{“page”:0,” year”:2023,” monthnum”:10,” day”:4,” name”:” active-success-still-elusive”,” mistake”:””,” m”:””,” p”:0,” post_parent”:””,” subpost”:””,” subpost_id”:””,” accessory”:””,” attachment_id”:0,” pagename”:””,” page_id”:0,” 2nd”:””,” minute”:””,” hour”:””,” w”:0,” category_name”:””,” tag”:””,” feline”:””,” tag_id”:””,” author”:””,” author_name”:””,” feed”:””,” tb”:””,” paged”:0,” meta_key”:””,” meta_value”:””,” sneak peek”:””,” s”:””,” sentence”:””,” title”:””,” fields”:””,” menu_order”:””,” embed”:””,” classification __ in”: [],” classification __ not_in”: [],” classification __ and”: [],” post __ in”: [],” post __ not_in”: [],” post_name __ in”: [],” tag __ in”: [],” tag __ not_in”: [],” tag __ and”: [],” tag_slug __ in”: [],” tag_slug __ and”: [],” post_parent __ in”: [],” post_parent __ not_in”: [],” author __ in”: [],” author __ not_in”: [],” search_columns”: [],” ignore_sticky_posts”: incorrect,” suppress_filters”: incorrect,” cache_results”: real,” update_post_term_cache”: real,” update_menu_item_cache”: incorrect,” lazy_load_term_meta”: real,” update_post_meta_cache”: real,” post_type”:””,” posts_per_page”:” 5″,” nopaging”: incorrect,” comments_per_page”:” 50″,” no_found_rows”: incorrect,” order”:” DESC”}

