sankai

Composed by Nick Ackerman.

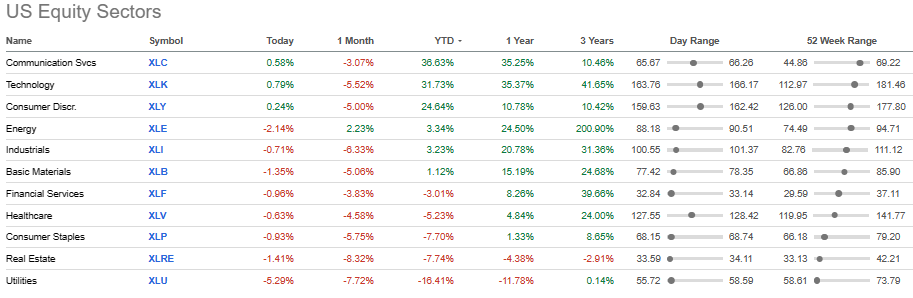

Realty financial investment trusts (” REITs”) have actually been getting struck hard by greater yields as the Fed increase rates of interest. In addition, energy business are being struck by the exact same thing. In truth, energies are the worst-performing sector on a YTD basis by a large margin. Other protective sectors, such as customer staples and health care, likewise aren’t looking too healthy this year, either.

Softer assistance from NextEra Energy ( NEE) has actually sent out the sector spiraling lower, which, in mix with seeing the safe rates increasing, is driving the sector considerably lower more just recently.

U.S. Equity Sector Efficiency ( Looking For Alpha)

Besides safe Treasury yields ending up being more appealing options to riskier equity properties, REITs and energies are likewise organization operations that normally count on financial obligation. A primary type of development for REITs is through funding brand-new jobs or acquisitions to grow their profits. Energies deal with heavy CAPEX requirements as facilities takes a remarkable quantity of products and labor to construct and keep trusted services to clients.

Lower rates of interest might definitely be a tailwind, however it likewise depends upon the situation of why the Fed would need to cut rates of interest. On the other hand, even if rates remain where they are and one thinks that we are near peak rates of interest from the Fed, we might prepare for some stabilization in these sectors too. So, I do not think that we always require to await the next one or perhaps 2 walkings from the Fed to attempt to eject the outright bottom. Investing is a long-lasting video game over several years, not normally attempting to time the marketplace from month to month.

All this being stated, there are a lot of names for dividend financiers taking a look at appealing yields and desiring some dividend development in the future for long-lasting financiers. 2 names that look intriguing and, I think, should have some financier attention are the NNN REIT ( NNN) and WEC Energy Group ( WEC).

NNN REIT

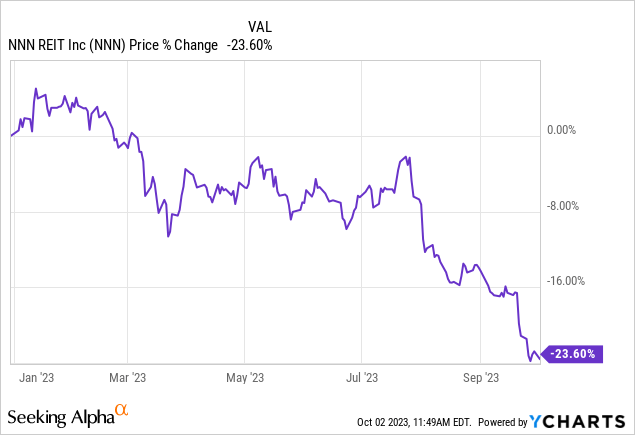

NNN REIT was previously Nationwide Retail Residences, however they altered their name previously this year. Sadly, the name modification did extremely little to decrease the share rate reduction that the REIT has actually been experiencing. Shares are now off almost 24% on a YTD basis.

NNN holds a basket of single-tenant net lease retail residential or commercial properties with a high tenancy level of 99.4% since their most current upgrade This is throughout 3479 residential or commercial properties in 49 various states. For more diversity steps, the REIT notes over 385 various nationwide and local retail occupants, so they are exposed to a different basket of retail occupants. Nevertheless, it deserves keeping in mind that the leading 25 represent approximately 55% of their leas.

