ROBYN BECK/AFP by means of Getty Images

Financial investment thesis

I have actually been exceptionally bearish about Lucid ( NASDAQ: LCID) in 2023, and this pessimism has actually aged well. The stock has actually tanked by 44% considering that I last covered it in August 2023, and today, I wish to share my view about the advancements that have actually unfolded over the last half a year and upgrade my assessment quote. Obviously, Lucid has a rich financier backing business and a fortress balance sheet. However at the exact same time, the business has a really weak performance history with regularly stopping working to satisfy agreement expectations, and the business’s EV sales development substantially drags rivals, even in spite of little scale and simple to magnify compensations. Additionally, my assessment analysis recommends the stock is around 3 times miscalculated under relatively positive presumptions. All in all, I restate my “Strong Offer” ranking for Lucid.

Monetary analysis upgrade

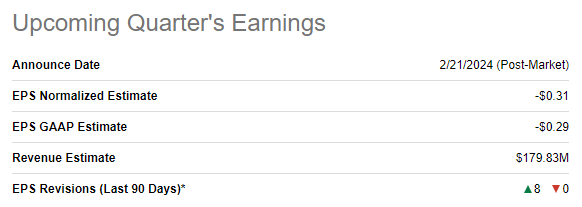

The business reports its December 2023 quarter profits on February 21. I see significant optimism from agreement price quotes considering that there were 8 EPS up modifications over the last 90 days. In spite of earnings forecasted to leap sequentially by 30%, the adjusted EPS is anticipated to avoid -$ 0.25 to -$ 0.31 on a QoQ basis. From the YoY viewpoint, the photo is even worse considering that LCID’s leading line is forecasted to dip by around 31%.

Looking For Alpha

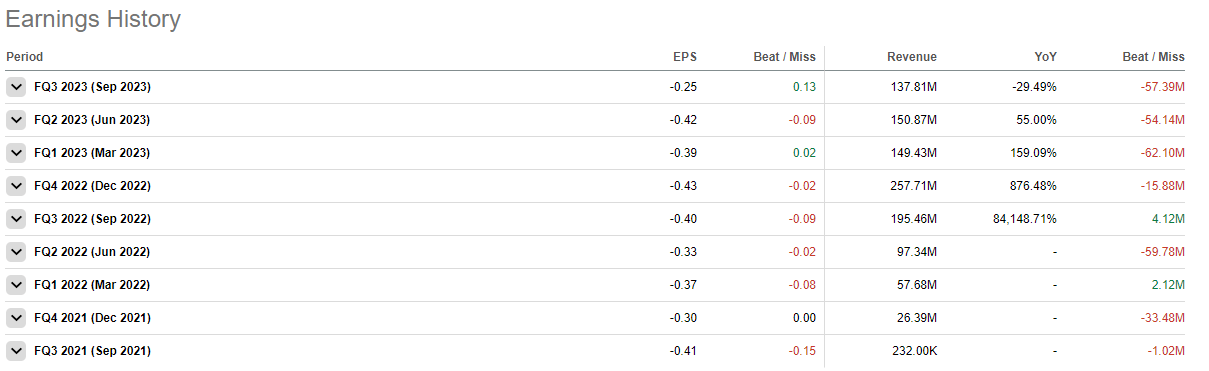

For a young business that still has actually not accomplished success, it is rather challenging to anticipate likelihoods of beating agreement price quotes, however when I take a look at Lucid’s profits history, it offers me a high level of conviction that the business will miss out on expectations. Considering that the business initially began openly launching its quarterly profits in FQ3 2021, Lucid has actually never ever topped agreement price quotes in regards to both earnings and EPS. That stated, I am rather downhearted about the approaching profits release.

Looking For Alpha

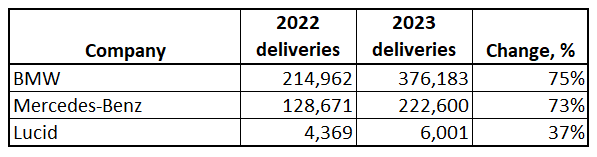

My pessimism is likewise sustained by the 2023 production and shipment numbers. Considering that Lucid positions itself as a high-end EV, I believe that thinking about Mercedes-Benz ( OTCPK: MBGAF) and BMW ( OTCPK: BMWYY) as rivals would be reasonable. Let’s see how Lucid’s EV shipments’ 2022 vs 2023 characteristics looked compared to the 2 popular German OEMs. As observed listed below, the increase in shipments for BMW and Mercedes carefully paralleled each other. Nevertheless, Lucid routed substantially, with sales development lagging by more than double. It is necessary to keep in mind that, simply from a mathematical viewpoint, smaller-scale OEMs ought to display more significant development as contrasts are simpler to magnify. I believe that the above table is a big warning suggesting that Lucid is losing the high-end section.

Assembled by the author from OEM’s main news release

I would likewise like to include that offered an enormous nonreligious EV pattern and the fairly loose EV high-end section, I anticipate the competitors to heighten. Apart from widely known German tradition car manufacturers, there are Chinese EV start-ups like NIO ( NIO) and Li Car ( LI), which currently run at a much bigger scale than Lucid does. Chinese EV makers are still not broadening abroad strongly, once they begin doing so, I think they will have a possibility to end up being significant gamers in the industrialized world.

It is likewise essential to keep in mind that the world’s biggest tradition car manufacturer, Toyota Motor ( TM), high-end brand name Lexus is likewise widely known and made strong track record in the U.S. That stated, when Toyota begins increase more towards the EV shift, I think that Lexus will likewise likely end up being a strong force in the high-end EV section. There are likewise dynamic British high-end brand names like Rolls-Royce ( OTCPK: RYCEY) and Bentley, which likewise have full-electric ramp-up strategies.