[{“display”:”Craig Lazzara”,”title”:”Managing Director, Index Investment Strategy”,”image”:”/wp-content/authors/craig_lazzara-353.jpg”,”url”:”https://www.indexologyblog.com/author/craig_lazzara/”},{“display”:”Tim Edwards”,”title”:”Managing Director, Index Investment Strategy”,”image”:”/wp-content/authors/timothy_edwards-368.jpg”,”url”:”https://www.indexologyblog.com/author/timothy_edwards/”},{“display”:”Hamish Preston”,”title”:”Head of U.S. Equities”,”image”:”/wp-content/authors/hamish_preston-512.jpg”,”url”:”https://www.indexologyblog.com/author/hamish_preston/”},{“display”:”Anu Ganti”,”title”:”Senior Director, Index Investment Strategy”,”image”:”/wp-content/authors/anu_ganti-505.jpg”,”url”:”https://www.indexologyblog.com/author/anu_ganti/”},{“display”:”Fiona Boal”,”title”:”Managing Director, Global Head of Equities”,”image”:”/wp-content/authors/fiona_boal-317.jpg”,”url”:”https://www.indexologyblog.com/author/fiona_boal/”},{“display”:”Jim Wiederhold”,”title”:”Director, Commodities and Real Assets”,”image”:”/wp-content/authors/jim.wiederhold-515.jpg”,”url”:”https://www.indexologyblog.com/author/jim-wiederhold/”},{“display”:”Phillip Brzenk”,”title”:”Managing Director, Global Head of Multi-Asset Indices”,”image”:”/wp-content/authors/phillip_brzenk-325.jpg”,”url”:”https://www.indexologyblog.com/author/phillip_brzenk/”},{“display”:”Howard Silverblatt”,”title”:”Senior Index Analyst, Product Management”,”image”:”/wp-content/authors/howard_silverblatt-197.jpg”,”url”:”https://www.indexologyblog.com/author/howard_silverblatt/”},{“display”:”John Welling”,”title”:”Director, Global Equity Indices”,”image”:”/wp-content/authors/john_welling-246.jpg”,”url”:”https://www.indexologyblog.com/author/john_welling/”},{“display”:”Michael Orzano”,”title”:”Senior Director, Global Equity Indices”,”image”:”/wp-content/authors/Mike.Orzano-231.jpg”,”url”:”https://www.indexologyblog.com/author/mike-orzano/”},{“display”:”Wenli Bill Hao”,”title”:”Senior Lead, Factors and Dividends Indices, Product Management and Development”,”image”:”/wp-content/authors/bill_hao-351.jpg”,”url”:”https://www.indexologyblog.com/author/bill_hao/”},{“display”:”Maria Sanchez”,”title”:”Director, Sustainability Index Product Management, U.S. Equity Indices”,”image”:”/wp-content/authors/maria_sanchez-527.jpg”,”url”:”https://www.indexologyblog.com/author/maria_sanchez/”},{“display”:”Shaun Wurzbach”,”title”:”Managing Director, Head of Commercial Group (North America)”,”image”:”/wp-content/authors/shaun_wurzbach-200.jpg”,”url”:”https://www.indexologyblog.com/author/shaun_wurzbach/”},{“display”:”Silvia Kitchener”,”title”:”Director, Global Equity Indices, Latin America”,”image”:”/wp-content/authors/silvia_kitchener-522.jpg”,”url”:”https://www.indexologyblog.com/author/silvia_kitchener/”},{“display”:”Akash Jain”,”title”:”Director, Global Research & Design”,”image”:”/wp-content/authors/akash_jain-348.jpg”,”url”:”https://www.indexologyblog.com/author/akash_jain/”},{“display”:”Ved Malla”,”title”:”Associate Director, Client Coverage”,”image”:”/wp-content/authors/ved_malla-347.jpg”,”url”:”https://www.indexologyblog.com/author/ved_malla/”},{“display”:”Rupert Watts”,”title”:”Head of Factors and Dividends”,”image”:”/wp-content/authors/rupert_watts-366.jpg”,”url”:”https://www.indexologyblog.com/author/rupert_watts/”},{“display”:”Jason Giordano”,”title”:”Director, Fixed Income, Product Management”,”image”:”/wp-content/authors/jason_giordano-378.jpg”,”url”:”https://www.indexologyblog.com/author/jason_giordano/”},{“display”:”Sherifa Issifu”,”title”:”Senior Analyst, U.S. Equity Indices”,”image”:”/wp-content/authors/sherifa_issifu-518.jpg”,”url”:”https://www.indexologyblog.com/author/sherifa_issifu/”},{“display”:”Qing Li”,”title”:”Director, Global Research & Design”,”image”:”/wp-content/authors/qing_li-190.jpg”,”url”:”https://www.indexologyblog.com/author/qing_li/”},{“display”:”Brian Luke”,”title”:”Senior Director, Head of Commodities and Real Assets”,”image”:”/wp-content/authors/brian.luke-509.jpg”,”url”:”https://www.indexologyblog.com/author/brian-luke/”},{“display”:”Glenn Doody”,”title”:”Vice President, Product Management, Technology Innovation and Specialty Products”,”image”:”/wp-content/authors/glenn_doody-517.jpg”,”url”:”https://www.indexologyblog.com/author/glenn_doody/”},{“display”:”Priscilla Luk”,”title”:”Managing Director, Global Research & Design, APAC”,”image”:”/wp-content/authors/priscilla_luk-228.jpg”,”url”:”https://www.indexologyblog.com/author/priscilla_luk/”},{“display”:”Liyu Zeng”,”title”:”Director, Global Research & Design”,”image”:”/wp-content/authors/liyu_zeng-252.png”,”url”:”https://www.indexologyblog.com/author/liyu_zeng/”},{“display”:”Sean Freer”,”title”:”Director, Global Equity Indices”,”image”:”/wp-content/authors/sean_freer-490.jpg”,”url”:”https://www.indexologyblog.com/author/sean_freer/”},{“display”:”Barbara Velado”,”title”:”Senior Analyst, Research & Design, Sustainability Indices”,”image”:”/wp-content/authors/barbara_velado-413.jpg”,”url”:”https://www.indexologyblog.com/author/barbara_velado/”},{“display”:”George Valantasis”,”title”:”Associate Director, Strategy Indices”,”image”:”/wp-content/authors/george-valantasis-453.jpg”,”url”:”https://www.indexologyblog.com/author/george-valantasis/”},{“display”:”Cristopher Anguiano”,”title”:”Senior Analyst, U.S. Equity Indices”,”image”:”/wp-content/authors/cristopher_anguiano-506.jpg”,”url”:”https://www.indexologyblog.com/author/cristopher_anguiano/”},{“display”:”Benedek Vu00f6ru00f6s”,”title”:”Director, Index Investment Strategy”,”image”:”/wp-content/authors/benedek_voros-440.jpg”,”url”:”https://www.indexologyblog.com/author/benedek_voros/”},{“display”:”Michael Mell”,”title”:”Global Head of Custom Indices”,”image”:”/wp-content/authors/michael_mell-362.jpg”,”url”:”https://www.indexologyblog.com/author/michael_mell/”},{“display”:”Maya Beyhan”,”title”:”Senior Director, ESG Specialist, Index Investment Strategy”,”image”:”/wp-content/authors/maya.beyhan-480.jpg”,”url”:”https://www.indexologyblog.com/author/maya-beyhan/”},{“display”:”Andrew Innes”,”title”:”Head of EMEA, Global Research & Design”,”image”:”/wp-content/authors/andrew_innes-189.jpg”,”url”:”https://www.indexologyblog.com/author/andrew_innes/”},{“display”:”Fei Wang”,”title”:”Senior Analyst, U.S. Equity Indices”,”image”:”/wp-content/authors/fei_wang-443.jpg”,”url”:”https://www.indexologyblog.com/author/fei_wang/”},{“display”:”Rachel Du”,”title”:”Senior Analyst, Global Research & Design”,”image”:”/wp-content/authors/rachel_du-365.jpg”,”url”:”https://www.indexologyblog.com/author/rachel_du/”},{“display”:”Joseph Nelesen”,”title”:”Senior Director, Index Investment Strategy”,”image”:”/wp-content/authors/joseph_nelesen-452.jpg”,”url”:”https://www.indexologyblog.com/author/joseph_nelesen/”},{“display”:”Izzy Wang”,”title”:”Senior Analyst, Factors and Dividends”,”image”:”/wp-content/authors/izzy.wang-326.jpg”,”url”:”https://www.indexologyblog.com/author/izzy-wang/”},{“display”:”Jason Ye”,”title”:”Director, Factors and Thematics Indices”,”image”:”/wp-content/authors/Jason%20Ye-448.jpg”,”url”:”https://www.indexologyblog.com/author/jason-ye/”},{“display”:”Jaspreet Duhra”,”title”:”Managing Director, Global Head of Sustainability Indices”,”image”:”/wp-content/authors/jaspreet_duhra-504.jpg”,”url”:”https://www.indexologyblog.com/author/jaspreet_duhra/”},{“display”:”Eduardo Olazabal”,”title”:”Senior Analyst, Global Equity Indices”,”image”:”/wp-content/authors/eduardo_olazabal-451.jpg”,”url”:”https://www.indexologyblog.com/author/eduardo_olazabal/”},{“display”:”Ari Rajendra”,”title”:”Senior Director, Head of Thematic Indices”,”image”:”/wp-content/authors/Ari.Rajendra-524.jpg”,”url”:”https://www.indexologyblog.com/author/ari-rajendra/”},{“display”:”Louis Bellucci”,”title”:”Senior Director, Index Governance”,”image”:”/wp-content/authors/louis_bellucci-377.jpg”,”url”:”https://www.indexologyblog.com/author/louis_bellucci/”},{“display”:”Daniel Perrone”,”title”:”Director and Head of Operations, ESG Indices”,”image”:”/wp-content/authors/daniel_perrone-387.jpg”,”url”:”https://www.indexologyblog.com/author/daniel_perrone/”},{“display”:”Srineel Jalagani”,”title”:”Senior Director, Thematic Indices”,”image”:”/wp-content/authors/srineel_jalagani-446.jpg”,”url”:”https://www.indexologyblog.com/author/srineel_jalagani/”},{“display”:”Raghu Ramachandran”,”title”:”Head of Insurance Asset Channel”,”image”:”/wp-content/authors/raghu_ramachandram-288.jpg”,”url”:”https://www.indexologyblog.com/author/raghu_ramachandram/”},{“display”:”Narottama Bowden”,”title”:”Director, Sustainability Indices Product Management”,”image”:”/wp-content/authors/narottama_bowden-331.jpg”,”url”:”https://www.indexologyblog.com/author/narottama_bowden/”}]