They definitely aren’t any complete strangers to various financial conditions as they boast a 39-year performance history, with 34 of those years seeing successive dividend boosts. In addition, they kept in mind that a 20-year low tenancy rate just ever touched 96.4%. This is appealing, thinking about that many financial experts are anticipating some sort of economic downturn as we head into 2024 and even in the tail end of 2023.

Hence, an economic downturn, among the reasons we would prepare for possibly lower rates of interest from the Fed in the next number of years, is to assist relieve pressure from REITs and energies.

Naturally, the counter-argument to that is the harder operating environment might then end up being the brand-new headwind. So, seeing information that recommends a strong performance history in even black swan occasions is rather soothing. It’s difficult to anticipate, however it basically depends upon the depths of the economic downturn when one takes place and just how much damage might be done. A shallow or moderate economic downturn might see restricted pressure on the kinds of occupants that NNN rents to, however a much deeper and extended economic downturn would definitely injure.

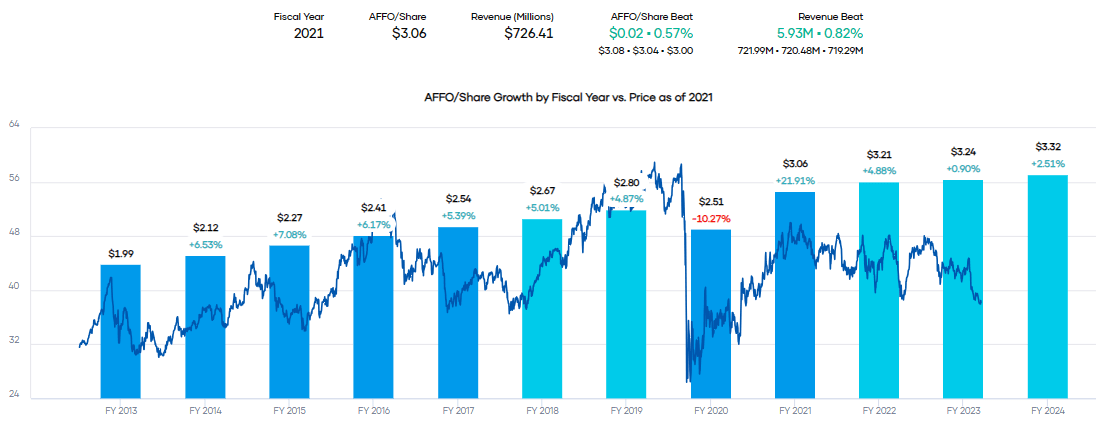

In regards to development moving forward, NNN is anticipated to produce some favorable AFFO development in the coming years. It definitely isn’t the most interesting name, however that might be thought about among its specific beauties. The business has actually frequently had the ability to beat profits over the last a number of years too, with 9 of the last 10 FFO quarterly numbers going beyond those of experts. Last quarter was the sole critic from that pattern as it just satisfied expectations.

NNN Revenues Past and Future Quotes ( Portfolio Insights)

