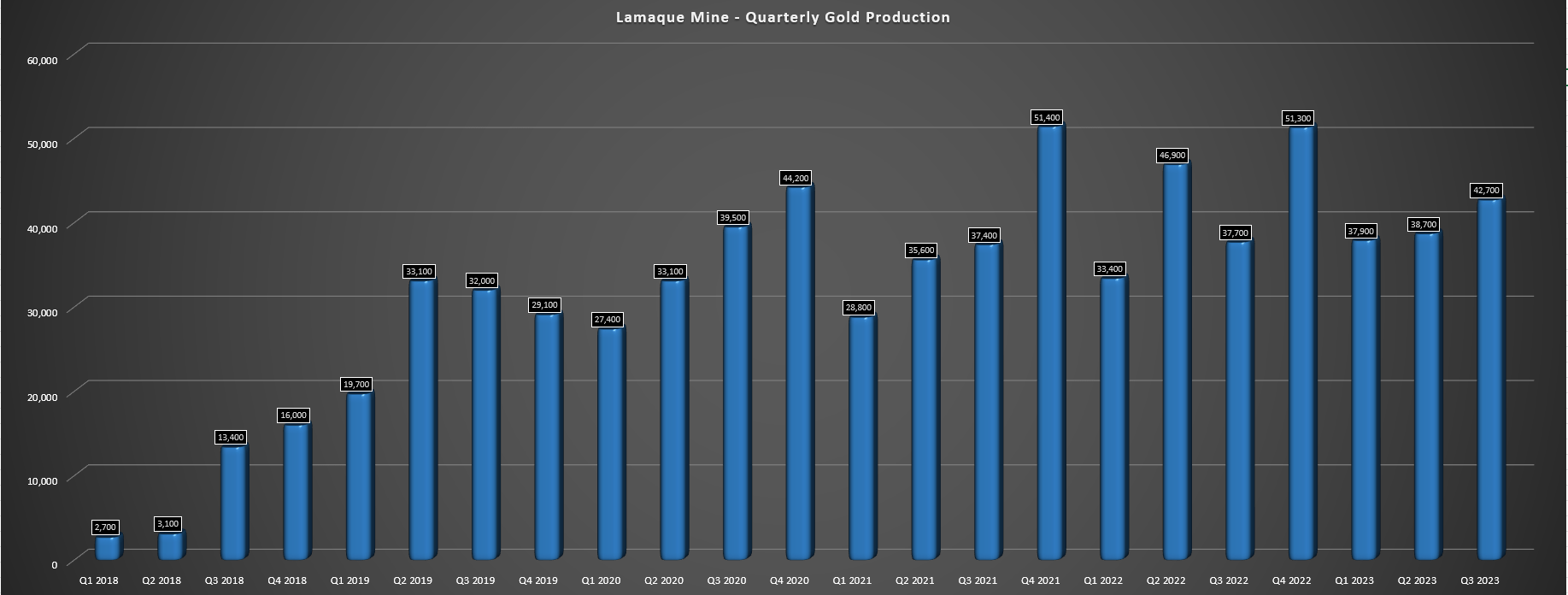

In Eldorado’s defense, it hasn’t been a simple year for the business’s Lamaque Mine in Quebec, with Q2 production impacted by wildfires that caused lower throughput, with the business picking to suspend some shifts to guarantee its employees’ security. While the business still assembled a strong Q2 at the mine in spite of the interruptions, underground advancement is a little behind due to the fact that of the lost shifts last quarter. This has actually left Lamaque sitting at simply|68% of its yearly assistance midpoint (175,000 ounces), and the business will now require a record quarter of|55,700 ounces simply to satisfy its assistance midpoint. And while Q4 will be much more powerful with access to state-of-the-art stopes in the C4 Zone (this zone has a typical reserve grade of|7.2 grams per tonne of gold per 2021 TR), the previous record for Lamaque is|51,400 ounces, recommending the property is most likely to come in simply behind its assistance mid-point even with a strong surface to the year.