Active Success: Still Evasive

Anybody even slightly proficient with our SPIVA ® Scorecards will recognize that(* )most active supervisors underperform passive criteria the majority of the time This outcome is robust throughout locations and throughout time, and is shown in our just recently released mid-year 2023 report for the U.S. market. Although the scorecard covers 39 classifications of equity and set earnings supervisors, the biggest and most carefully enjoyed contrast is that in between large-cap U.S. equity supervisors and the

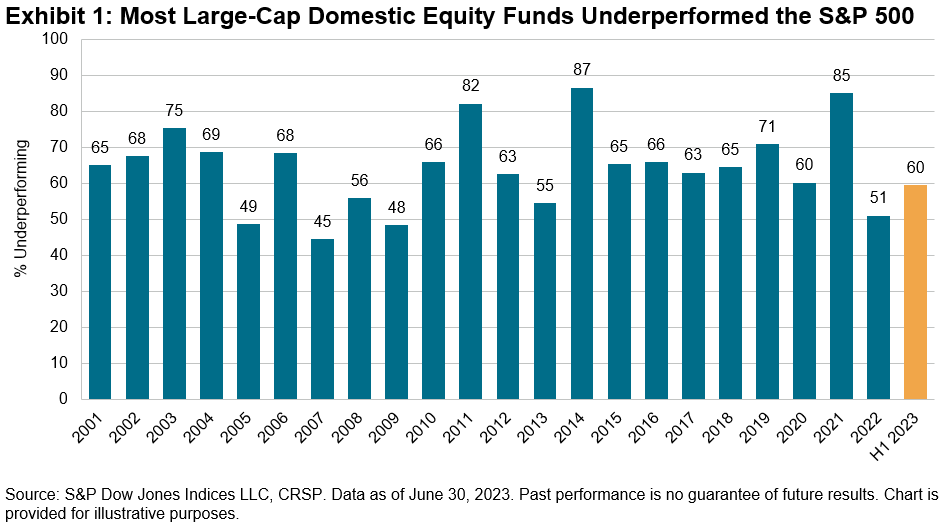

S&P 500 ® Display 1 reveals that 60% of large-cap supervisors underperformed the S&P 500 in the very first 6 months of 2023; not given that 2009 has a bulk of large-cap supervisors surpassed. More crucial than the last 6 months’ outcomes is the long-run record of active efficiency, and here our mid-year report follows its predecessors:

as period extend, active outperformance ends up being more difficult to discover Although “just” 60% of large-cap supervisors lagged the S&P 500 in the very first 6 months of 2023, after ten years the underperformance rate is 86%, and after twenty years it’s 94%. We see comparable outcomes throughout all supervisor classifications. The degeneration of outcomes over the long term is strong inferential proof that the real possibility of active outperformance is less than 50%

; if this were not so, we would anticipate longer-term outcomes to be much better than much shorter. As we have actually observed prior to, ability continues, while luck is ephemeral There are