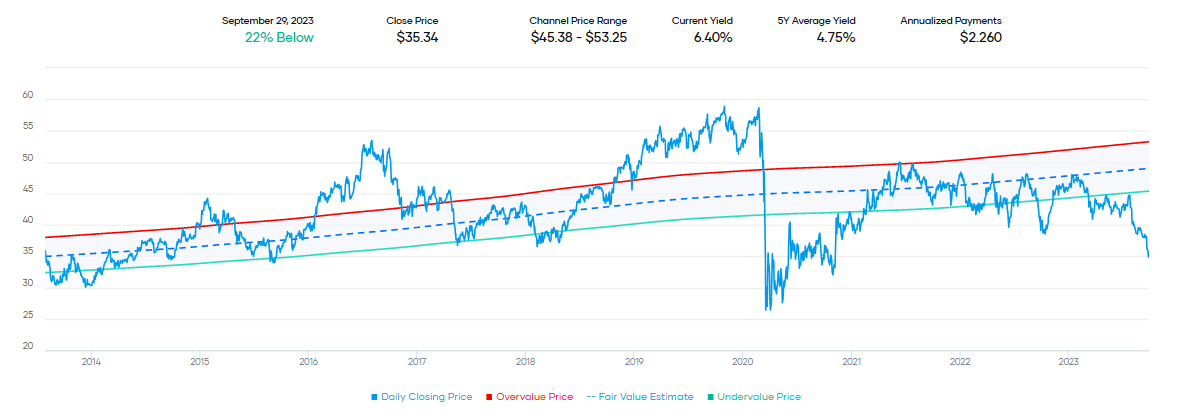

Offered the more dull however constant nature of NNN’s profits, one may prepare for a greater yield being suitable. For the many part, that is basically what has actually taken place over the life of this REIT. Nevertheless, with this sharp sell-off, the yield is now pressing closer to 6.5%, well above its historic average. A few of this is mainly should have as the safe rate has actually likewise ticked up, naturally. Still, this is where the longer-term chance might originate from in being rewarded in the future with development and if/when yields decrease.

NNN Fair Worth Dividend Variety ( Portfolio Insight)

This dividend has actually corresponded in regards to seeing successive development, as we kept in mind above, boasting 34 years of successive boosts. Based upon the profits price quotes for next year and the just recently revealed dividend boost, the forward AFFO payment ratio is relaxing 70%. That leaves a lot of space for more boosts in the future and some cushion if profits take a struck throughout the next economic downturn.

NNN Dividend History ( Looking For Alpha)

WEC Energy Group

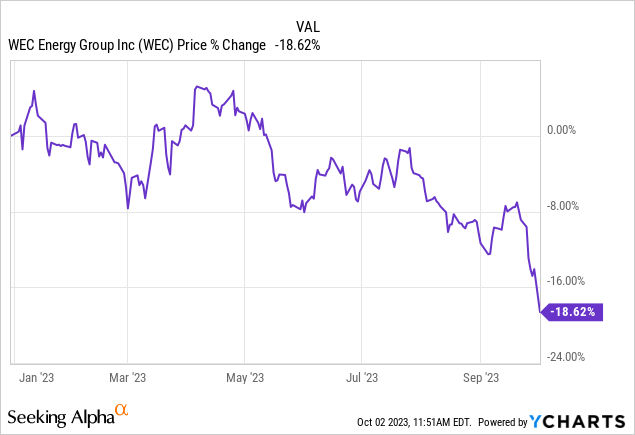

Another name that has actually been struck harder just recently is WEC Energy Group. Shares are off just around 18.5% this year. The majority of this being available in the last couple of days given that NEE revealed a soft outlook with its yield cutting circulation development expectations in half. Sadly for me, I had actually offered $75 rectifies prior to this most current plunge. The likelihood of task was 2% prior to NEE’s statement.

There is not a surprise here as the style of covering NNN and WEC is because of being rate-sensitive. The statement from NEE was more of an admission that greater rates are going to be affecting their outlook more considerably than they most likely wished to confess. After seeing safe yields breach brand-new levels above last October 2022, it makes good sense to see renewed pressure in this area – and we even saw it more broadly throughout the equity market too.

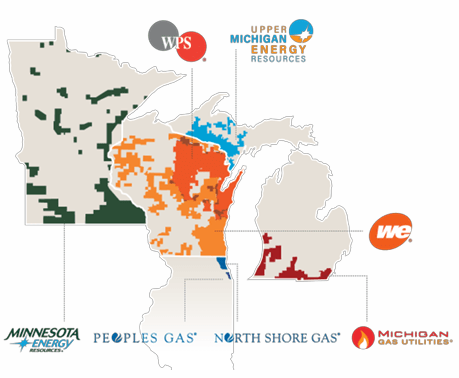

Even after some healing from the lows, the shares are still beautifully priced for a long-lasting earnings financier trying to find a strong energy play. WEC Energy runs a number of energy business under its organizing umbrella, serving 4.6 million retail clients with operations throughout Minnesota, Michigan, Wisconsin and Illinois.