Lamaque Mine – Quarterly Production – Business Filings, Author’s Chart

Moving over to Kisladag, it was an acceptable quarter for the Turkish Mine, with production of|37,500 ounces, down somewhat from the|37,700 ounces produced in Q3 2022. This has actually left the mine well behind its assistance too (| 66% of yearly assistance midpoint), however like Lamaque, it must delight in a more powerful Q4 too. And while Q3 was available in somewhat behind my price quotes, Eldorado kept in mind that its heap drum was effectively commissioned and greater tonnes are now being put with the advantage of increased capability from its insect conveyors and radial stacker. Still, even if Kisladag has a beast quarter with 55,000 plus ounces (simply shy of its finest quarter in the previous 3 years in Q4 2020), it will likewise be available in simply shy of its FY2023 assistance midpoint of 165,000 ounces.

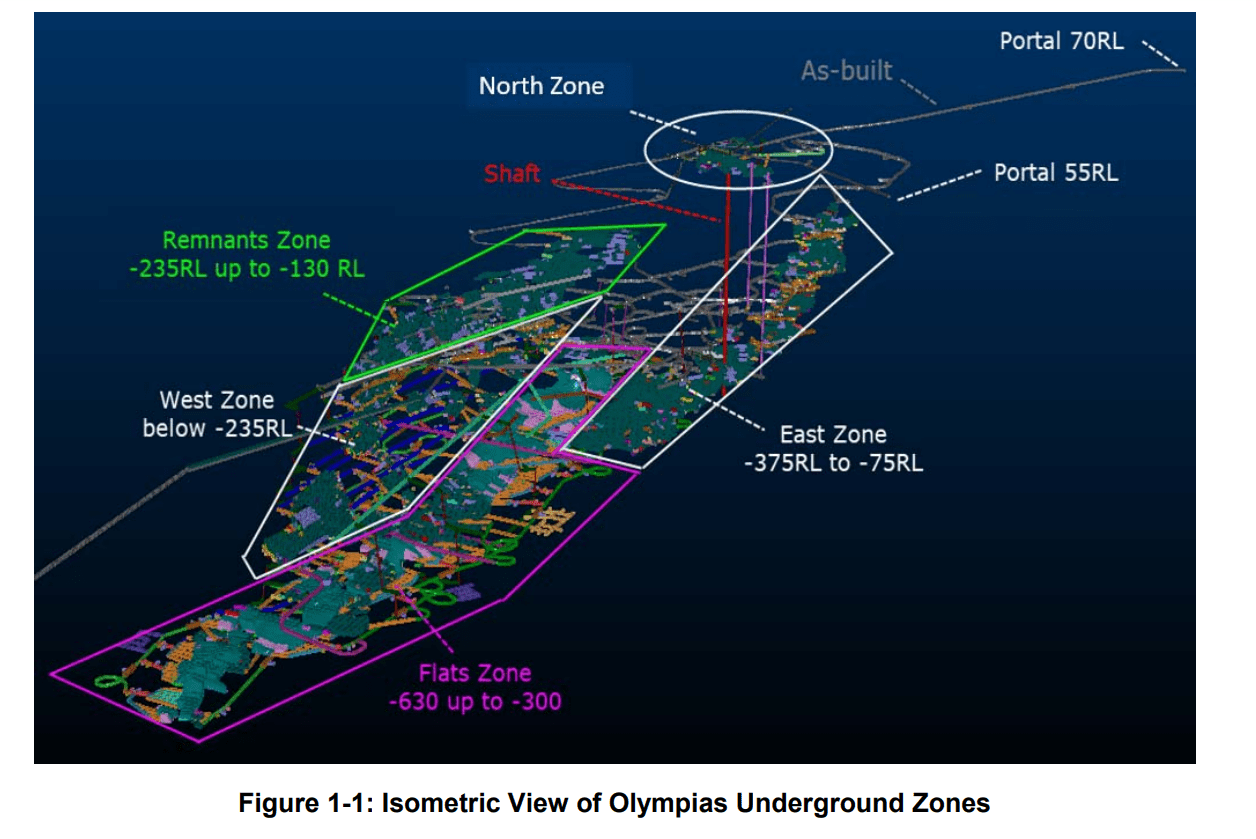

Olympias UG Mine Isometric View – Technical Report

Moving over to the business’s 2 tiniest mines, Efemcukuru is tracking well versus yearly assistance (| 75%), and while Olympias lags its yearly assistance midpoint, we continue to see enhancements at this property which will eventually take production greater over the coming years. Eldorado kept in mind in its ready remarks that the property is now gaining from enhanced ventilation, which will permit increased advancement headings, and permit much better efficiency in lower parts of the mine where higher-grade base metals exist. On the other hand, the business has actually transitioned to bulk emulsion blasting which will equate to enhanced advancement rates. So, while this property has actually been a constant sub 20,000 ounce manufacturer at greater expenses, it’s good to see things advancing well on the ground, with bigger drop in the Flats Zone (lower mine) anticipated to benefit Q4 production.