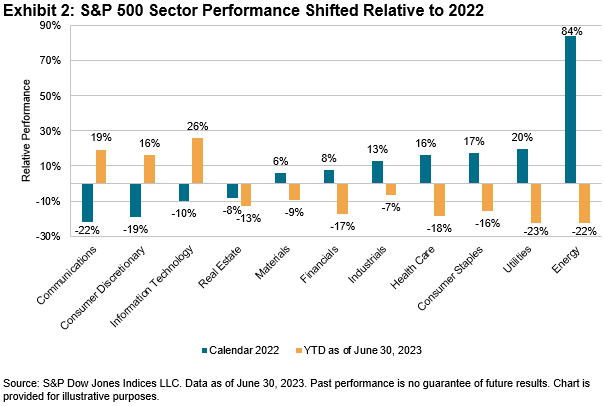

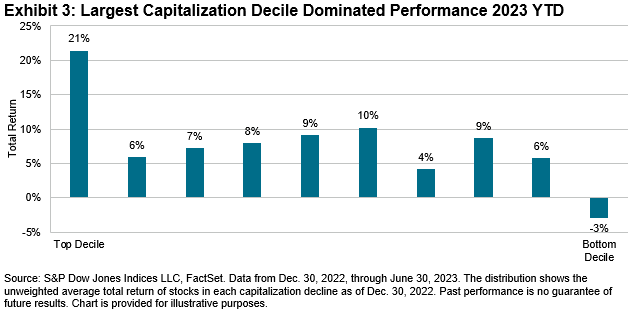

great reasons that active supervisors usually underperform, however market motions in early 2023 worsened the difficulty. Display 2 highlights the shift in relative sectoral efficiency in between 2022 and the very first 6 months of this year. The 3 worst-performing sectors in 2022 were the only 3 sectors to beat the S&P 500 in the very first half of 2023. For an active supervisor to browse through such a sector turnaround is hard in any scenario, and particularly so when, as now, the 3 sectors entering into favor are likewise the 3 with the index’s greatest typical capitalization. As Display 3 highlights, the typical return of the stocks in the S&P 500’s biggest capitalization decile was more than double the typical return of the next-best-performing decile.

When an index’s biggest constituents are amongst its finest entertainers,

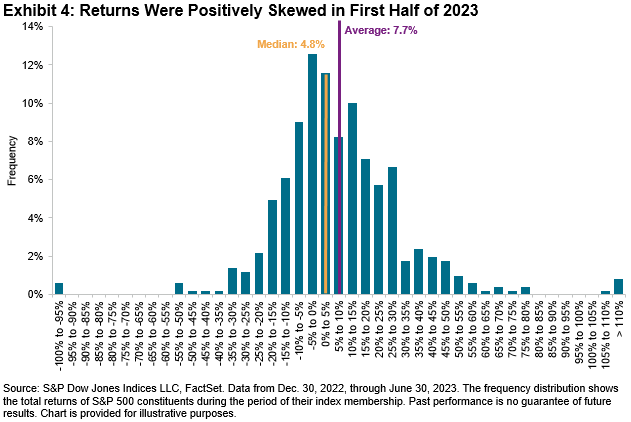

active management ends up being particularly hard: the bigger a stock’s index weight is, the less most likely it is that active supervisors will obese it. The reasonably weak efficiency of the biggest stocks assisted to describe the relatively great efficiency of active supervisors in 2022, simply as their reasonably strong efficiency in early 2023 functioned as a headwind. That headwind blows with specific strength in Display 4, which reveals the circulation of the efficiency of the members of the S&P 500 for the very first 6 months of 2023. The mean stock in the index increased by 4.8%, while the easy average of all returns was 7.7%. Due to the fact that the biggest stocks in the index were amongst the very best entertainers, the index’s 16.9% cap-weighted return was well above the easy average. The manipulated circulation of returns, and the existence of many big names on the best tail of the circulation, implied that

just 28% of the stocks in the S&P 500 surpassed the index throughout the very first 6 months Twenty-three years of SPIVA information have actually taught us that effective active management is unusual. The impressive efficiency of the S&P 500’s biggest stocks made it especially hard in the very first half of 2023. If the index’s

bigger caps continue to surpass, active supervisors’ problems are most likely to continue. The posts on this blog site are viewpoints, not recommendations. Please read our

Disclaimers Checking Out Dividends Down Under

Classifications

-

Aspects

Tags -

Ausbiz,

Australia, Australia FA, buy-write, covered call, Dividend, dividend earnings, dividend chances, high dividend, earnings methods, Jason Ye, choices, S&P/ ASX 200, S&P/ ASX 200 High Dividend Index, S&P/ ASX 300, S&P/ ASX Sustainability Evaluated Dividend Opportunities Index, yield What’s driving need for index-based access to dividends in Australia? S&P DJI’s Jason Ye surveys the dividend landscape in the Australian market and analyzes how market individuals are utilizing indices in the look for yield.