WEC Energy Group Operations ( WEC Energy Group)

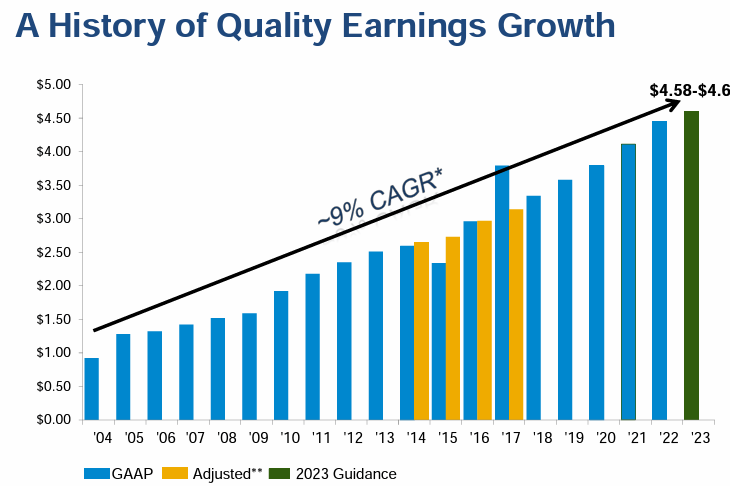

This business has actually had the ability to provide strong profits development for investors returning to 2004. Even through the worldwide monetary crisis, profits kept ticking greater.

WEC Revenues Development History ( WEC Energy Group)

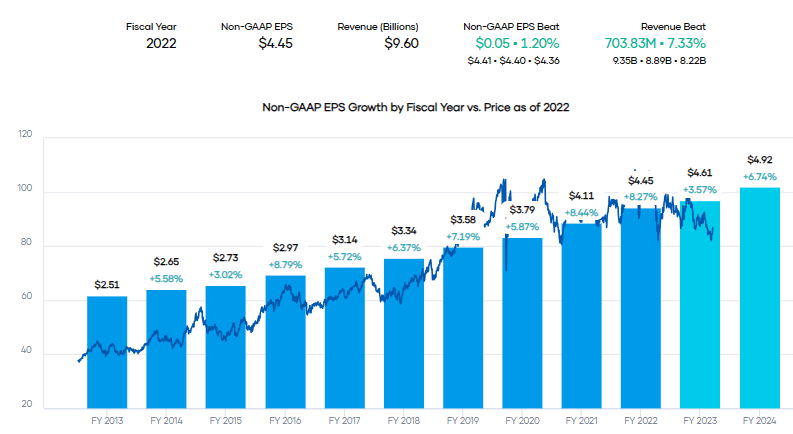

Besides the business’s projection for profits development heading through 2023, this is supported by experts too. The assistance provided by the business is likewise something that must be weighed, considered that they have actually now surpassed their assistance for each year for 19 years now.

Experts think that the business will continue to provide around 4-7% non-GAAP EPS development in the next 2 years.

WEC Revenues History and Projection ( Portfolio Insight)

Surprisingly, this is below simply the more just recently declared assistance from the business of 6.5 to 7% development they are preparing for. Considered that vibrant, they truly are established to surpass expert expectations. That’s another function of WEC that isn’t anything brand-new as they have actually provided for 16 out of the last 16 quarters beat experts’ expectations.