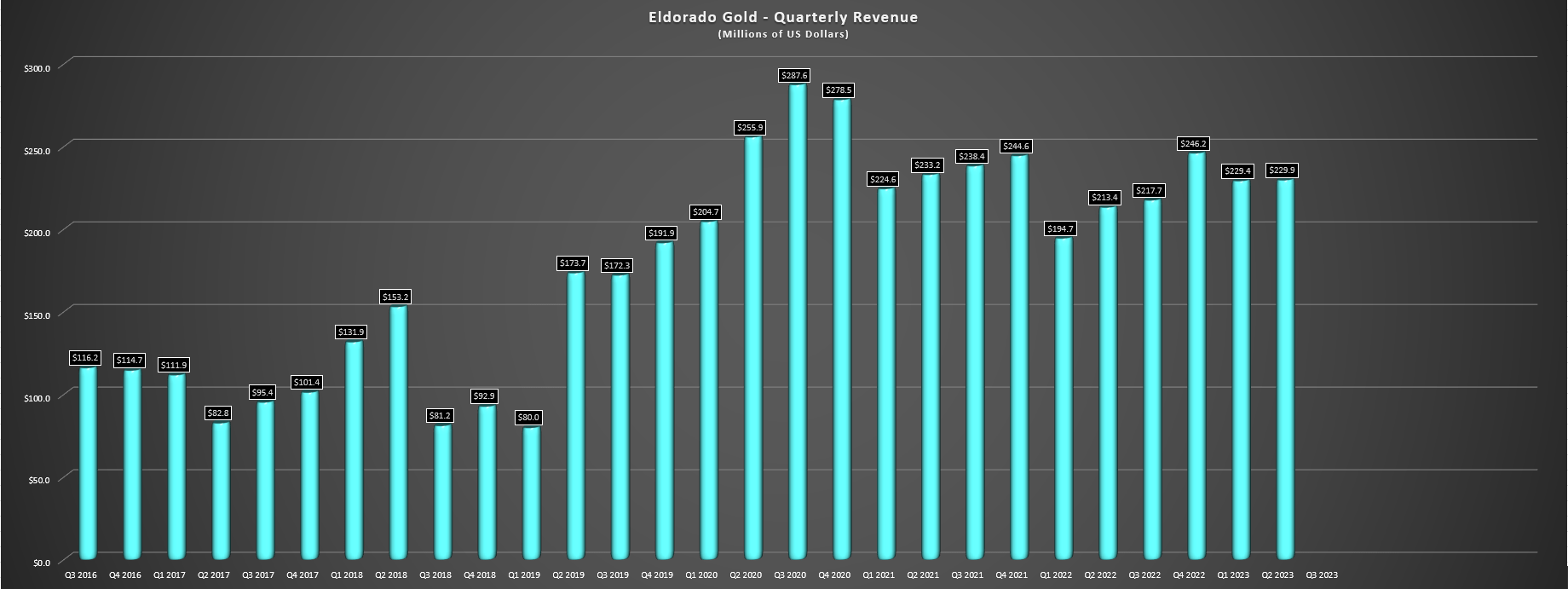

Lastly, from a sales perspective, Eldorado’s gold sales might be available in at comparable levels to in 2015 (| 118,400 ounces), however it will take advantage of simple year-over-year compensations with a typical understood cost of simply $1,688/ oz in Q3 2022. For this reason, Eldorado must see a sharp boost in profits from the $217.7 million reported in the year-ago duration, with profits most likely to increase a minimum of 10%, with real profits depending upon the number of ounces are offered in the duration and its typical understood cost. Sadly, Olympias will not benefit as much as its other gold-only possessions from a sales perspective, with lower zinc rates being a small drag on its outcomes. On a favorable note, however, zinc has actually gone into a brand-new uptrend after a violent bearish market decrease, with base metals tightening for its Q4 results presuming they can keep their current gains, which ought to assist Olympias report lower expenses with the advantage of greater spin-off credits.