Joseph Nelesen

-

Equities,

Fixed Earnings Tags -

2023,

set earnings, International equity, Latin America, passive vs. active, S&P Brazil BMI, S&P Chile BMI, S&P/ BMV IPC, SPIVA, SPIVA Latin America, SPIVA Latin America Mid-Year 2023 Scorecard In the history of SPIVA (S&P Indices Versus Active) Scorecards, most active supervisors have actually tended to underperform criteria the majority of the time, particularly over longer durations. The

SPIVA Latin America Mid-Year 2023 Scorecard exposed that active supervisors produced blended efficiency throughout the very first half of 2023. Throughout H1 2023, more than half of active supervisors underperformed in the 5 out of 7 classifications observed, varying from 54% for Brazil Mid-/ Small-Cap funds to 91% for Mexico Equity funds. The only classifications in which less than half of supervisors underperformed were Brazil Corporate Bond and Chile Equity funds, at 30% and 36%, respectively. Over longer time horizons, outperformance was short lived throughout all 7 classifications, with 10-year underperformance rates varying from 82% for Brazil Large-Cap funds to 96% for Brazil Corporate Mutual fund (see Display 1).

Active supervisors looked for outperformance in a normally strong market environment, with the

S&P Latin America BMI increasing 21.4% over the very first half of the year and each local criteria studied producing favorable efficiency for H1 (see Exhibitions 2 and 3). The start to the year remained in significant contrast to 2022, which ended with 2 criteria, S&P Brazil MidSmallCap and Mexico’s S&P/ BMV IRT, in unfavorable area. One traditionally typical headwind for active supervisors has actually been the existence of a favorably manipulated circulation of constituent returns. Put more merely, a little number of stocks usually surpasses the benchmark return while the bulk lags. This situation was definitely present in Mexico, where just 37% of constituents surpassed the S&P/ BMV IRT in H1 2023, maybe a contributing aspect to the exceptionally high underperformance rate of Mexico Equity funds. Nevertheless, more than half of benchmark constituents surpassed throughout all 4 other equity classifications (see Display 4). This reasonably uncommon situation implied that an arbitrarily chosen stock in each of the 4 criteria had more than a 50% possibility of being an outperformer. In spite of this absence of favorable alter, couple of supervisors taken advantage of the chance, as the Chile Equity fund classification was the sole classification in which less than half of supervisors underperformed.

Throughout many Latin American equity markets, dispersion levels in H1 2023 fell a little from 2022’s raised levels (see Display 5). Greater dispersion, a procedure of cross-sectional volatility revealing distinctions in between stock returns within each index, has actually usually been associated not just with higher benefits from selecting surpassing stocks however likewise with higher charges from picking underperformers.

For fund selectors, threats of underperformance are twofold. Initially, results program that many funds underperform their criteria gradually, making the procedure of discovering a future winner statistically not likely. Second, the charge of picking an underperforming fund has actually traditionally been more penalizing in regards to typical unfavorable efficiency than the typical benefit created from surpassing funds. More exactly, bottom-quartile funds underperformed their particular criteria to a higher degree than top-quartile funds surpassed in 4 out of 7 classifications in H1 2023 (see Display 6).

While the outcomes for the complete year are yet to be seen, for numerous active fund supervisors in Latin America, efficiency difficulties throughout the very first half might have made the climb ahead look much steeper.