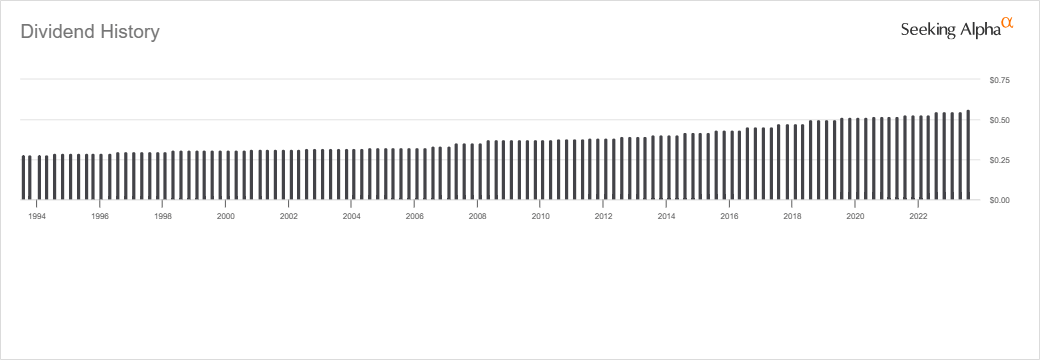

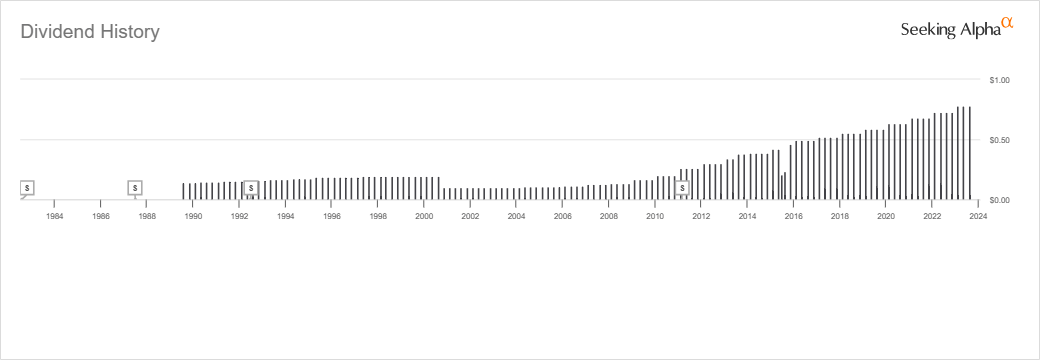

This business provides constant and dull development. That development has actually likewise equated into a progressively growing dividend to investors who can be client over the long term. They have actually raised their dividend for 20 successive years, and they prepare for the development to continue to remain in line with their profits development.

WEC Dividend History ( Looking For Alpha)

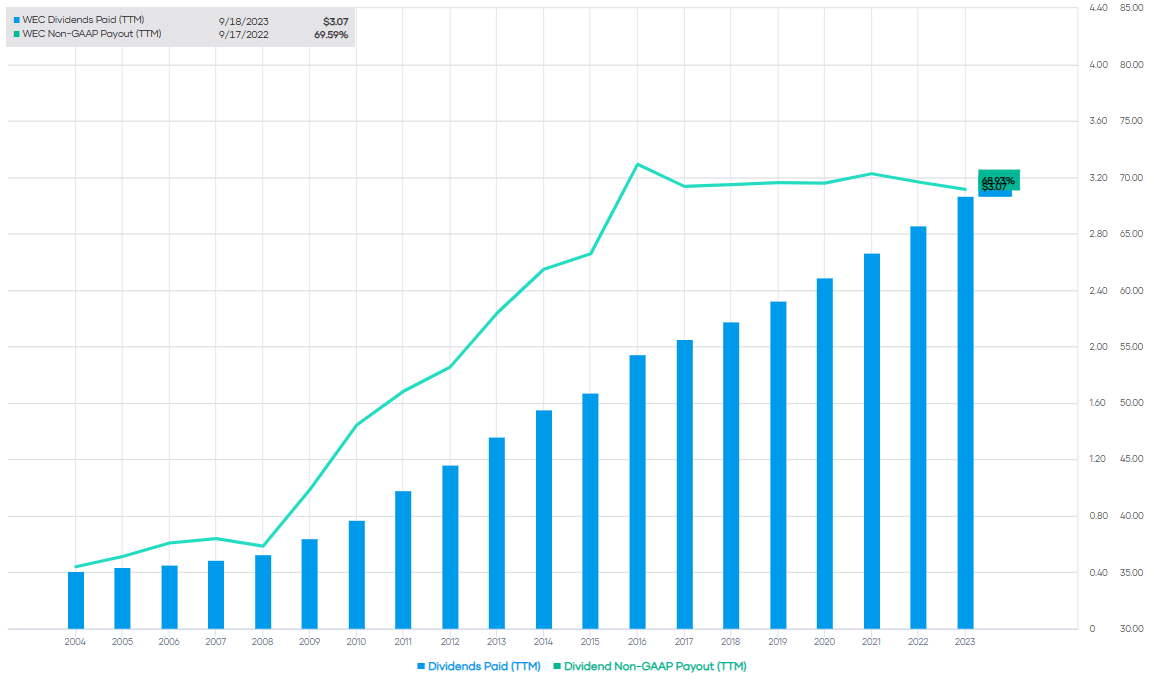

Based upon the forward profits price quotes, we are taking a look at a payment ratio of 67.7%. This payment ratio has actually been relatively constant given that returning to around 2015. Energies and REITs normally pay a relatively considerable quantity of their profits to financiers, so this is another case of a healthy payment level with some cushion for a prospective downturn.