Eldorado Gold – Quarterly Income – Business Filings, Author’s Chart

Current Advancements

Moving over to current advancements, Eldorado kept in mind that its Skouries Task stays on budget plan and schedule, with business production at this transformative gold-copper porphyry anticipated by year-end 2025. As it stands, the job is sitting at 33% conclusion, in-depth engineering is at 55% conclusion, and procurement is at 68% conclusion, with the job anticipated to end the year at almost 40% total. For those unknown, this property might be continuing relatively rapidly due to the fact that it was currently partly built prior to building and construction was stopped in 2015 following the approval to finish its building and construction at Skouries being withdrawed previously in the year. For this reason, although building and construction just rebooted just recently, it’s currently over one-third total due to the headstart from the previous building and construction duration and gain from considerable sunk capital.

When it pertains to Skouries, the advantages to Eldorado are huge, assisting to increase its typical weighted mine life, assisting to substantially enhance its margins, and including|140,000 ounces of yearly gold production to press company-wide production towards the 700,000+ ounce mark. Nevertheless, while the business’s liquidity and capital from its 4 operating mines can quickly support financing building and construction of Skouries without the requirement for any additional share dilution, this big job will lead to considerable complimentary money outflows in the near term, and we’re still 2 years far from business production. So, while developing this property is definitely the best relocation as it makes Eldorado’s margins a lot more competitive amongst its peer group, the stock might underperform in a market where little worth is being provided to future development. This isn’t a concern for client financiers, however with energy rates increasing, the gold cost softening, and inflationary pressures staying sticky, we might see approximately $300 million in complimentary money outflows next year if product rates do not enhance.