Rolls-Royce site

To be able to combat with such unsafe rivals having dynamic brand names, Lucid’s execution will be perfect. On the contrary, the business has a history of falling significantly behind its enthusiastic pre-IPO pledges to financiers, and a multibillion-dollar money burn rate is still huge.

Evaluation upgrade

LCID lost 70% of its worth over the last 12 months, substantially dragging the wider U.S. stock exchange. Considering that Lucid is still deeply unprofitable, there are few assessment ratios offered, however comparing the price-to-sales [P/S] ratio to peers appears like a reasonable workout. Lucid’s 9.3 forward P/S ratio is an obvious outlier, while Rivian ( RIVN) and the 3 most popular Chinese EV start-ups have a P/S varying from 1.3 to 2.3. That stated, Lucid is still extremely pricey from the P/S/ viewpoint, even after an enormous stock plunge over the last 12 months.

Looking For Alpha

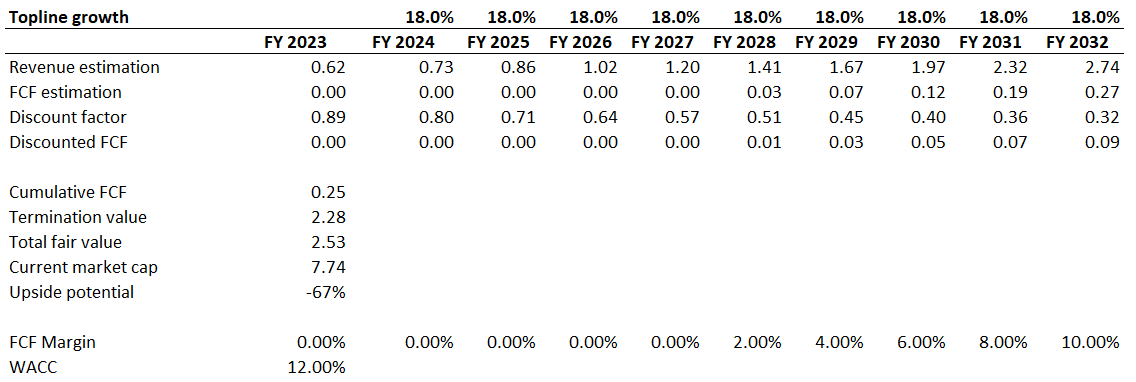

Now, let me carry on to the reduced capital [DCF] simulation. Considering that there are 3 rate cuts prepared in 2024, I reduce WACC from 12% to 11.25%, presuming it will be a 25-basis point action each time. For earnings development, I normally count on agreement price quotes, however they look too positive to me when we discuss Lucid due to the fact that Wall Street experts forecast a shocking 51% CAGR for the years. This looks definitely impractical to me, thinking about the truth that the worldwide high-end EV section is anticipated to intensify practically 3 times slower at an 18% CAGR. With the competitors in the high-end EV section heightening and Lucid’s history of frustrating financiers, I think the forecasted high-end section’s 18% earnings CAGR will be a lot more reputable. Figuring out the complimentary capital margin is extremely challenging for LCID due to the fact that Wall Street experts anticipate the EPS to strike favorable just in FY 2028. The level of unpredictability is severe, however I think that lining up the FCF margin breakeven with the EPS forecast appears like a conservative option. I anticipate the FCF margin to attain 2% in FY 2028 and broaden by 2 portion points annual. I neglect the present strong net money position due to the fact that the business’s money burn rate is high, and these reserves will extremely likely be made use of far previously than the business begins producing favorable FCF.

Author’s estimations

According to my DCF simulation, business’s reasonable capitalization is $2.53 billion. This is more than 3 times lower than the present market cap, implying there is still an enormous disadvantage capacity. To conclude the assessment procedure, I motivate readers to truthfully think about whether, offered more than enough resources, they would invest $7.7 billion completely ownership of Lucid.

Dangers to my bearish thesis

The stock is extremely unstable and can show brief durations of sharp stock cost spikes, which LCID bears ought to understand. That stated, short-term motions in the instructions opposite to my thesis are likely. At the exact same time, offered the weak basics, these spikes are not likely to be sustainable. For instance, the stock is presently around 25% more pricey than it was simply 10 days earlier.

Looking For Alpha

As it is commonly understood, Lucid is backed by among the biggest sovereign funds on the planet, the Saudi Arabian Public Mutual Fund The fund has around $777 billion in properties under management, and it appears like such a big fund will have the ability to continue wagering huge and funding Lucid for a long period of time. Lucid’s success may even be the leading concern for the PIF offered an enthusiastic Saudi Vision 2030 tactical strategy to end up being “the heart of the Arab and Islamic worlds”, which will be difficult without development. Considering that the worldwide shift to EVs is among the biggest technological patterns in the 21st century, I think that it is extremely most likely that being at the leading edge of the EV pattern is among the top priorities of the Saudi side. That stated, I will be unsurprising if Saudi Arabia begins supporting Lucid more strongly so the business can provide appealing terms to the market’s brightest engineers, designers, and marketing leaders. With huge funds behind its back, there is constantly a possibility that any business may make a remarkable turn-around.

Looking For Alpha

Bottom line

To conclude, I prompt my readers not to attempt to capture this falling knife due to the fact that a number of basic aspects explain that LCID should have a “Strong Offer” ranking to be restated. In spite of having a robust balance sheet supported by the Saudi PIF, there seems a detach in between Lucid’s resources and their reliable usage by management to take full advantage of investor worth. The plain contrast in shipment development, dragging Mercedes and BMW by more than double in 2023, indicates a substantial issue. This efficiency space raises doubts about Lucid’s capability to endure the extreme competitors in the market, which will likely just continue to heighten.