The posts on this blog site are viewpoints, not recommendations. Please read our

Jim Wiederhold

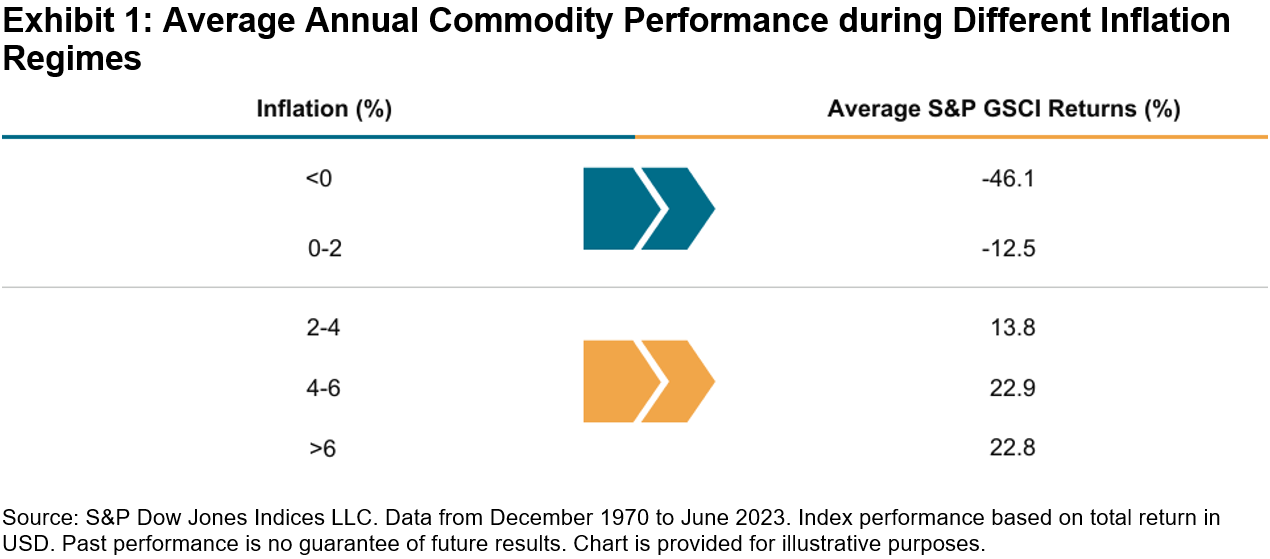

S&P GSCI, increased over 4% in September and 16% in Q3 2023. This highlighted the possible diversity qualities of this property class, as equities and set earnings both fell throughout the month. Products’ low connections to other property classes can offer a cushion when other higher-allocated property classes drop throughout risk-off situations as was seen last month. Including products to a technique tends to moisten general portfolio threat and drawdowns gradually. Historically, throughout durations of excellent macroeconomic shifts like we are experiencing now, a varied portfolio has actually tended to carry out much better than more extremely focused ones. Throughout durations of high and sticky inflation readings, products have actually supplied a hedge when other property classes tend to drop from greater input expenses. The primary factors to the outsized efficiency last month were the energy products. Supply cuts from Saudi Arabia and Russia were the greatest drivers as need continued internationally. The heading S&P GSCI presently has a weight in energy products of over 60% due to its building as a world production-weighted index. Market individuals duplicating it as an inflation hedge experienced greater returns just recently in contrast to other equivalent product indices, which tend to be more similarly weighted. Energy products tend to have the greatest inflation beta or level of sensitivity to modifications in inflation gradually. Other products utilized in petroleum items such as sugar likewise increased by 5%, with its heavy usage in ethanol in South America.

The

S&P GSCI Farming fell 4.35% and the S&P GSCI Rare-earth Elements fell 3.76% in the 3rd quarter. Both sectors, in addition to many products, were struck by the headwind of an increasing U.S. dollar. For the farming products, lower soybean use and remarkably bigger wheat production figures were reported in the most recent USDA quarterly stocks report. Within the rare-earth elements, gold and silver both fell as genuine rates continued to increase. Gold tends to be inversely associated to genuine rates however this hasn’t held true for the majority of 2023. Current heavy reserve bank bullion purchasing might have been the factor for gold’s strength up until now in 2023. The posts on this blog site are viewpoints, not recommendations. Please read our

Classifications

-

Equities,

Fixed Earnings, Thematics Tags -

Chimera Capital,

Dubai Financial Markets, Eric Solomon, ESG, ETFs, index-based methods, indexing Shariah, Islamic law, John Welling, Muslim financiers, Shariah, Shariah compliance, Sherif Salem, socially mindful investing, Sukuk, thematics How are indices assisting broaden the series of Shariah-compliant tools for market individuals? S&P DJI’s John Welling and Chimera Capital’s Sherif Salem sign up with Dubai Financial Markets’ Eric Solomon for an appearance inside how S&P DJI’s Shariah-compliant and Sukuk indices are assisting financiers examine and gain access to regional, local, and worldwide markets while sticking to Islamic law and lining up with customer goals.