WEC Dividend Payment Ratio ( Portfolio Insight)

Naturally, if there is a prospective downturn, energies can frequently be the supreme defensive play, which might be a tailwind for WEC. Their profits are frequently not strike materially in a downturn as customers still take in electrical power.

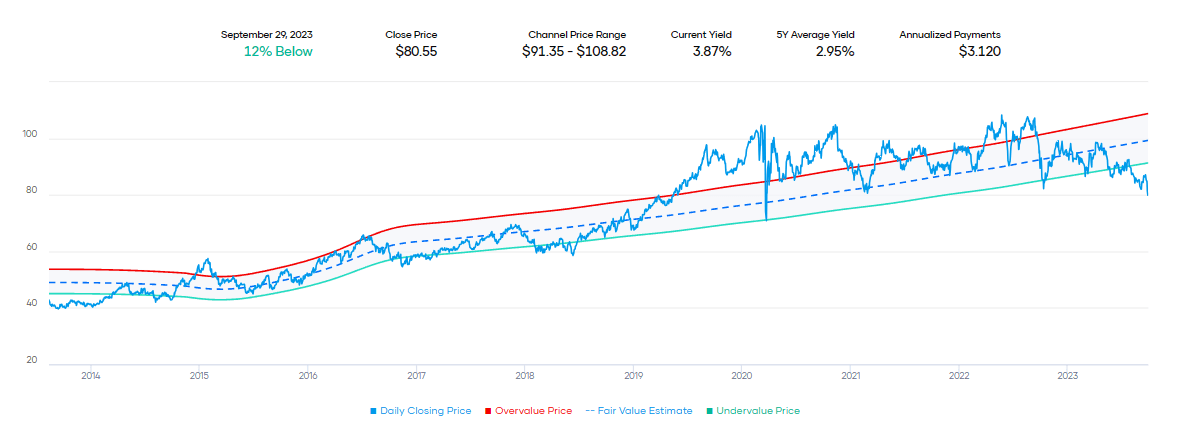

The yield may not be the greatest for this constant energy name, however it still represents an appealing entry for a financier from a historic reasonable worth yield variety. Since composing, shares are down another ~ 5% today.

WEC Fair Worth Dividend Variety ( Portfolio Insight)

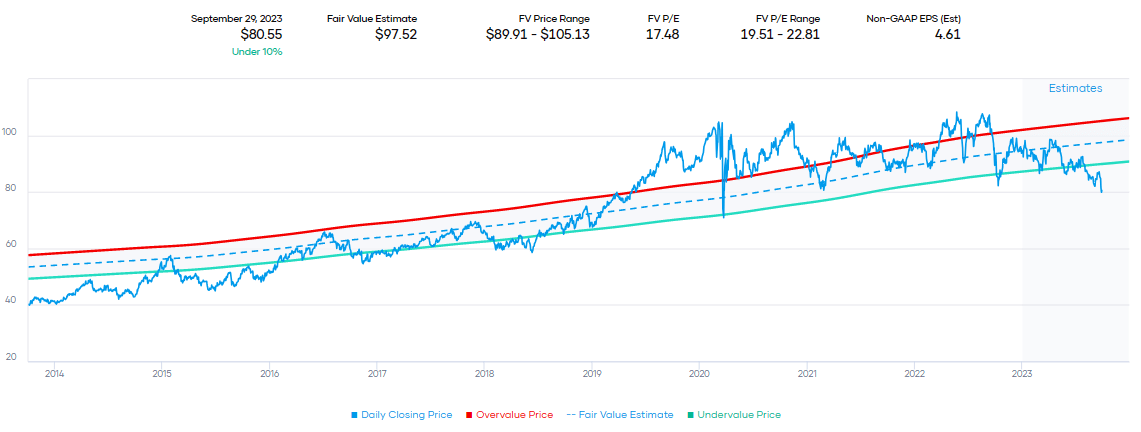

Furthermore, if we take a look at the historic reasonable worth P/E variety, shares are likewise looking rather appealing.

WEC Fair Worth Variety ( Portfolio Insight)

Once again, comparable to what was pointed out with NNN. The safe rate is certainly greater now, which is among the primary pressures that put WEC shares where they are today. Nevertheless, this might still be a great long-lasting bet and even a short-term bet to get more protective if one thinks that the economy will begin to decrease from here.