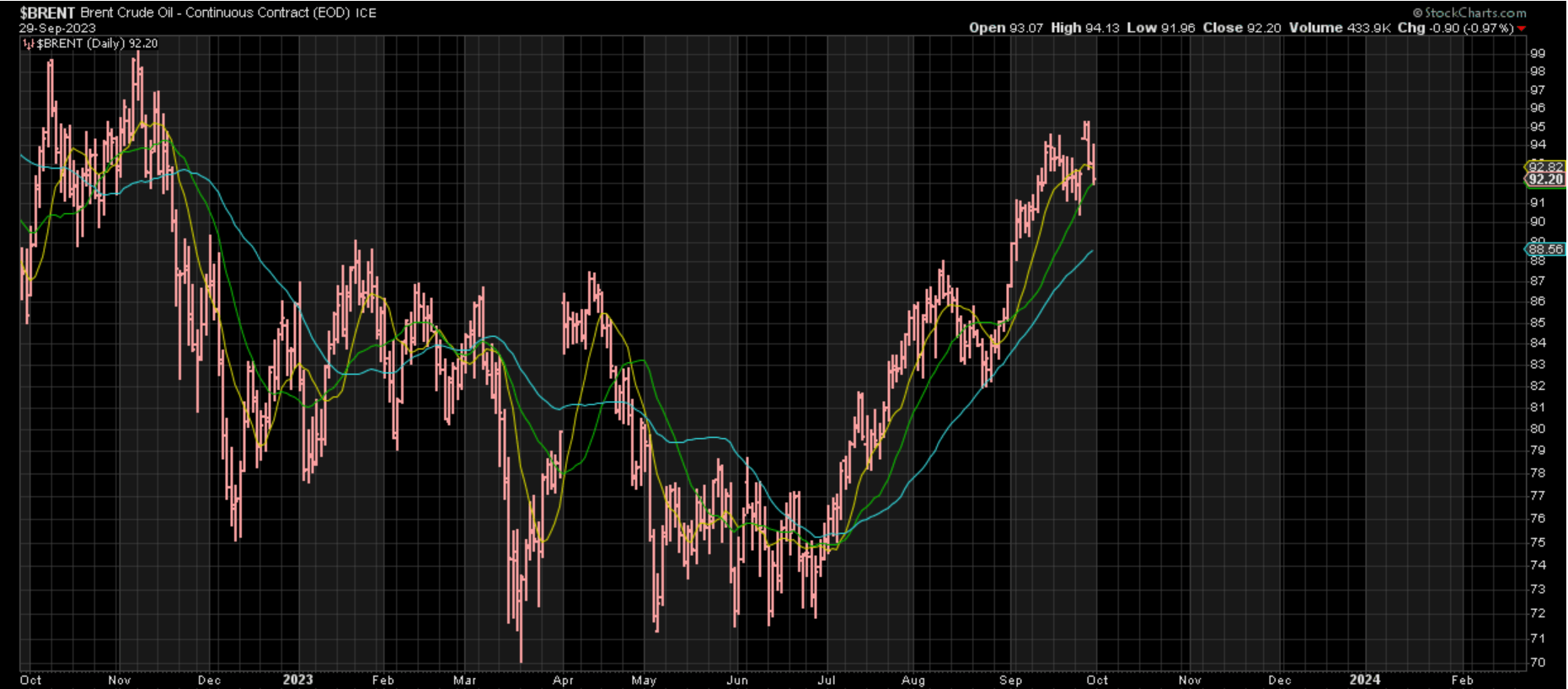

Brent Petroleum Daily Chart – StockCharts.com

On The Other Hand, at its present operations, it appears like it will be tight in concerns to fulfilling all-in sustaining expense assistance, with the greater oil cost set to effect Eldorado’s expenses and sustaining capital currently being rather back-end weighted with|40% of prepared sustaining capital invested in H1. So, with all-in sustaining expenses currently sitting 4% above its assistance mid-point in H1 ($ 1,296/ oz vs. $1,240/ oz), it will be difficult for Eldorado to provide at or listed below its assistance mid-point. Certainly, this is not a huge offer when it pertains to the larger image with a property with sub $100/oz AISC set to delight in a complete year of production in 2026. Still, short-term, Eldorado might see more margin pressure like its peers with weaker gold rates, an increasing oil cost, and numerous business reporting sticky inflationary pressures. Let’s have a look at the stock’s appraisal listed below.

Evaluation

Based Upon|208 million totally watered down shares and a share cost of US$ 8.90, Eldorado trades at a market cap of|$1.85 billion and a business worth of|$1.95 billion. This leaves Eldorado Gold as one of the most affordable capitalization names amongst its 500,000 ounce manufacturer peers, and among the steeper discount rates amongst business that have the prospective to grow production to 700,000+ ounces within 4 years. That stated, the business is not producing complimentary capital presently in an environment where the marketplace is providing little worth to future development and rather concentrating on present capital for evaluations. So, while Eldorado Gold might have a brilliant future and the prospective to produce $320+ million in yearly complimentary capital in 2026, financiers can anticipate a totally free money outflow of $300+ million next year if gold rates do not rebound, offered the considerable development capital for Skouries set to be invested in between now and year-end 2025.

