Up until now in 2024, less homes are taking rate cuts than in 2023, and this pattern is on the brink of breaking listed below the 2023 lows in rate cuts portions. While weekly stock is still falling, we have year-over-year development in overall active listing and brand-new listings information. This casts doubt on a home mortgage rate lockdown, as home mortgage rates are likewise greater year over year.

What is all this information indicating? We may have a typical year in real estate compared to the previous 4 years! So, we require to be extremely conscious of the weekly information to get hints on the market.

Price-cut portion

Every year, one-third of all homes take a rate cut before offering– this is a standard real estate activity. Nevertheless, this information can move more powerful in either instructions when home mortgage rates increase or fall strongly.

An ideal example was in 2022: when real estate stock increased quicker as need crashed, the portion of rate cuts increased quicker. After November of 2022, home sales stopped crashing and the price-cut portion information has actually supported. Even when home mortgage rates were approaching 8% in 2015, the variety of homes taking rate cuts was constantly 4% listed below the 2022 level. Presently, the price-cut portion is less than 1% from breaking listed below the lows embeded in 2023. Need is increasing from a low bar, and overall real estate stock levels are still traditionally low. This is the price-cut portion for recently over the last couple of years:

- 2024: 30.1%

- 2023: 32.2%

- 2022: 18.3 %

Weekly real estate stock information

An actually favorable story for 2024 is that we have greater real estate stock year over year. It isn’t anything to compose home about, however it’s a favorable story nevertheless. I am a really pro-housing supply individual and will feel better about the real estate market when we go back to pre-COVID-19 levels for overall active listings. Recently, stock fell week to week however was up over this time in 2015. I am still hoping we get the seasonal bottom in stock in February and not March or April.

Here is a take a look at recently:

- Weekly stock modification (Feb. 2-9): Stock fell from 497,389 to 494,862

- Very same week in 2015 (Feb. 3-10): Stock fell from 457,717 to 444,129

- The current stock bottom remained in 2022 at 240,194

- The stock peak for 2023 was 569,898

- For context, active listings for today in 2015 were 947,864

New listings information

The brand-new listing information put a huge smile on my face today! For the very first time in a while, this was an excellent week for brand-new listing information. Over the last couple of years, we have actually been trending at the most affordable levels ever, so seeing a favorable week is excellent. Likewise, this brings into concern the home mortgage rate lockdown property considering that home mortgage rates are greater annual. This is something I have actually been talking about for numerous months on CNBC

Weekly brand-new listing information for recently over the last numerous years:

- 2024: 51,875

- 2023: 44,533

- 2022: 45,594

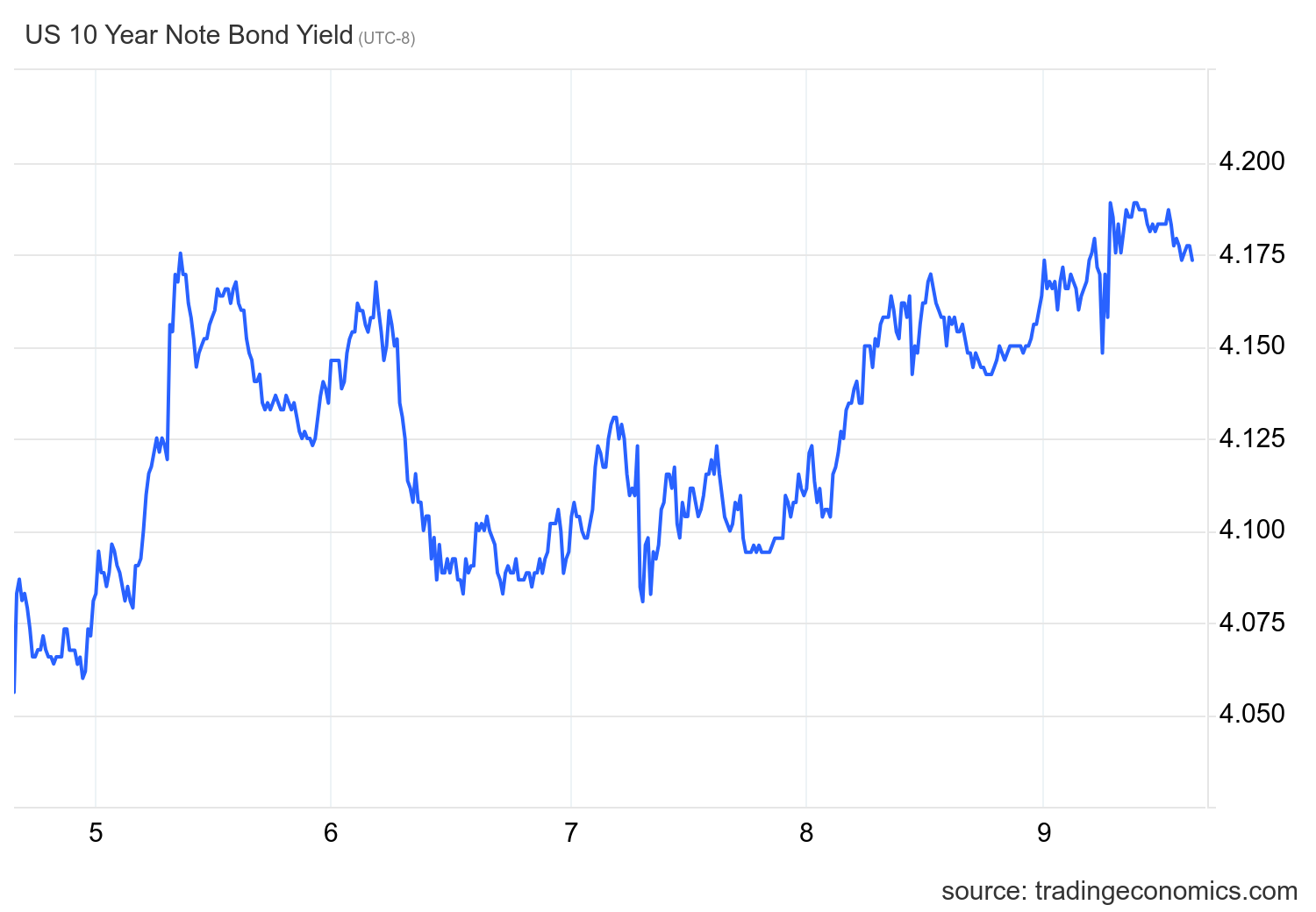

Home loan rates and the 10-year yield

The 10-year yield is the secret for real estate in 2024. In my 2024 projection, I put the 10-year yield variety in between 3.21% -4.25%, with an important line in the sand at 3.37% If the financial information remains company, we should not break listed below 3.21%, however if the labor information gets weaker, that line in the sand– which I call the Gandalf line, as in “you will not pass”– will be checked.

This 10-year yield variety equates to home mortgage rates in between 5.75% -7.25%, however this presumes spreads are still bad. The spreads have actually been enhancing this year a lot that if we struck 4.25% on the 10-year yield, we still will not see 7.25% in home mortgage rates.

Recently was extremely intriguing since we had a couple of Fed occasions to handle. Initially there was the after-effects of Jay Powell’s 60 Minutes interview Then the president of the Minneapolis Fed, Neel Kashkari, made declarations about how the Federal Reserve policy isn’t as tight as individuals would think, providing his case in this post Nevertheless, simply a couple of days later on, Kashkari discussed how his gut informs him that 2 to 3 rate cuts are undoubtedly in play. I discussed this turn of occasions with Editorial director Sarah Wheeler on the HousingWire Daily podcast

The 10-year yield closed at the week high up on Friday, although the extremely expected CPI modifications information revealed that the inflation downturn was precise and no upward modifications were made.

Home loan rates didn’t walk around excessive recently, varying in between 7.04% and 6.95%. Nevertheless, as we can see, even with considerable development on the development rate of inflation decreasing, home mortgage rates are near 7% and the 10-year yield is still over 4%. My point on this subject has actually been clear for a while: the Fed hasn’t rotated, and they have an extremely limiting policy versus real estate as they still think in their COVID-19 real estate policy keeping home sales trending near lowest levels.

Purchase application information

Recently, we had some confusion on purchase apps, as the unadjusted numbers revealed 6% week-to-week development. We do not represent that information line ever; the real numbers revealed -1% week-to-week development, and we are still revealing unfavorable 19% year-over-year information. In 2015, we had much better favorable information as home mortgage rates headed down towards 6% before rates began greater, so the year-over-year compensations will get simpler. Nevertheless, if we had strong real estate need, purchase application information would quickly be favorable year over year and by double digits also. In the meantime, simply think about a bounce from record lows in need.

The year-to-date count is 2 favorable reports and 2 unfavorable purchase application reports. Considering that home mortgage rates began to fall in November of 2023, we have actually had 8 favorable and 2 unfavorable weeks after making some vacation changes. This has the possible to take the seasonal stock bottom to March. Nevertheless, I am expecting the bottom in February.

The week ahead: It’s inflation week, plus retail sales and real estate starts

We have a great deal of information showing up: 2 inflation reports, retail sales, the home builder’s self-confidence index and real estate starts. The CPI inflation information will be interesting over the next 6 to 7 months since we can begin to see the lease aspect kicking into greater equipment to the drawback. Although the Fed states they do not represent shelter when speaking about rate cuts, lower inflation will bring increasingly more pressure on them to pivot and bring rates down. We will have lots of information lines to work from next week.