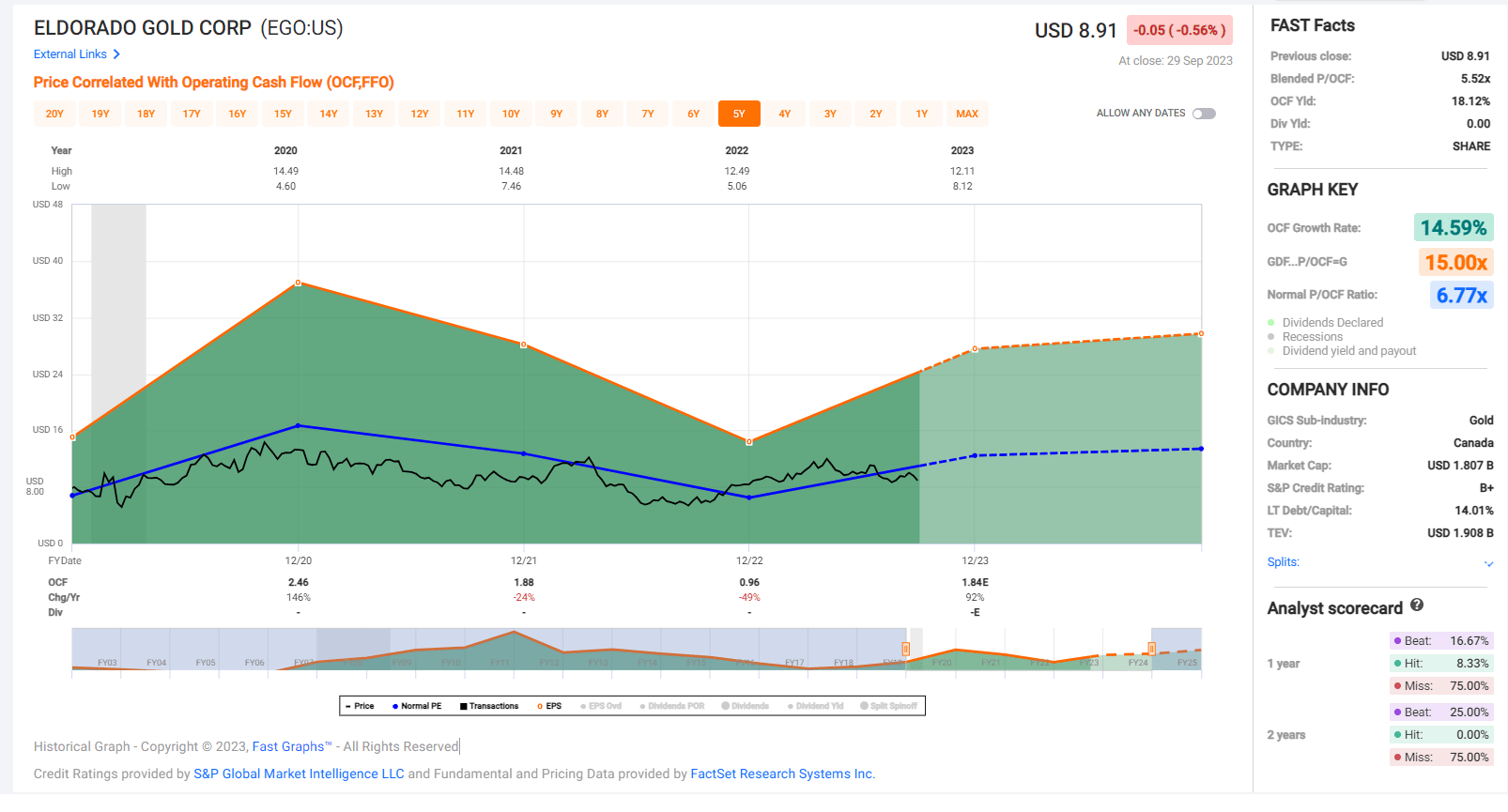

EGO – Historic Capital Numerous – FASTGraphs.com

Taking A Look At the above chart, we can see that Eldorado has actually traditionally traded at|6.8 x capital, and traded at|6.6 x FY2023 capital per share price quotes in Might, for this reason why I noted this was not the time to be chasing after the stock above US$ 12.00. Ever since, EGO has actually underperformed its peer group with a 26% drawdown (24% drawdown in the GDX). When it comes to the stock’s reasonable worth, I believe a more conservative several for EGO is 6.5 x capital offered the several compression we have actually seen sector-wide, with some senior manufacturers trading listed below 6.0 x FY2024 capital per share price quotes, not to mention mid-tiers like Eldorado. If we use this more conservative multiple to FY2024 capital per share price quotes of $2.05, Eldorado’s reasonable worth is available in at US$ 13.30, indicating a 48% upside from present levels.

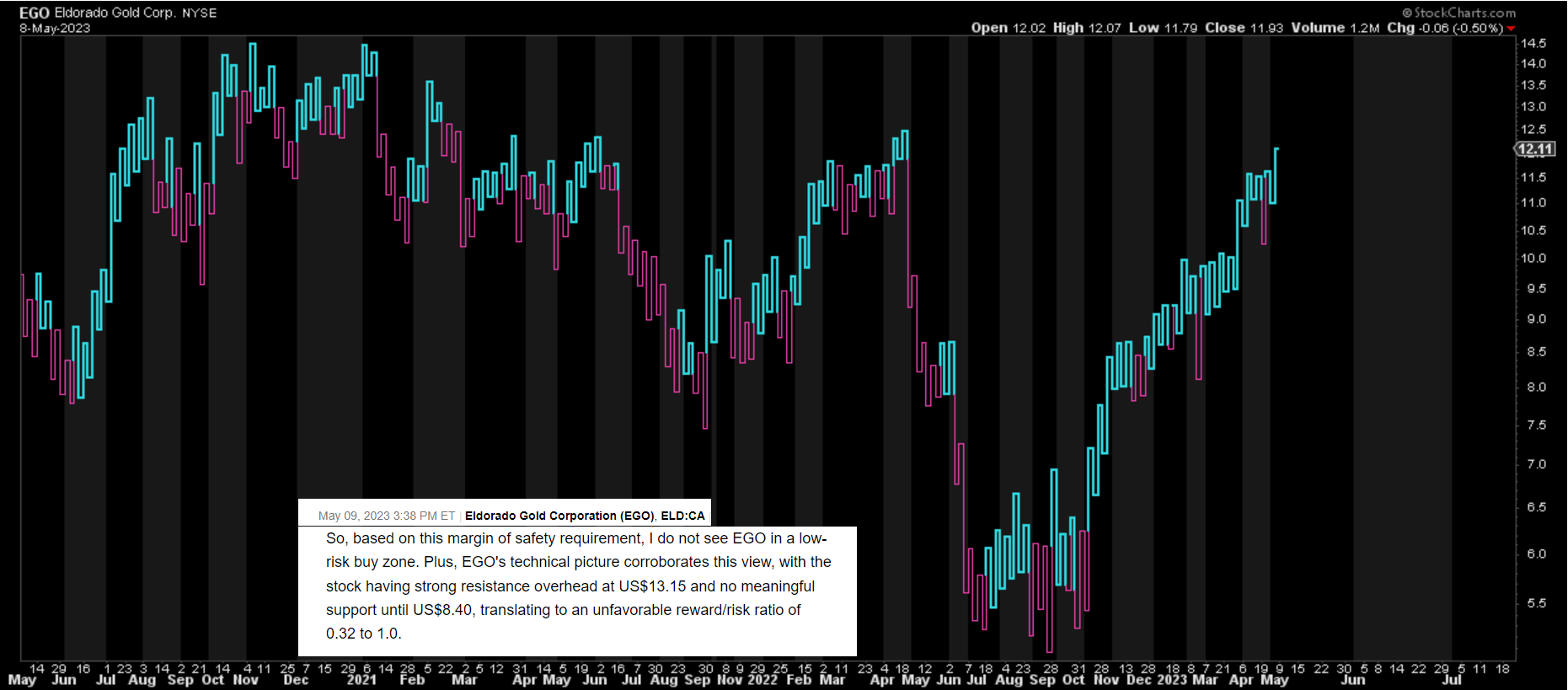

EGO Daily Chart & & Might Update – Looking For Alpha Premium, StockCharts.com

Although this is a good benefit case for an 18-month cost target and Eldorado is trading at simply|4.9 x P/CF on this year’s price quotes, I am searching for a minimum 40% discount rate to guarantee a margin of security. If we use this discount rate, Eldorado’s perfect buy zone is available in at US$ 8.00 or lower, recommending that although the stock might be down dramatically from its highs, it still hasn’t entered what I would think about being a low-risk buy zone. Although the business’s future is brilliant, financiers will need to wait a minimum of 2 years at present gold rates to see an inflection point in complimentary capital. So, while EGO would remain in a low-risk buy zone currently if not for its current funding that led to share dilution, I do not see enough of a margin of security right now with it trading at|6x FY2026 complimentary capital approximates vs. names like B2Gold ( BTG) at hardly 5x FY2025 complimentary capital approximates with a bigger production profile and|5.6% dividend yield that pays financiers to wait.

Summary

Eldorado Gold has actually drawn back dramatically from its highs and has actually exceeded its peer group year-to-date, taking pleasure in a 6% year-to-date return vs. the GDX’s unfavorable return for the 3rd successive year if its current efficiency continues. This outperformance can be credited to the change that Skouries will supply to its portfolio, which this job was green-lighted for the resumption of building and construction previously this year, with its very first gold put anticipated in 2025. That stated, while this property will be a totally free capital device, we will see considerable complimentary money outflows in the interim, considered that this is an enormous job, and while on budget plan, there is threat to capex misses out on for significant development jobs (like we saw from the Super Pit Growth and Hemi just recently in Australia) with inflation staying stickier than anticipated. So, while EGO is definitely a name worth owning offered its mix of growing production at enhancing margins, I continue to see more appealing bets somewhere else from a relative worth perspective.